Advertisement

- United States

- /

- IT

- /

- NasdaqGS:DOX

Is Amdocs (DOX) Now An Opportunity After Recent Share Price Weakness?

Reviewed by Bailey Pemberton

- If you are wondering whether Amdocs at around US$73 is a bargain or a value trap, you are asking the right question for this stock right now.

- The share price is at US$73.06, with returns of a 10.7% decline over the last week, a 9.8% decline over the last month, an 8.9% decline year to date, a 15.0% decline over 1 year, and a 4.2% gain over 5 years. These moves could change how investors view both risk and opportunity.

- Recent coverage of Amdocs has focused on its role as a software and services provider to telecom and media companies, and how that positioning fits into long term digital transformation trends. This context is important when thinking about why some investors may be reassessing what they are willing to pay for the stock today.

- On our checks, Amdocs scores 6 out of 6 for being undervalued across key metrics. Next we will look at how different valuation approaches line up on that view before finishing with a broader way to think about what the current price really offers.

Find out why Amdocs's -15.0% return over the last year is lagging behind its peers.

Approach 1: Amdocs Discounted Cash Flow (DCF) Analysis

A discounted cash flow, or DCF, model takes estimates of the cash a business could generate in the future and discounts those cash flows back to today to arrive at an estimate of what the entire company might be worth now.

For Amdocs, the model uses a 2 Stage Free Cash Flow to Equity approach. The latest twelve month free cash flow is about $758.0 million, and analysts and extrapolated estimates put projected free cash flow at $956.5 million in 2030. Simply Wall St provides a detailed path between those points, with annual projections in the hundreds of millions of dollars, all expressed in $ and discounted back to today using the DCF framework.

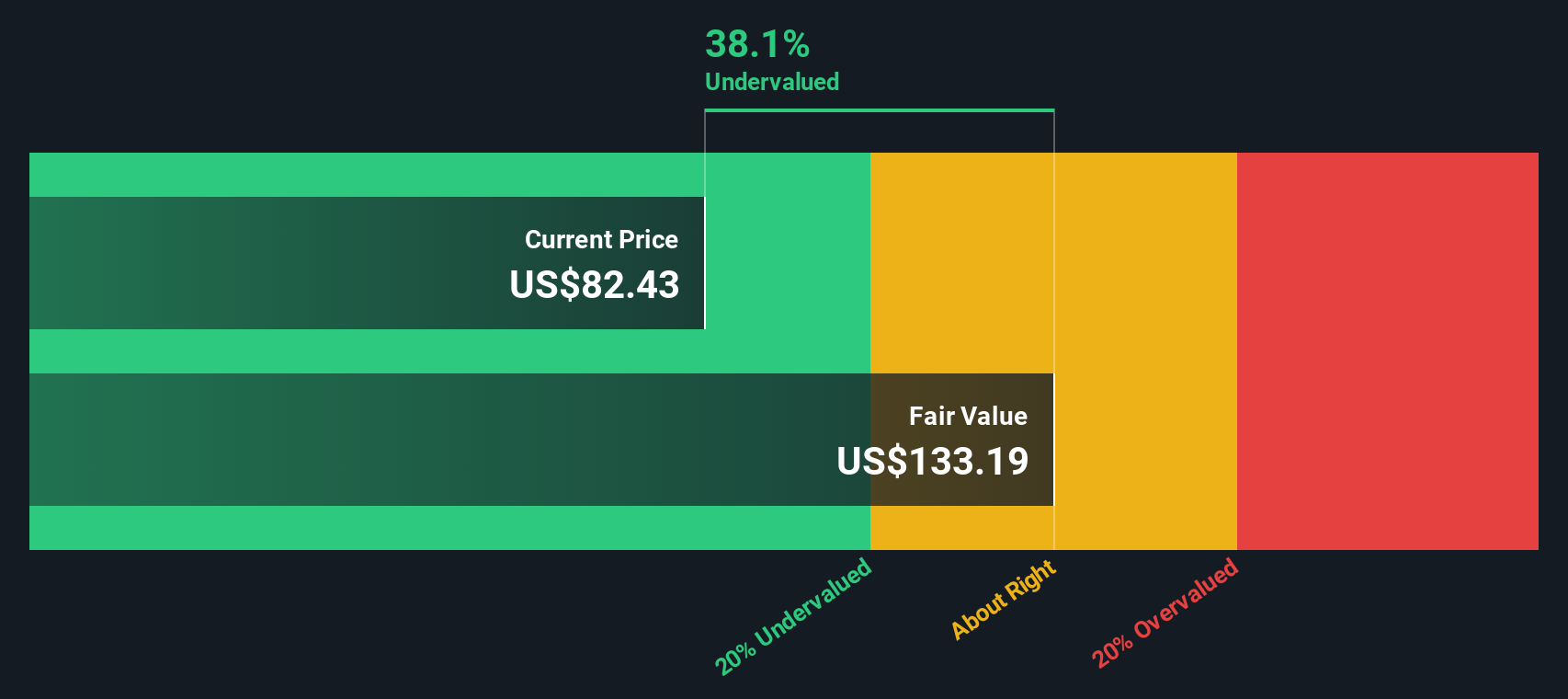

On this basis, the estimated intrinsic value comes out at about $132.92 per share, compared with the current share price of around $73.06. That implies the stock is trading at roughly a 45.0% discount to this DCF estimate, which is a substantial gap for a cash flow driven model.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Amdocs is undervalued by 45.0%. Track this in your watchlist or portfolio, or discover 868 more undervalued stocks based on cash flows.

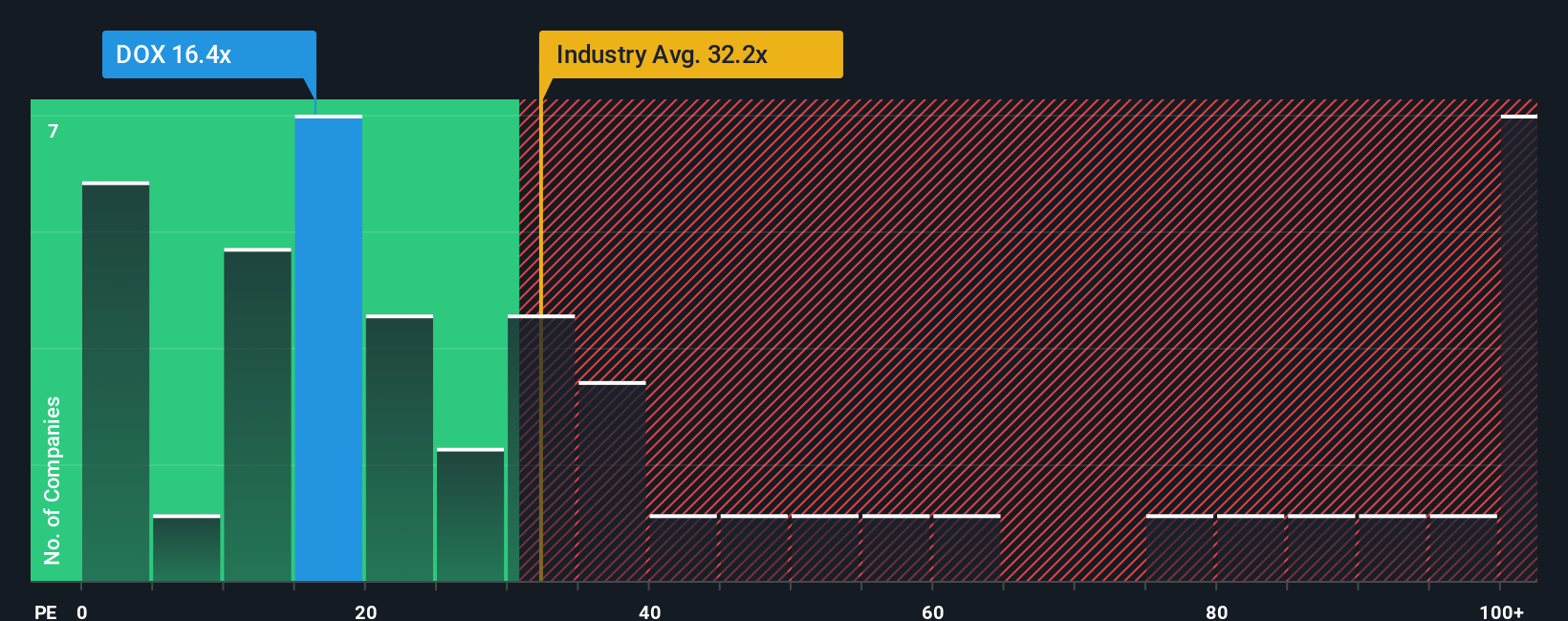

Approach 2: Amdocs Price vs Earnings

For a profitable company like Amdocs, the P/E ratio is a useful way to connect what you pay for each share with the earnings that support it. In simple terms, a “normal” or “fair” P/E tends to be higher when investors expect stronger earnings growth and are comfortable with the company’s risk profile, and lower when growth expectations are more modest or risks are higher.

Amdocs currently trades on a P/E of 13.8x. That sits below both the IT industry average P/E of 26.1x and a peer group average of 14.8x, which indicates that the market is pricing Amdocs at a discount to many similar businesses. Simply Wall St’s “Fair Ratio” for Amdocs is 24.5x, which is its proprietary view of what the P/E might be given factors such as earnings growth, industry, profit margin, market cap and identified risks.

The Fair Ratio adds context that simple peer or industry comparisons cannot, because it is tailored to Amdocs rather than applying a broad sector multiple. Comparing the current P/E of 13.8x with the Fair Ratio of 24.5x suggests the shares are trading meaningfully below that tailored benchmark.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1426 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Amdocs Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. Narratives let you attach a clear story to your numbers, including your view of fair value and your expectations for Amdocs’ future revenue, earnings and margins.

A Narrative is simply your own written perspective on the company that connects what Amdocs does, how you think its business will develop, and what that means for a financial forecast and a fair value per share. On Simply Wall St, Narratives live in the Community page, where millions of investors can create and compare these story plus forecast views using the same framework. Each Narrative translates your assumptions into a Fair Value that you can line up against the current market price, which can help you consider whether you see Amdocs as closer to a potential buy, hold, or sell. Narratives update automatically when new information such as earnings or news is added, so your fair value view stays aligned with the latest data. For example, one Amdocs Narrative on the Community page might reflect a much higher fair value than another that takes a more cautious stance on future growth and profitability.

Do you think there's more to the story for Amdocs? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:DOX

Amdocs

Through its subsidiaries, provides software and services to communications, entertainment, media, and other service providers worldwide.

6 star dividend payer and undervalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2540.0% undervalued

84 followersusers have followed this narrative

0 commentsusers have commented on this narrative

22 likesusers have liked this narrative

HE

HedgeY on IonQ ·

The Best-Funded Quantum Platform and Still a Stock Priced for Perfection

Fair Value:US$482.3% overvalued

33 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5450.7% undervalued

56 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

IV

Ivoed on Netflix ·

Netflix’s Business Quality Is Clear. The Harder Question Is Whether The Stock Is Still Cheap

Fair Value:US$825.3% undervalued

28 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative

Recently Updated Narratives

SO

Solvent_Octopus_mwbl on CRDB Bank ·

Is the Market Underestimating CRDB?

Fair Value:TSh2.8k1.4% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.917.0% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DR

DrPotato on TeamViewer ·

TeamViewer Set to Evolve from Stagnation to Enterprise Growth by 2028

Fair Value:€13.3260.9% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75028.1% undervalued

82 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9631.3% undervalued

63 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

NI

niteco on Broadcom ·

A Capital Allocation Favorite with Structural Importance

Fair Value:US$651.0544.6% undervalued

56 followersusers have followed this narrative

0 commentsusers have commented on this narrative

13 likesusers have liked this narrative

Trending Discussion

PR

ProjectKai on Iovance Biotherapeutics ·

Polip, this is Kai. When do you estimate IOVA could reach a $12–20 billion valuation, implying rough...

0

|0