Advertisement

- United States

- /

- Software

- /

- NasdaqGS:DOCU

Is DocuSign (DOCU) Offering Value After Recent Share Price Weakness?

Reviewed by Bailey Pemberton

- Wondering whether DocuSign at around US$46.82 still lines up with what you would consider a fair price? This article walks through the key valuation checks so you can put the current share price in context.

- The stock has seen a mixed run recently, with a 3.8% decline over the last 7 days, a 4.5% gain over the last 30 days, and year to date and 1 year returns of 27.8% and 43.9% declines respectively.

- Recent headlines have continued to focus on DocuSign's role in digital agreement workflows and how that position fits into broader software sector sentiment. This backdrop helps explain why some investors see the recent share price swings as a changing assessment of both risk and long term potential rather than just short term noise.

- DocuSign currently has a valuation score of 3 out of 6, and the rest of this article will unpack what that means across different valuation methods and point to one more powerful way to think about value at the end.

Find out why DocuSign's -43.9% return over the last year is lagging behind its peers.

Approach 1: DocuSign Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a company might be worth by projecting its future cash flows and then discounting those back to today, so you can compare that value to the current share price.

For DocuSign, the model used is a 2 Stage Free Cash Flow to Equity approach based on cash flow projections. The latest twelve month free cash flow sits at about $990.3 million. Analyst inputs and Simply Wall St extrapolations point to free cash flow of $1,203.6 million in 2028, with a full set of annual projections out to 2035 used to build the valuation.

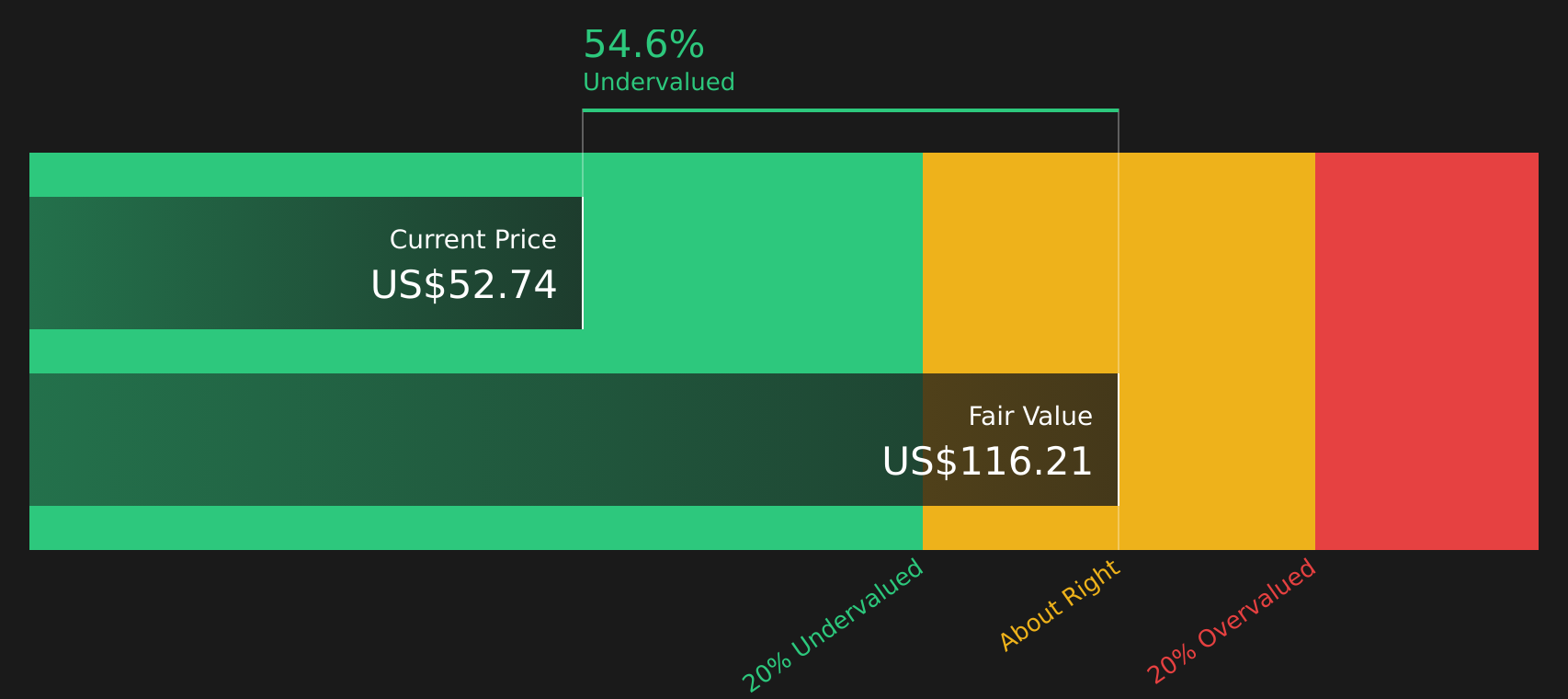

Putting those cash flows together and discounting them back results in an estimated intrinsic value of $118.88 per share, compared with a current share price of about $46.82. On this model, the stock screens as around 60.6% undervalued.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests DocuSign is undervalued by 60.6%. Track this in your watchlist or portfolio, or discover 47 more high quality undervalued stocks.

