Advertisement

- United States

- /

- Software

- /

- NasdaqGS:MANH

Manhattan Associates (MANH): Assessing Valuation After Pacsun’s Fast-Track POS Rollout and Retail Efficiency Gains

Simply Wall St

Reviewed by Simply Wall St

Manhattan Associates (MANH) is back in the spotlight following Pacsun's swift rollout of its cloud-native POS solution across more than 300 stores. This initiative quickly delivered measurable boosts to Pacsun's revenue, operational efficiency, and cost control.

See our latest analysis for Manhattan Associates.

Manhattan Associates’ recent win with Pacsun comes at a pivotal time, as the company navigates shifting sentiment in the software sector. While its latest cloud-native retail deployment showcased real-world value, the 1-year total shareholder return sits at -34.6%, with the share price closing at $178.23. This reminds investors that momentum has faded after several strong years, even though long-term total returns remain compelling.

If you're curious where opportunity is building next, consider broadening your search and discover fast growing stocks with high insider ownership

With shares trading at a notable discount to analyst targets and expectations muted despite solid long-term returns, the question now is whether Manhattan Associates represents underappreciated value or if the market is already taking its future growth into account.

Price-to-Earnings of 49.7x: Is it justified?

Manhattan Associates currently trades at a price-to-earnings ratio of 49.7x, placing it well above both the industry and peer group averages. With the last close at $178.23, this steep multiple clearly signals the market is pricing in strong future performance.

The price-to-earnings (P/E) ratio measures how much investors are willing to pay today for a dollar of earnings tomorrow. In software, where high growth and predictable revenue streams are prized, elevated P/E ratios often highlight investors’ expectations for robust profit expansion over the coming years.

However, Manhattan Associates’ P/E of 49.7x outpaces the US Software industry’s average of 31.2x and the peer average of 37.6x. In addition, the estimated fair P/E for the company stands at 32.1x. The market could eventually revert towards this level if growth expectations cool or peer valuations shift.

Explore the SWS fair ratio for Manhattan Associates

Result: Price-to-Earnings of 49.7x (OVERVALUED)

However, ongoing sector volatility and any slowdown in annual revenue or net income growth could present challenges for the current valuation and investor optimism.

Find out about the key risks to this Manhattan Associates narrative.

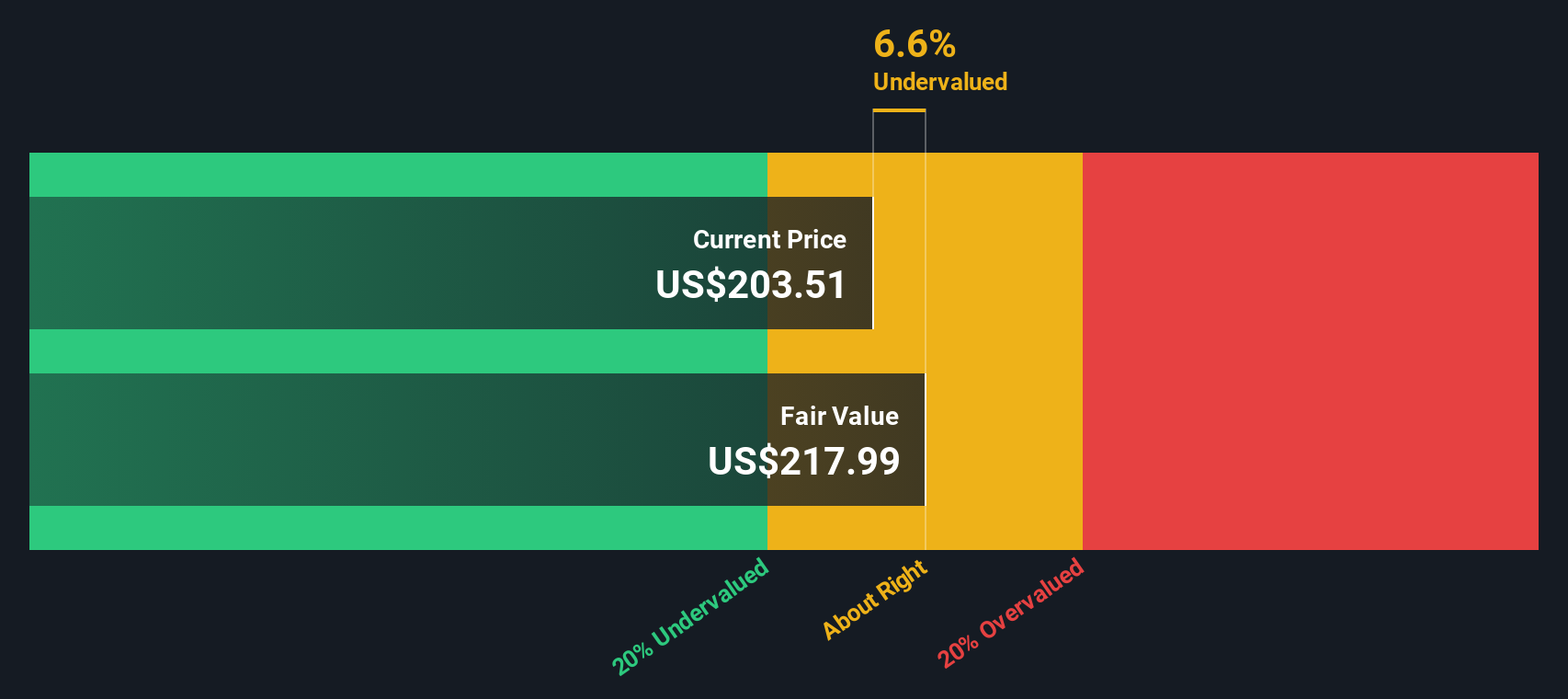

Another View: Discounted Cash Flow Model Shows Undervaluation

While Manhattan Associates looks pricey when compared on a price-to-earnings basis, our DCF model offers a different outlook. It suggests shares are trading about 21% below their estimated fair value. This hints at the potential for upside if future cash flows come through. Which perspective will prove closer to reality as the story unfolds?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Manhattan Associates for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 886 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Manhattan Associates Narrative

If you see things differently or want to dive into the numbers yourself, you can craft your own analysis and perspective in just a few minutes, and Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Manhattan Associates.

Looking for More Investment Ideas?

Smart investors keep their edge by spotting trends early. Don’t let great opportunities slip by. Expand your horizons with these standout stock ideas you can act on right now:

- Capitalize on rapid shifts in medicine and technology by checking out these 32 healthcare AI stocks among emerging healthcare innovators.

- Start building passive income streams by reviewing these 16 dividend stocks with yields > 3% and find companies offering yields above 3%.

- Catch tailwinds in financial tech as you scan these 82 cryptocurrency and blockchain stocks, where blockchain and digital currencies are reshaping global markets.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:MANH

Manhattan Associates

Develops, sells, deploys, services, and maintains software solutions to manage supply chains, inventory, and omni-channel operations.

Flawless balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor