Advertisement

- United States

- /

- Software

- /

- NasdaqGS:DOCU

Is It Time To Revisit DocuSign (DOCU) After Its Multi‑Year Share Price Slide?

Reviewed by Bailey Pemberton

- Wondering if DocuSign at around US$45.71 is a bargain or still pricing in big expectations? This article walks through what the current share price might be implying about value.

- The stock has had a mixed run, with a 1.4% return over 30 days, a 29.5% decline year to date, and a 43.8% decline over the last year. These moves can change how the market views both risk and potential reward.

- Recent coverage has focused on DocuSign's position in digital agreements and how investors are reassessing software names that previously traded on higher expectations. This backdrop helps explain why a stock that is down 77.8% over five years and 21.3% over three years can still attract fresh interest from investors looking for potential mispriced opportunities.

- Simply Wall St currently gives DocuSign a valuation score of 4 out of 6. The rest of this article will unpack what different valuation methods say about that score and introduce one more way to think about value at the end.

Find out why DocuSign's -43.8% return over the last year is lagging behind its peers.

Approach 1: DocuSign Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a company may be worth by projecting the cash it could generate in the future and then discounting those cash flows back to today using a required return. It is essentially asking what those future dollars are worth in current terms.

For DocuSign, the model used is a 2 Stage Free Cash Flow to Equity approach. The latest twelve months Free Cash Flow sits at about US$1.06b. Simply Wall St then uses analyst estimates for several years and extends them further out, with projected Free Cash Flow of US$1.37b in the year to 2029. Beyond the explicit analyst window, the ten year path of cash flows is extrapolated using more moderate growth assumptions.

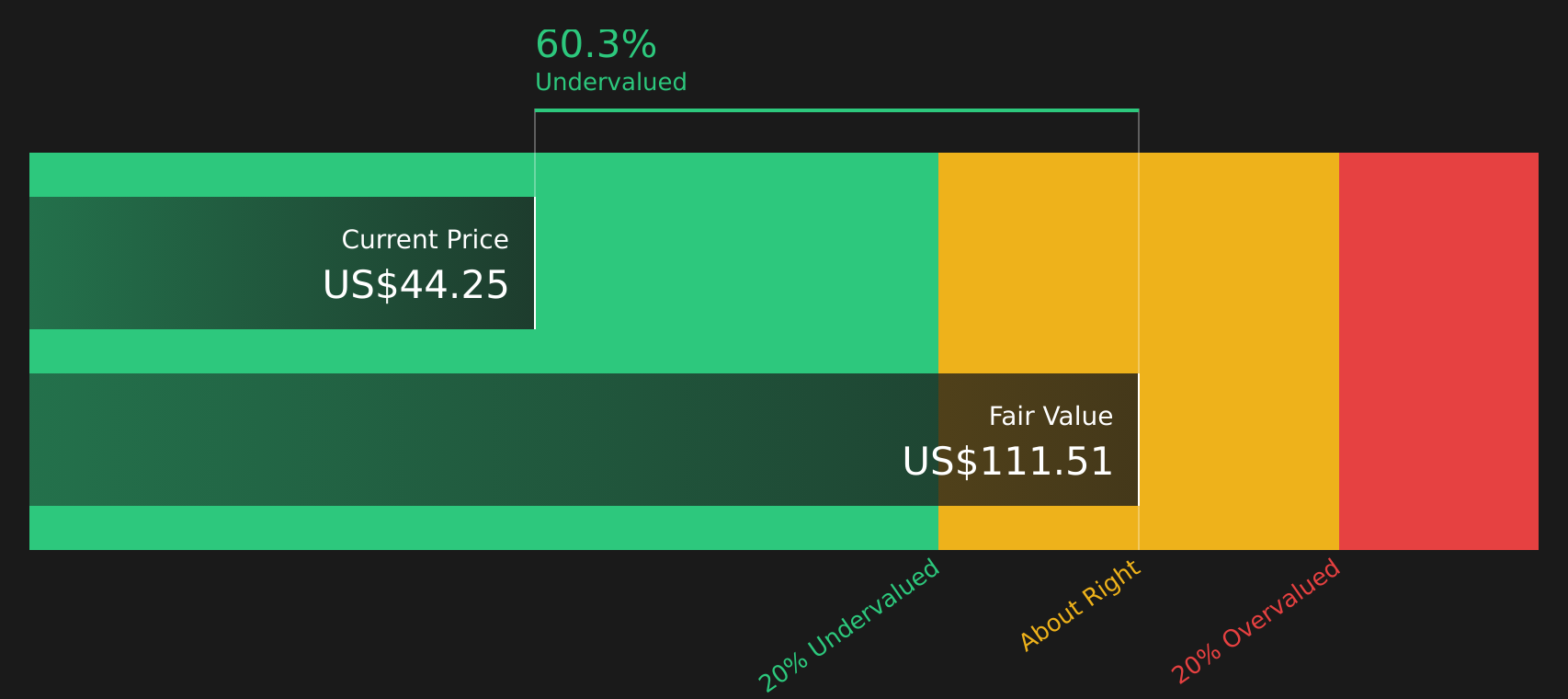

When all of those projected cash flows are discounted back, the DCF model arrives at an estimated intrinsic value of about US$132.99 per share. Against a share price of around US$45.71, this implies a 65.6% discount, which suggests the shares screen as materially undervalued on this method alone.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests DocuSign is undervalued by 65.6%. Track this in your watchlist or portfolio, or discover 62 more high quality undervalued stocks.

Approach 2: DocuSign Price vs Earnings

For a company that is already profitable, the P/E ratio is a useful way to think about value because it connects what you pay today with the earnings the business is currently generating. A higher or lower P/E often reflects what the market assumes about future growth and risk, with faster growth or perceived stability usually justifying a richer multiple, and higher risk or weaker growth supporting a lower one.

DocuSign currently trades on a P/E of about 28.8x. That sits close to both the Software industry average P/E of about 28.2x and the peer average of around 32.1x, which suggests the market is not treating DocuSign as a clear outlier on simple comparisons. Simply Wall St also calculates a proprietary “Fair Ratio” for DocuSign of 29.5x, which is the P/E that would typically be expected given its earnings growth profile, industry, profit margins, market cap and key risk factors.

This Fair Ratio is more tailored than a basic peer or industry comparison because it adjusts for DocuSign specific characteristics rather than assuming all software companies deserve the same multiple. With the actual P/E at 28.8x and the Fair Ratio at 29.5x, the stock screens as slightly undervalued on this metric.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your DocuSign Narrative

Earlier it was mentioned that there is an even better way to understand valuation, so Narratives are introduced as a simple way for you to attach a story about DocuSign to the hard numbers. This links your view on its future revenue, earnings and margins to a Fair Value estimate that can then be compared with the current share price on Simply Wall St's Community page, where millions of investors share scenarios that update automatically as news or earnings arrive. For example, a bullish DocuSign Narrative might lean toward a Fair Value around US$117.02, while a cautious one might sit closer to US$53.00. This gives you a clear, number backed framework for deciding whether the price you see today lines up with the story you believe.

Do you think there's more to the story for DocuSign? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:DOCU

DocuSign

Provides electronic signature solution in the United States and internationally.

Excellent balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.562.8% undervalued

25 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

73 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56052.2% undervalued

64 followersusers have followed this narrative

4 commentsusers have commented on this narrative

30 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2780.9% undervalued

36 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

AN

Anthony_Lee on Geohan Corporation Berhad ·

Geohan's Growth Outlook Brightens on Expanding Order Book and Easing Cost Pressures

Fair Value:RM 0.7461.5% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

danmad on CSL ·

Strong buy. World-leading healthcare company with steady growth

Fair Value:AU$143.1519.8% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on Orezone Gold ·

Orezone Gold Could 3X–5X, Bomboré Ramp + Casa Berardi Quebec Asset Delivers 160-180Koz in 2026

Fair Value:CA$10.6878.4% undervalued

13 followersusers have followed this narrative

4 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

73 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9636.6% undervalued

62 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7442.1% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative