Advertisement

- United States

- /

- Software

- /

- NasdaqGS:IDCC

A Look At InterDigital (IDCC) Valuation After Record Results And Expanded AI And Licensing Growth

InterDigital (IDCC) has drawn fresh attention after reporting record 2025 results, supported by long term smartphone and electronics licensing agreements, expanding AI and video technology efforts, and updated 2026 earnings guidance.

See our latest analysis for InterDigital.

Following the 2025 results and fresh 2026 guidance, InterDigital’s share price has surged, with a 1 month share price return of 20.06% and a 1 year total shareholder return of 83.40%, building on a very large 5 year total shareholder return.

If this AI and wireless story has your attention, it could be a good moment to scan other opportunities through our list of 56 profitable AI stocks that aren't just burning cash.

With the share price up sharply and analysts’ average target sitting above the current US$371.08 level, the key question now is whether InterDigital’s recent success is still underappreciated by the market or whether any future growth is already fully reflected in the price.

Most Popular Narrative: 19.8% Undervalued

InterDigital’s most followed narrative pegs fair value at about $462.67 per share versus the last close of $371.08, putting a spotlight on what is driving that gap.

The combination of modest revenue growth assumptions and higher margins is framed by bullish analysts as a way to support cash generation and earnings quality. They see this as important for sustaining the revised target range.

Some bullish analysts argue that using a lower future P/E in their models still results in a price target above the current level. They interpret this as room for valuation upside if the company meets its revenue and margin assumptions.

Curious how modest top line assumptions still support that higher fair value? The narrative emphasizes margin strength, cash generation and a re rated earnings multiple. The exact mix of these drivers might surprise you.

Result: Fair Value of $462.67 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this upbeat fair value story still leans heavily on the raised 2026 guidance and on continued success in renewing a handful of large licensing deals.

Find out about the key risks to this InterDigital narrative.

