Advertisement

- United States

- /

- IT

- /

- NasdaqGM:MDB

Is MongoDB, Inc. (NASDAQ:MDB) Potentially Undervalued?

Let's talk about the popular MongoDB, Inc. (NASDAQ:MDB). The company's shares received a lot of attention from a substantial price increase on the NASDAQGM over the last few months. The company's trading levels have reached its high for the past year, following the recent bounce in the share price. With many analysts covering the large-cap stock, we may expect any price-sensitive announcements have already been factored into the stock’s share price. However, could the stock still be trading at a relatively cheap price? Today we will analyse the most recent data on MongoDB’s outlook and valuation to see if the opportunity still exists.

View our latest analysis for MongoDB

Is MongoDB Still Cheap?

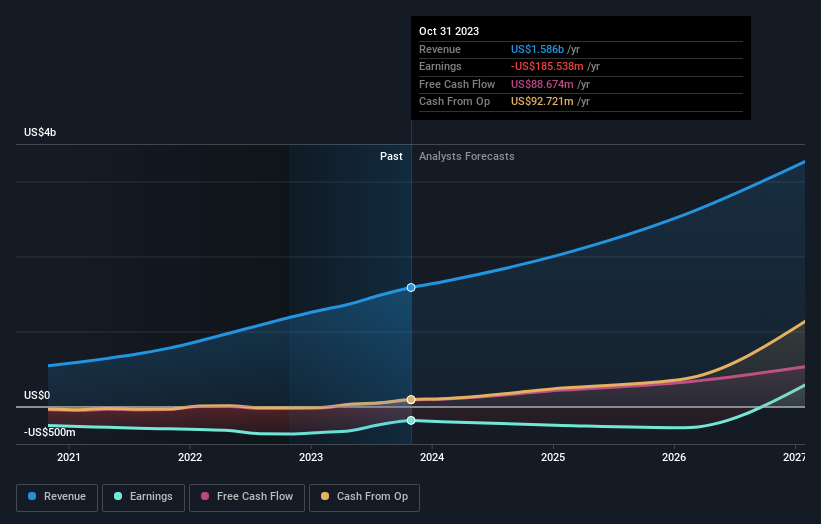

MongoDB appears to be overvalued by 40% at the moment, based on our discounted cash flow valuation. The stock is currently priced at US$457 on the market compared to our intrinsic value of $326.86. This means that the buying opportunity has probably disappeared for now. If you like the stock, you may want to keep an eye out for a potential price decline in the future. Since MongoDB’s share price is quite volatile, this could mean it can sink lower (or rise even further) in the future, giving us another chance to invest. This is based on its high beta, which is a good indicator for how much the stock moves relative to the rest of the market.

What kind of growth will MongoDB generate?

Investors looking for growth in their portfolio may want to consider the prospects of a company before buying its shares. Although value investors would argue that it’s the intrinsic value relative to the price that matter the most, a more compelling investment thesis would be high growth potential at a cheap price. However, with an extremely negative double-digit change in profit expected over the next couple of years, near-term growth is certainly not a driver of a buy decision. It seems like high uncertainty is on the cards for MongoDB, at least in the near future.

What This Means For You

Are you a shareholder? If you believe MDB is currently trading above its value, selling high and buying it back up again when its price falls towards its real value can be profitable. Given the risk from a negative growth outlook, this could be the right time to de-risk your portfolio. But before you make this decision, take a look at whether its fundamentals have changed.

Are you a potential investor? If you’ve been keeping tabs on MDB for some time, now may not be the best time to enter into the stock. The company’s price has climbed passed its true value, in addition to a risky future outlook. However, there are also other important factors which we haven’t considered today, such as the financial strength of the company. Should the price fall in the future, will you be well-informed enough to buy?

With this in mind, we wouldn't consider investing in a stock unless we had a thorough understanding of the risks. While conducting our analysis, we found that MongoDB has 2 warning signs and it would be unwise to ignore these.

If you are no longer interested in MongoDB, you can use our free platform to see our list of over 50 other stocks with a high growth potential.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGM:MDB

MongoDB

Provides general purpose database platform worldwide.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2542.9% undervalued

64 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative

HE

HedgeY on IonQ ·

The Best-Funded Quantum Platform and Still a Stock Priced for Perfection

Fair Value:US$487.1% overvalued

24 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5446.8% undervalued

41 followersusers have followed this narrative

1 commentusers have commented on this narrative

7 likesusers have liked this narrative

IV

Ivoed on Netflix ·

Netflix’s Business Quality Is Clear. The Harder Question Is Whether The Stock Is Still Cheap

Fair Value:US$829.5% undervalued

22 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

BR

Bravosatya on Meta Platforms ·

Meta Platforms - Zuckerberg’s investment decisions are impulsive or Prudent?

Fair Value:US$730.0216.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JU

julio on FIGS ·

Figs valuation

Fair Value:US$14.3930.2% undervalued

20 followersusers have followed this narrative

6 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AS

AstrisCorporateAdvisory on MIRAI ·

Improving NOI growth visibility on wider rent gap

Fair Value:JP¥77.06k46.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75030.3% undervalued

80 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9634.1% undervalued

62 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7441.1% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative