Advertisement

- United States

- /

- IT

- /

- NasdaqGS:DOX

Is There Now an Opportunity in Amdocs After Recent Share Price Weakness?

Reviewed by Bailey Pemberton

- Wondering if Amdocs is quietly turning into a value opportunity while everyone is chasing the latest hype stock? You are not alone, and this is exactly what we are going to unpack.

- Despite a choppy year where the share price is down 4.4% year to date and 5.3% over the last 12 months, the stock has started to firm up recently, with a 1.4% gain over the past week and 6.8% over the last month.

- Much of this price action has been shaped by ongoing contract wins and renewals with major telecom operators, along with continued investment in 5G and cloud based customer experience platforms that keep Amdocs embedded in clients’ critical systems. On top of that, the market has been paying closer attention to software names that generate recurring revenue and strong cash flows. This puts a spotlight on how fairly, or unfairly, Amdocs might be priced today.

- On our framework Amdocs currently scores a 6/6 valuation score, indicating it screens as undervalued across every one of our six checks. In the sections that follow, we will walk through traditional valuation methods like DCFs and multiples, before finishing with a more intuitive way to tie those numbers back to Amdocs long term narrative.

Find out why Amdocs's -5.3% return over the last year is lagging behind its peers.

Approach 1: Amdocs Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow model estimates what a business is worth today by projecting its future cash flows and discounting them back to a present value. For Amdocs, this is done using a 2 Stage Free Cash Flow to Equity approach, which first relies on analyst forecasts and then tapers growth to more conservative long term assumptions.

Amdocs generated last twelve month free cash flow of about $644 Million, and analysts see this rising steadily over the rest of the decade, with projections reaching roughly $961 Million by 2030. Beyond the explicit analyst window, Simply Wall St extrapolates cash flows using gradually slowing growth rates to avoid overly aggressive assumptions.

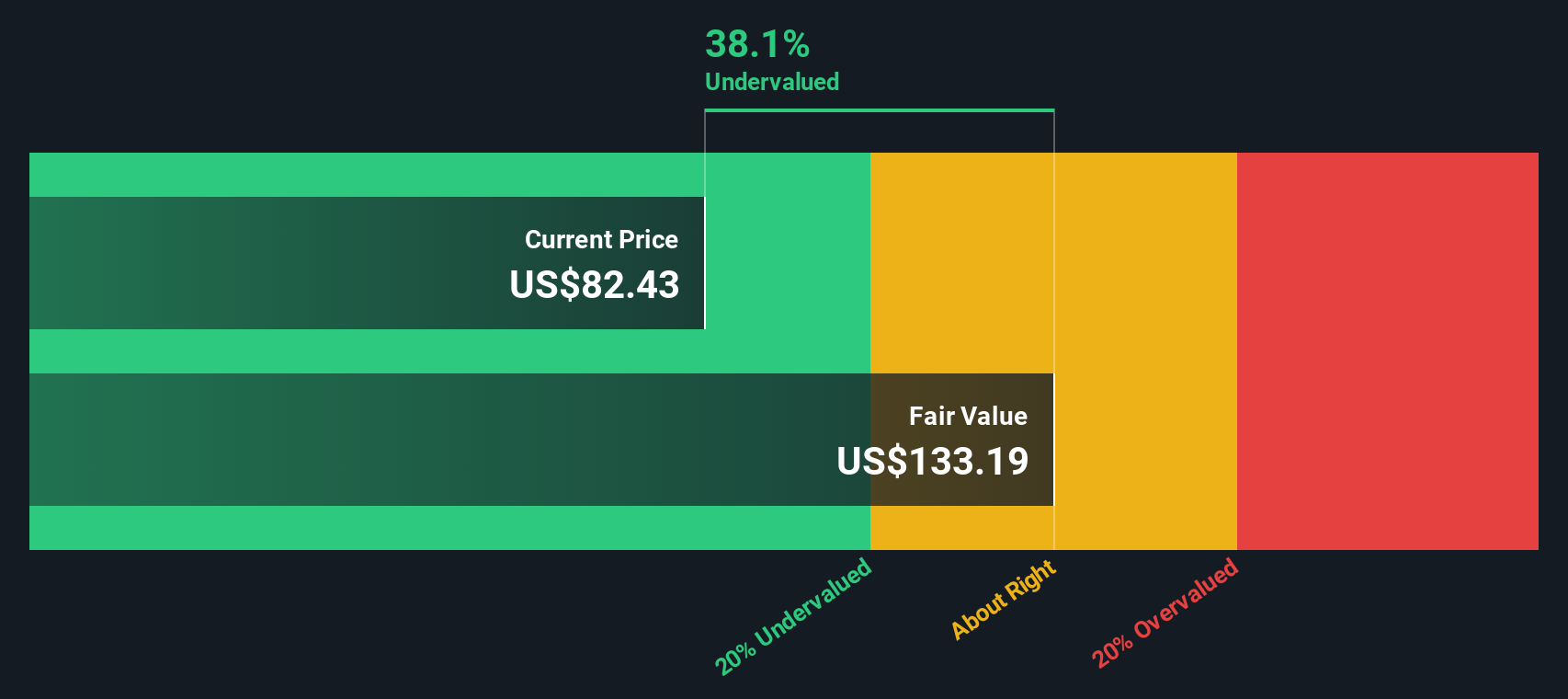

Pulling those cash flows back to today gives an estimated intrinsic value of about $130.82 per share. Based on the current market price, this implies the stock is roughly 38.5% undervalued. This suggests investors are paying materially less than what the long term cash generation would justify.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Amdocs is undervalued by 38.5%. Track this in your watchlist or portfolio, or discover 913 more undervalued stocks based on cash flows.

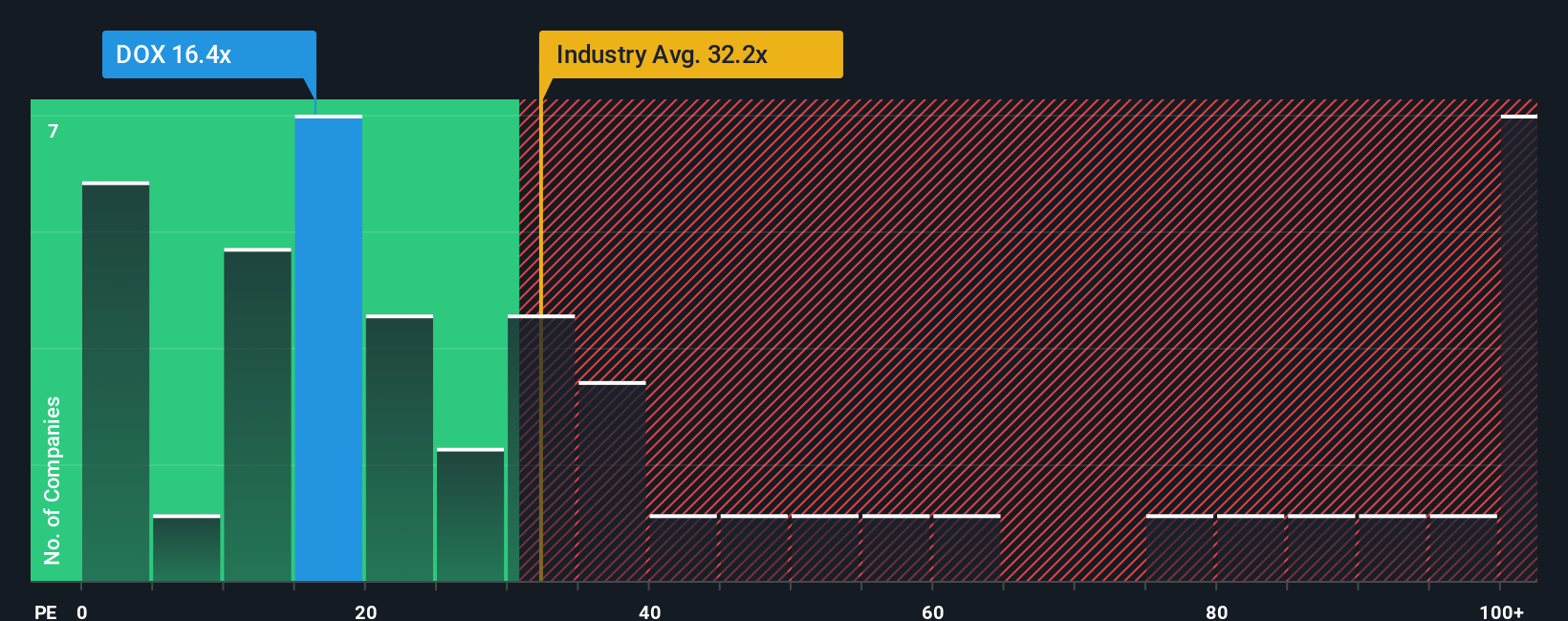

Approach 2: Amdocs Price vs Earnings

For consistently profitable businesses like Amdocs, the price to earnings, or PE, ratio is a practical way to judge valuation because it directly links what investors pay to the profits the company generates today. In general, companies with stronger growth prospects and lower perceived risk can justify a higher PE, while slower growth or higher risk usually call for a lower, more conservative multiple.

Amdocs currently trades on a PE of about 15.4x, which is below both its IT industry average of roughly 29.8x and the peer group average of around 18.5x. Simply Wall St also calculates a Fair Ratio of about 24.4x for Amdocs, a proprietary estimate of what its PE should be given its earnings growth outlook, margins, industry, size and risk profile. This Fair Ratio is more tailored than a simple comparison to peers or the sector, because it adjusts for Amdocs specific strengths and risk factors rather than assuming all software and IT names deserve the same multiple. With the shares at 15.4x compared with a Fair Ratio of 24.4x, the stock appears attractively priced on earnings.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1463 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Amdocs Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple way to connect your view of a company with the numbers behind it. A Narrative is your story about Amdocs, expressed as assumptions for future revenue, earnings and margins, which then feeds into a financial forecast and an estimated fair value. On Simply Wall St, millions of investors build and explore Narratives on the Community page, using them as an easy, accessible tool to see how different assumptions change a company’s valuation. Narratives can be used to compare your fair value estimate to today’s share price, and they update dynamically as new information like earnings, guidance or major contract wins comes in. For example, one Amdocs Narrative on Simply Wall St assumes revenue will grow around 2.8% annually with margins rising above 19% and a fair value near $104 per share, while another more cautious view bakes in slower cloud adoption, softer margins and a meaningfully lower fair value.

Do you think there's more to the story for Amdocs? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:DOX

Amdocs

Through its subsidiaries, provides software and services to communications, entertainment, media, and other service providers worldwide.

Very undervalued with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Gain Therapeutics ·

The Market Is Sleeping on This Parkinson's Biotech - And I Think That's a Mistake

Fair Value:US$7.675.4% undervalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

11 likesusers have liked this narrative

KI

Kingman1152 on NVIDIA ·

NVIDIA will see a profit margin surge of 55% in the next 5 years

Fair Value:US$305.2538.0% undervalued

14 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

TE

TechMegaTrends on Bambuser ·

Bambuser is today the only listed company in Europe that simultaneously possesses an 85% gross margin, proprietary AI infrastructure for the

Fair Value:SEK 238.2690.3% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

HE

HedgeY on Constellium ·

Constellium jet another cyclical aluminum processor, or a mispriced aluminum platform?

Fair Value:US$3410.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

AS

AstrisCorporateAdvisory on SAN Holdings ·

Forging ahead with an ambitious growth plan

Fair Value:JP¥1.92k28.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FA

FA_Trader on Verdant Solar Holdings Berhad ·

Verdant Solar: Continued share accumulation may be hinting that the worst is temporary, not structural

Fair Value:RM 0.4555.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DI

DinTang on Bumitama Agri ·

Expectations focused on stable output, disciplined costs, and continued cash returns to shareholders

Fair Value:S$2.4622.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TR

tripledub on Microsoft ·

Everyone's Terrified Microsoft Will Keep Spending. I'm Terrified They'll Stop.

Fair Value:US$3952.7% undervalued

45 followersusers have followed this narrative

3 commentsusers have commented on this narrative

42 likesusers have liked this narrative

RO

Robbo on Tesla ·

The academically fascinating Tesla

Fair Value:US$301.1k% overvalued

38 followersusers have followed this narrative

11 commentsusers have commented on this narrative

32 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$587.3134.6% undervalued

1356 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative