Advertisement

- United States

- /

- Software

- /

- NasdaqGS:IDCC

InterDigital (IDCC): Evaluating Valuation After Earnings Gains and New Video Technology Unveiling

Reviewed by Simply Wall St

InterDigital (IDCC) just made headlines with two developments that could shape how investors think about this stock’s trajectory. The company is preparing to showcase its latest video innovation, an advanced combination of Versatile Video Coding and film grain preservation, at the upcoming International Broadcasting Convention in Amsterdam. At the same time, InterDigital’s recent improvements in both earnings and margins have sparked conversations about whether the company is turning operational strength into sustainable growth, especially as it grabs industry attention with its technology advances.

These announcements come after a year marked by meaningful upward momentum for InterDigital’s share price. The stock has outperformed, delivering strong gains across both short and long timeframes. That performance is unfolding even as InterDigital moves to demonstrate leadership in video compression and streaming technology, aiming to set a standard for next-generation media delivery.

With InterDigital pushing both financial and innovation boundaries, is the current share price factoring in too much future optimism or is there a real opportunity to be uncovered?

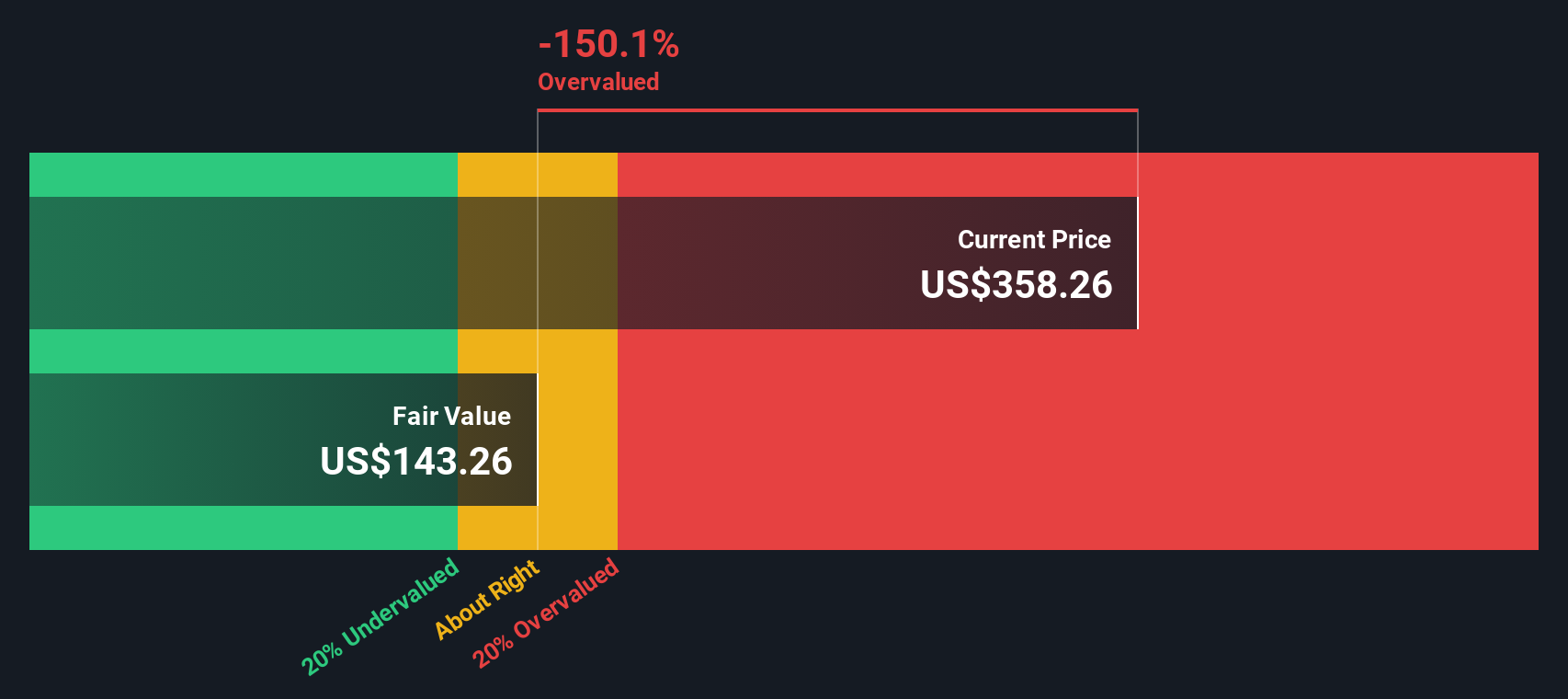

Most Popular Narrative: 12.5% Overvalued

The most widely followed narrative sees InterDigital trading above fair value, with major assumptions about its growth trajectories and premium assigned to its future earnings.

The recent 67% uplift in the Samsung license and an all-time high annualized recurring revenue, driven by multi-year agreements with major OEMs, have set highly optimistic expectations for continued outsized growth in future contract renewals. This may potentially inflate valuation multiples and overstate the sustainable revenue trajectory.

What is driving this bold price tag? The narrative leans on aggressive forecasts for future margins, licensing wins, and the expansion into new markets. However, the numbers behind this story—future revenue, profits, and contract assumptions—are not what you might expect from a typical software stock. Think the growth outlook is obvious? Consider the key projections powering this valuation call.

Result: Fair Value of $266.5 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, breakthrough license renewals with major manufacturers or rapid expansion into new verticals could quickly challenge the view that InterDigital is overvalued.

Find out about the key risks to this InterDigital narrative.Another View: Sizing Up the Numbers

Looking at InterDigital through our DCF model, the story changes. This method suggests the shares may be trading far above what underlying cash flows support. Could future growth make up the gap, or is caution needed?

Look into how the SWS DCF model arrives at its fair value.

Stay updated when valuation signals shift by adding InterDigital to your watchlist or portfolio. Alternatively, explore our screener to discover other companies that fit your criteria.

Build Your Own InterDigital Narrative

If you’re looking to dig into the numbers yourself or approach the story from a fresh perspective, you can craft your own take on InterDigital in just a few minutes. Do it your way.

A great starting point for your InterDigital research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Smart Investment Opportunities?

Don’t let your next big opportunity pass you by. Leap ahead with handpicked investment ideas designed to match different strategies, sectors, and breakthrough trends.

- Capitalize on digital transformation by tracking innovators in the artificial intelligence sector with our selection of AI penny stocks.

- Boost your portfolio’s income potential by targeting stable companies offering attractive yields using our collection of dividend stocks with yields > 3%.

- Discover undervalued gems with potential for growth by tapping into our suite of undervalued stocks based on cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Kshitija Bhandaru

Kshitija (or Keisha) Bhandaru is an Equity Analyst at Simply Wall St and has over 6 years of experience in the finance industry and describes herself as a lifelong learner driven by her intellectual curiosity. She previously worked with Market Realist for 5 years as an Equity Analyst.

About NasdaqGS:IDCC

InterDigital

Operates as a global research and development company focuses on wireless, visual, artificial intelligence (AI), and related technologies.

Flawless balance sheet, good value and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Optimi Health ·

The Only Psychedelic Company Already Selling MDMA and Psilocybin to Real Patients, Yet Priced Like It Doesn’t Exist

Fair Value:US$1157.5% undervalued

47 followersusers have followed this narrative

2 commentsusers have commented on this narrative

7 likesusers have liked this narrative

WE

WealthAP on Novo Nordisk ·

Novo Nordisk (NVO): Is the "Easy Growth" Story Over?

Fair Value:DKK 407.7721.4% undervalued

66 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

VA

ValueInvestingSubstack on Zoetis ·

Zoetis down -50% over the past year

Fair Value:US$92.9218.9% undervalued

22 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

CE

CentryResearch on Centrus Energy ·

Centrus Energy: The Next Nuclear Bottleneck Isn't Reactors. It's Fuel.

Fair Value:US$19013.7% undervalued

24 followersusers have followed this narrative

0 commentsusers have commented on this narrative

10 likesusers have liked this narrative

Recently Updated Narratives

WI

WisetoWealth on PayPal Holdings ·

The Underrated Transformation of a Digital Payments Giant

Fair Value:US$90.3137.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BL

Blagget on Terra Balcanica Resources ·

The C$4M Explorer Positioned to Become Europe's First Antimony Mine

Fair Value:CA$0.487.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

david_6nroa on Charter Communications ·

Charter is undervalued - Here's why.

Fair Value:US$87.0741.6% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.919.1% undervalued

81 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28026.1% undervalued

185 followersusers have followed this narrative

9 commentsusers have commented on this narrative

15 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6513.6% undervalued

71 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Trending Discussion

DE

derek_3wsdg on Teladoc Health ·

You’ve overlooked the activist investor factor. Travis Cocke’s Voss has announced 5% ownership through a 13G filing. They’ve added to that 5% since, and in doing so, have created a structural trap door for 27.42 Million Shares actively sold short. Chuck will announce lots of positives on July 29 but it’s what Voss announces shortly after that will rock the overextended Teledoc shorts. The Walmart partnership is the tip of the iceberg. The market is missing the sheer regulatory and enterprise friction of modern corporate healthcare. Teladoc isn't a "consumer app"; it is the primary digital infrastructure integrated directly into the legacy backends of Tier-1 insurance companies and fortune 500 employers, covering 105 million+ lives. Teladoc is acting as the digital top-of-funnel engine for the world's largest retailer. If Voss pushes the narrative that Teladoc is effectively the outsourced digital brain of Walmart's entire healthcare footprint, the fair value shifts from a basic health multiple to an enterprise distribution premium. Additionally , we are in a structural gold rush for high-quality, legally compliant, longitudinal medical data to train vertical healthcare AI models. Large technology hyperscalers and pharmaceutical giants cannot simply scrape the internet for this; they need structured clinical inputs. Teladoc sits on one of the largest de-identified virtual medical datasets on earth. From the activist playbook , we’ll see Voss demand the immediate creation of a Data & Diagnostics Licensing Division, transforming a legacy liability into an incredibly high-margin, pure-software data asset that requires zero human clinician hours to scale. Chuck is doing great work and deserves credi5 for the Teledoc turnaround but it will be Travis Cocke who will be responsible for a share price way beyond your $15 valuation.

1

|0