Approach 2: DocuSign Price vs Earnings

For profitable companies, the P/E ratio is a useful shorthand because it links what you are paying directly to the earnings the business is already generating. It helps you see how many dollars of share price the market is assigning to each dollar of earnings.

What counts as a reasonable P/E depends on how the market views a company’s growth potential and risk profile. Higher growth or lower perceived risk can justify a higher P/E, while lower growth or higher risk often lines up with a lower P/E.

DocuSign currently trades on a P/E of 31.0x. That sits above the wider Software industry average P/E of about 27.8x, but below the peer group average of around 35.0x. Simply Wall St’s Fair Ratio for DocuSign is 29.4x, which is its proprietary estimate of what the P/E might be given factors such as earnings growth, margins, industry, market cap and company specific risks.

This Fair Ratio can be more informative than a simple comparison with peers or the industry, because it adjusts for DocuSign’s own characteristics rather than assuming all software names deserve the same multiple. With the current P/E of 31.0x sitting a little above the 29.4x Fair Ratio, the shares screen as slightly overvalued on this metric.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your DocuSign Narrative

Earlier it was mentioned that there is an even better way to understand valuation, so Narratives are introduced here as a simple way for you to attach a clear story about DocuSign to hard numbers like fair value, and future revenue, earnings and margin estimates, then see how that story stacks up against the current price.

A Narrative on Simply Wall St links what you think is happening with DocuSign, such as the impact of AI powered agreement tools or competition in e signature, to a financial forecast and then to a fair value, so you can quickly compare that value with the live market price and decide whether the stock looks expensive or cheap on your view.

These Narratives live in the Community page on Simply Wall St, are used by millions of investors, and update automatically as new information arrives, for example when news on DocuSign’s Intelligent Agreement Management roll out or quarterly earnings guidance is released, so your fair value view can stay aligned with the latest data without extra spreadsheet work.

For DocuSign today, one investor might align with a more optimistic Narrative that points to a fair value around US$117.02, while a more cautious investor might lean toward a fair value closer to US$53.00. Seeing both side by side helps you decide which story, and which numbers, feel more reasonable to you.

Do you think there's more to the story for DocuSign? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:DOCU

DocuSign

Provides electronic signature solution in the United States and internationally.

Excellent balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Unicycive Therapeutics ·

Looking to be second time lucky with a game-changing new product

Fair Value:US$21.5360.5% undervalued

135 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

DE

Degen_GCR on Everpure ·

Second order memory play likely to double in a year

Fair Value:US$18053.1% undervalued

19 followersusers have followed this narrative

1 commentusers have commented on this narrative

13 likesusers have liked this narrative

DO

Double_Bubbler on Intuitive Machines ·

Intuitive Machines: To The Moon and Beyond!

Fair Value:US$42.315.7% undervalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

YI

yiannisz on AppLovin ·

AppLovin’s AI Engine Is Printing Profit

Fair Value:US$989.2454.2% undervalued

30 followersusers have followed this narrative

2 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

MA

MarkoVT on COVER ·

Significant headwinds will temper expectations for FY2027

Fair Value:JP¥2.28k36.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KA

kapirey on Unicycive Therapeutics ·

Unicycive Therapeutics is a late-stage clinical biotech transitioning toward commercialization

Fair Value:US$9.177.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KA

kapirey on Guming Holdings ·

A scaled, high-growth, franchise-driven beverage leader with strong penetration in China

Fair Value:HK$47.5650.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8589.8% undervalued

108 followersusers have followed this narrative

2 commentsusers have commented on this narrative

31 likesusers have liked this narrative

KI

Kingman1152 on NVIDIA ·

NVIDIA will see a profit margin surge of 55% in the next 5 years

Fair Value:US$305.226.0% undervalued

70 followersusers have followed this narrative

2 commentsusers have commented on this narrative

24 likesusers have liked this narrative

TR

tripledub on Meta Platforms ·

The $135 Billion Bet That Should Make Every Shareholder Nervous

Fair Value:US$74016.7% undervalued

37 followersusers have followed this narrative

3 commentsusers have commented on this narrative

33 likesusers have liked this narrative