Advertisement

- United States

- /

- Software

- /

- NasdaqGS:EVCM

We Like These Underlying Return On Capital Trends At EverCommerce (NASDAQ:EVCM)

If we want to find a potential multi-bagger, often there are underlying trends that can provide clues. Typically, we'll want to notice a trend of growing return on capital employed (ROCE) and alongside that, an expanding base of capital employed. This shows us that it's a compounding machine, able to continually reinvest its earnings back into the business and generate higher returns. So on that note, EverCommerce (NASDAQ:EVCM) looks quite promising in regards to its trends of return on capital.

What Is Return On Capital Employed (ROCE)?

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. Analysts use this formula to calculate it for EverCommerce:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.0062 = US$8.8m ÷ (US$1.5b - US$117m) (Based on the trailing twelve months to December 2023).

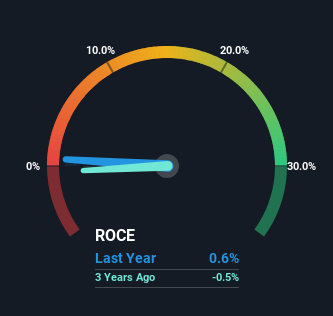

Therefore, EverCommerce has an ROCE of 0.6%. In absolute terms, that's a low return and it also under-performs the Software industry average of 7.2%.

View our latest analysis for EverCommerce

Above you can see how the current ROCE for EverCommerce compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like, you can check out the forecasts from the analysts covering EverCommerce for free.

What Does the ROCE Trend For EverCommerce Tell Us?

We're delighted to see that EverCommerce is reaping rewards from its investments and is now generating some pre-tax profits. Shareholders would no doubt be pleased with this because the business was loss-making four years ago but is is now generating 0.6% on its capital. And unsurprisingly, like most companies trying to break into the black, EverCommerce is utilizing 61% more capital than it was four years ago. This can indicate that there's plenty of opportunities to invest capital internally and at ever higher rates, both common traits of a multi-bagger.

What We Can Learn From EverCommerce's ROCE

In summary, it's great to see that EverCommerce has managed to break into profitability and is continuing to reinvest in its business. And since the stock has fallen 24% over the last year, there might be an opportunity here. With that in mind, we believe the promising trends warrant this stock for further investigation.

Before jumping to any conclusions though, we need to know what value we're getting for the current share price. That's where you can check out our FREE intrinsic value estimation for EVCM that compares the share price and estimated value.

For those who like to invest in solid companies, check out this free list of companies with solid balance sheets and high returns on equity.

Valuation is complex, but we're here to simplify it.

Discover if EverCommerce might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:EVCM

EverCommerce

Provides integrated software-as-a-service solutions for service-based small and medium-sized businesses in the United States and internationally.

Adequate balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

VA

valuebull on Eva Live ·

Is this the AI replacing marketing professionals?

Fair Value:US$7.4346.7% undervalued

13 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

ZA

ZayaanS on Pro Medicus ·

Pro Medicus: The Market Is Confusing a Lumpy Quarter With a Broken Business

Fair Value:AU$196.7838.3% undervalued

25 followersusers have followed this narrative

4 commentsusers have commented on this narrative

18 likesusers have liked this narrative

ST

SteveGruber on Warner Bros. Discovery ·

The Rising Deal Risk That Helped Sink Netflix’s $72 Billion Bid for Warner Bros. Discovery

Fair Value:US$18.1753.8% overvalued

5 followersusers have followed this narrative

1 commentusers have commented on this narrative

3 likesusers have liked this narrative

PD

pdixit1 on Vertiv Holdings Co ·

The Infrastructure AI Cannot Be Built Without

Fair Value:US$408.6438.5% undervalued

31 followersusers have followed this narrative

3 commentsusers have commented on this narrative

13 likesusers have liked this narrative

Recently Updated Narratives

AN

andre_santos on Realty Income ·

Realty Income - A Fundamental and Historical Valuation

Fair Value:US$73.4610.2% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

HP

HpN on Microsoft ·

A Structured Counter‑Analysis of "The Leaking Dreadnought"

Fair Value:US$509.8220.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on Alphabet ·

Alphabet Inc. (GOOG): The Gemini Era – Consolidating AI Dominance in 2026.

Fair Value:US$35514.6% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

DA

davidlsander on Ubisoft Entertainment ·

Is Ubisoft the Market’s Biggest Pricing Error? Why Forensic Value Points to €33 Per Share

Fair Value:€33.888.0% undervalued

65 followersusers have followed this narrative

5 commentsusers have commented on this narrative

28 likesusers have liked this narrative

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.376.7% undervalued

48 followersusers have followed this narrative

3 commentsusers have commented on this narrative

27 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$59632.0% undervalued

1299 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative