Advertisement

- United States

- /

- Software

- /

- NasdaqGS:DOCU

Do DocuSign's (NASDAQ:DOCU) Earnings Warrant Your Attention?

Investors are often guided by the idea of discovering 'the next big thing', even if that means buying 'story stocks' without any revenue, let alone profit. But as Peter Lynch said in One Up On Wall Street, 'Long shots almost never pay off.' While a well funded company may sustain losses for years, it will need to generate a profit eventually, or else investors will move on and the company will wither away.

In contrast to all that, many investors prefer to focus on companies like DocuSign (NASDAQ:DOCU), which has not only revenues, but also profits. While profit isn't the sole metric that should be considered when investing, it's worth recognising businesses that can consistently produce it.

See our latest analysis for DocuSign

DocuSign's Improving Profits

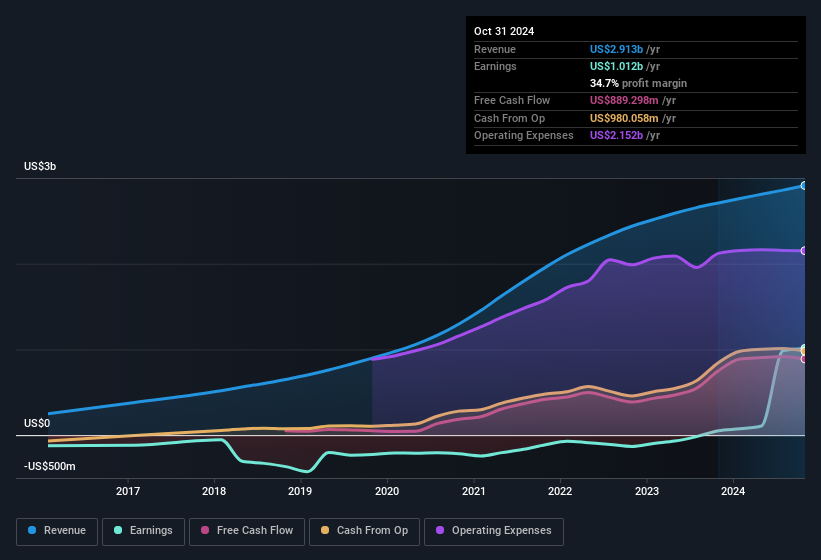

Strong earnings per share (EPS) results are an indicator of a company achieving solid profits, which investors look upon favourably and so the share price tends to reflect great EPS performance. So a growing EPS generally brings attention to a company in the eyes of prospective investors. Commendations have to be given in seeing that DocuSign grew its EPS from US$0.25 to US$5.01, in one short year. While it's difficult to sustain growth at that level, it bodes well for the company's outlook for the future.

One way to double-check a company's growth is to look at how its revenue, and earnings before interest and tax (EBIT) margins are changing. DocuSign shareholders can take confidence from the fact that EBIT margins are up from 2.0% to 6.2%, and revenue is growing. Ticking those two boxes is a good sign of growth, in our book.

In the chart below, you can see how the company has grown earnings and revenue, over time. To see the actual numbers, click on the chart.

In investing, as in life, the future matters more than the past. So why not check out this free interactive visualization of DocuSign's forecast profits?

Are DocuSign Insiders Aligned With All Shareholders?

Owing to the size of DocuSign, we wouldn't expect insiders to hold a significant proportion of the company. But we do take comfort from the fact that they are investors in the company. We note that their impressive stake in the company is worth US$203m. This suggests that leadership will be very mindful of shareholders' interests when making decisions!

Does DocuSign Deserve A Spot On Your Watchlist?

DocuSign's earnings per share growth have been climbing higher at an appreciable rate. That EPS growth certainly is attention grabbing, and the large insider ownership only serves to further stoke our interest. At times fast EPS growth is a sign the business has reached an inflection point, so there's a potential opportunity to be had here. So at the surface level, DocuSign is worth putting on your watchlist; after all, shareholders do well when the market underestimates fast growing companies. What about risks? Every company has them, and we've spotted 2 warning signs for DocuSign you should know about.

Although DocuSign certainly looks good, it may appeal to more investors if insiders were buying up shares. If you like to see companies with more skin in the game, then check out this handpicked selection of companies that not only boast of strong growth but have strong insider backing.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:DOCU

DocuSign

Provides electronic signature solution in the United States and internationally.

Excellent balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

VA

valuebull on Eva Live ·

Is this the AI replacing marketing professionals?

Fair Value:US$7.4349.5% undervalued

41 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

TR

tripledub on Microsoft ·

Everyone's Terrified Microsoft Will Keep Spending. I'm Terrified They'll Stop.

Fair Value:US$3956.3% undervalued

11 followersusers have followed this narrative

3 commentsusers have commented on this narrative

17 likesusers have liked this narrative

RO

Robbo on Tesla ·

The academically fascinating Tesla

Fair Value:US$301.1k% overvalued

21 followersusers have followed this narrative

5 commentsusers have commented on this narrative

15 likesusers have liked this narrative

AH

AHaron on Eli Lilly ·

Eli Lilly: A Pipeline-Driven Growth Story Trading 30% Below What the Business Is Actually Worth

Fair Value:US$1.48k37.7% undervalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

Recently Updated Narratives

FA

FA_Trader on Meta Bright Group Berhad ·

Meta Bright: Rising fuel costs could gradually accelerate the shift to EVs and rooftop solar

Fair Value:RM 0.1720.6% undervalued

1 followerusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

AL

alegget on Walt Disney ·

The happiest company on Earth, also perennially misunderstood.

Fair Value:US$134.6328.4% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

RE

REElax on Volta Metals ·

Springer REE deposit valuation

Fair Value:CA$3.593.7% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9830.9% undervalued

51 followersusers have followed this narrative

0 commentsusers have commented on this narrative

36 likesusers have liked this narrative

PD

pdixit1 on Vertiv Holdings Co ·

The Infrastructure AI Cannot Be Built Without

Fair Value:US$408.6438.7% undervalued

40 followersusers have followed this narrative

3 commentsusers have commented on this narrative

18 likesusers have liked this narrative

ZA

ZayaanS on Pro Medicus ·

Pro Medicus: The Market Is Confusing a Lumpy Quarter With a Broken Business

Fair Value:AU$196.7837.0% undervalued

34 followersusers have followed this narrative

7 commentsusers have commented on this narrative

21 likesusers have liked this narrative