Advertisement

- United States

- /

- Software

- /

- NasdaqGS:GTLB

After Leaping 29% GitLab Inc. (NASDAQ:GTLB) Shares Are Not Flying Under The Radar

The GitLab Inc. (NASDAQ:GTLB) share price has done very well over the last month, posting an excellent gain of 29%. Longer-term shareholders would be thankful for the recovery in the share price since it's now virtually flat for the year after the recent bounce.

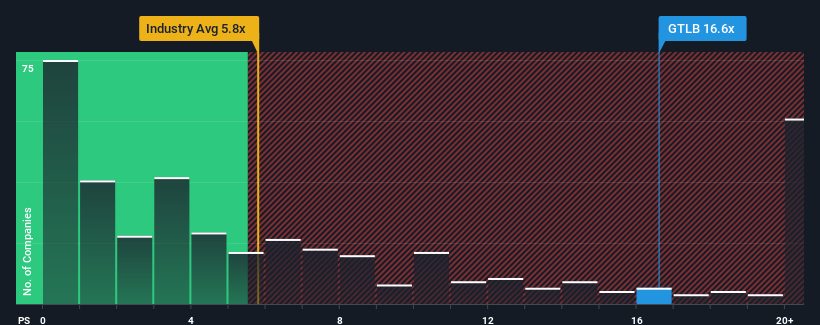

Following the firm bounce in price, GitLab may be sending very bearish signals at the moment with a price-to-sales (or "P/S") ratio of 16.6x, since almost half of all companies in the Software industry in the United States have P/S ratios under 5.8x and even P/S lower than 2x are not unusual. However, the P/S might be quite high for a reason and it requires further investigation to determine if it's justified.

See our latest analysis for GitLab

What Does GitLab's P/S Mean For Shareholders?

GitLab certainly has been doing a good job lately as it's been growing revenue more than most other companies. It seems the market expects this form will continue into the future, hence the elevated P/S ratio. However, if this isn't the case, investors might get caught out paying too much for the stock.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on GitLab.What Are Revenue Growth Metrics Telling Us About The High P/S?

There's an inherent assumption that a company should far outperform the industry for P/S ratios like GitLab's to be considered reasonable.

If we review the last year of revenue growth, the company posted a terrific increase of 32%. The latest three year period has also seen an excellent 222% overall rise in revenue, aided by its short-term performance. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Looking ahead now, revenue is anticipated to climb by 23% per year during the coming three years according to the analysts following the company. Meanwhile, the rest of the industry is forecast to only expand by 20% per year, which is noticeably less attractive.

In light of this, it's understandable that GitLab's P/S sits above the majority of other companies. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Bottom Line On GitLab's P/S

GitLab's P/S has grown nicely over the last month thanks to a handy boost in the share price. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

Our look into GitLab shows that its P/S ratio remains high on the merit of its strong future revenues. It appears that shareholders are confident in the company's future revenues, which is propping up the P/S. It's hard to see the share price falling strongly in the near future under these circumstances.

Having said that, be aware GitLab is showing 3 warning signs in our investment analysis, and 1 of those doesn't sit too well with us.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:GTLB

GitLab

Develops software for the software development lifecycle in the United States, Europe, and the Asia Pacific.

Flawless balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Cue Biopharma ·

Cue Biopharma (NASDAQ: CUE): The Scientist Behind Xolair Just Gave Cue a Next-Generation Shot at the Same Multi-Billion-Dollar Market

Fair Value:US$7058.5% undervalued

21 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$317.222.8% undervalued

9 followersusers have followed this narrative

4 commentsusers have commented on this narrative

6 likesusers have liked this narrative

NI

niteco on Broadcom ·

A Capital Allocation Favorite with Structural Importance

Fair Value:US$651.0539.1% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TO

Tokyo on Okta ·

Good foundation, but now it's all about the next steps

Fair Value:US$15122.6% undervalued

82 followersusers have followed this narrative

7 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Recently Updated Narratives

WA

waioa on Tanco Holdings Berhad ·

Tanco's Pullback Brings Key Accumulation Zones Into Focus

Fair Value:RM 1.855.6% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

AntonioS on IDP Education ·

IDP Education Limited (ASX: IEL) - A contrarian Review

Fair Value:AU$4.6254.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

REElax on Volta Metals ·

Springer REE deposit valuation

Fair Value:CA$3.595.0% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7449.0% undervalued

58 followersusers have followed this narrative

0 commentsusers have commented on this narrative

15 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9723.3% undervalued

57 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1933.9% undervalued

48 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

Trending Discussion

SI

Simply Wall St User on Access Holdings ·

It's wonderful. It has greatly helped me take informed decisions.

1

|0

SI

singhappily on Space Exploration Technologies ·

I wish there exists a time in my life, where Musk's companies are valued by fundamentals :D It's all...

0

|0