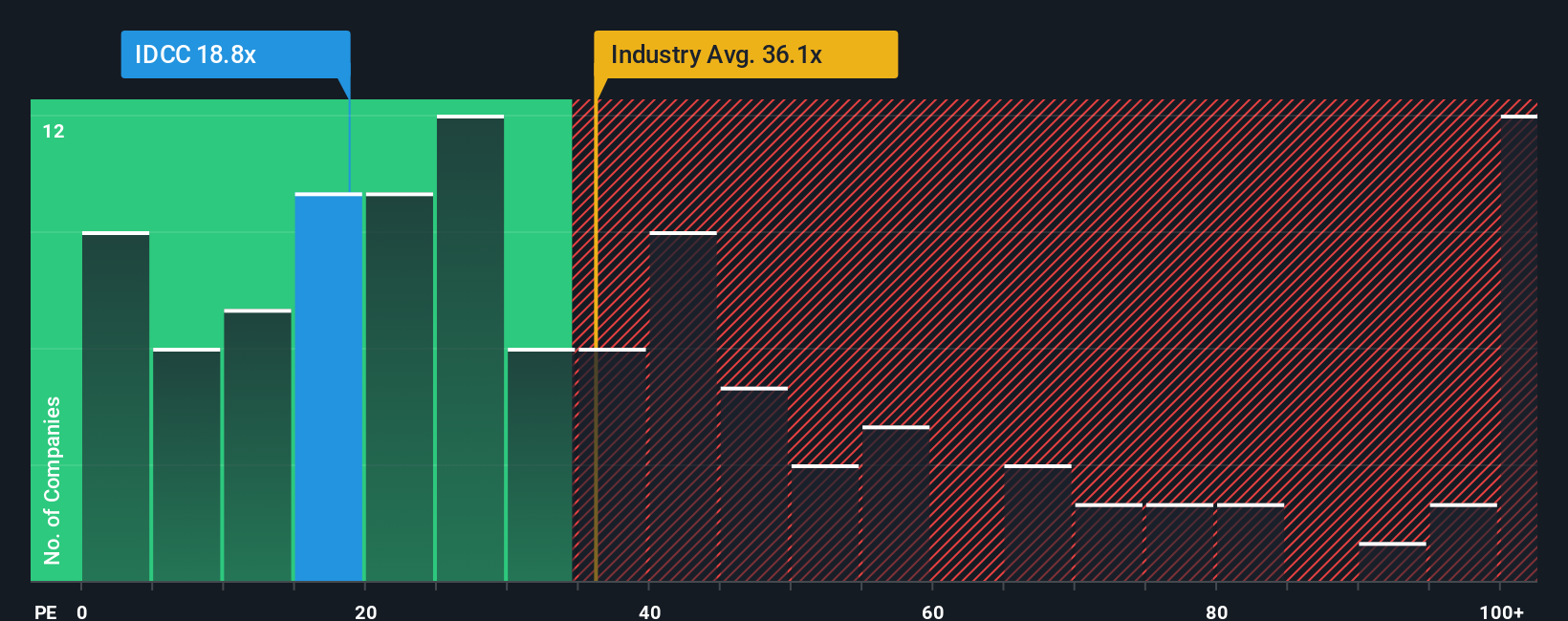

Another Angle: Multiples Point to a Richer Price

That 19.8% undervalued fair value hinges on narrative assumptions, but the current P/E of 23.4x paints a more cautious picture. It sits below the US Software industry at 26.9x, yet above both peers and the fair ratio, each at 22.3x. That premium suggests less room for error if earnings disappoint. Which signal do you put more weight on: the narrative gap or the P/E premium?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own InterDigital Narrative

If you see the story differently or prefer to rely on your own view, you can stress test the same data and build a custom perspective in minutes, Do it your way.

A great starting point for your InterDigital research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Ready to Hunt for Your Next Idea?

If InterDigital has sharpened your appetite for opportunities, do not stop here; broaden your watchlist with fresh ideas tailored to different risk and return preferences.

- Target potential value opportunities by checking companies our screener flags as 52 high quality undervalued stocks with solid fundamentals backing their current pricing.

- Strengthen your income focus by reviewing companies in our list of 14 dividend fortresses that combine higher yields with resilience potential.

- Protect your capital first by scanning the 82 resilient stocks with low risk scores that our models suggest have more resilient risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:IDCC

InterDigital

Operates as a global research and development company focuses on wireless, visual, artificial intelligence (AI), and related technologies.

Flawless balance sheet with proven track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

VA

valuebull on Eva Live ·

Is this the AI replacing marketing professionals?

Fair Value:US$7.4346.3% undervalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

ZA

ZayaanS on Pro Medicus ·

Pro Medicus: The Market Is Confusing a Lumpy Quarter With a Broken Business

Fair Value:AU$196.7841.0% undervalued

22 followersusers have followed this narrative

4 commentsusers have commented on this narrative

17 likesusers have liked this narrative

ST

SteveGruber on Warner Bros. Discovery ·

The Rising Deal Risk That Helped Sink Netflix’s $72 Billion Bid for Warner Bros. Discovery

Fair Value:US$18.1755.2% overvalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

PD

pdixit1 on Vertiv Holdings Co ·

The Infrastructure AI Cannot Be Built Without

Fair Value:US$408.6440.2% undervalued

25 followersusers have followed this narrative

2 commentsusers have commented on this narrative

13 likesusers have liked this narrative

Recently Updated Narratives

DO

Double_Bubbler on EnSilica ·

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value:UK£590.0% undervalued

120 followersusers have followed this narrative

17 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

AnimalDoctorKwon on Inotiv ·

Inotiv NAMs Test Center

Fair Value:US$1.276.3% undervalued

24 followersusers have followed this narrative

2 commentsusers have commented on this narrative

1 likeusers have liked this narrative

VE

Vestra on Credo Technology Group Holding ·

Credo Technology Group (CRDO): High-Speed Growth Meets Margin Compression in 2026.

Fair Value:US$174.944.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

DA

davidlsander on Ubisoft Entertainment ·

Is Ubisoft the Market’s Biggest Pricing Error? Why Forensic Value Points to €33 Per Share

Fair Value:€33.888.0% undervalued

65 followersusers have followed this narrative

5 commentsusers have commented on this narrative

28 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$59632.2% undervalued

1298 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.377.0% undervalued

48 followersusers have followed this narrative

3 commentsusers have commented on this narrative

27 likesusers have liked this narrative