Advertisement

- United States

- /

- Software

- /

- NasdaqGS:DDOG

Datadog (DDOG): Evaluating Current Valuation and Market Prospects in the Cloud Monitoring Sector

Datadog (DDOG) continues to draw attention from investors, especially as recent performance numbers signal interesting trends for the company. Its year-to-date gains and wider market moves provide context for anyone watching the cloud monitoring sector.

See our latest analysis for Datadog.

Datadog’s share price has gained strong momentum lately, with a recent 17.1% return over the last 90 days setting it apart from many tech peers. While there were some short-term dips this month, the stock’s robust three-year total shareholder return of 114.17% and year-to-date price return of 11.4% point to ongoing confidence in its growth story, even as near-term volatility reminds investors to stay watchful.

If you’re keeping an eye on cloud innovators like Datadog, you can spot more tech movers and fresh opportunities with our curated list: See the full list for free.

The key question for investors now is whether Datadog’s recent gains leave more room for upside, or if the stock’s forward momentum already reflects all the positive future expectations. Are we looking at a buying opportunity, or has the market already priced in its growth potential?

Most Popular Narrative: 24.5% Undervalued

Compared to Datadog’s last close at $160.01, the most popular narrative assigns a fair value of $211.97. This suggests strong potential for upside. This valuation reflects expectations that future earnings and platform expansion can outpace recent volatility and market skepticism.

Ongoing product innovation (for example, autonomous AI agents, enhanced security modules, expanded log and data observability) is increasing platform breadth and relevance. This is providing cross-selling opportunities and driving higher average revenue per user and net retention rate, which in turn improves recurring revenue predictability and gross margins.

Curious which assumptions are powering this bullish stance? The narrative’s core rests on a unique mix of rising margins and future profit multiples that defy typical software sector trends. Find out what surprising numbers could justify this aggressive fair value.

Result: Fair Value of $211.97 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, major customers cutting spending or fiercer competition from new platform entrants could quickly challenge Datadog’s optimistic growth outlook.

Find out about the key risks to this Datadog narrative.

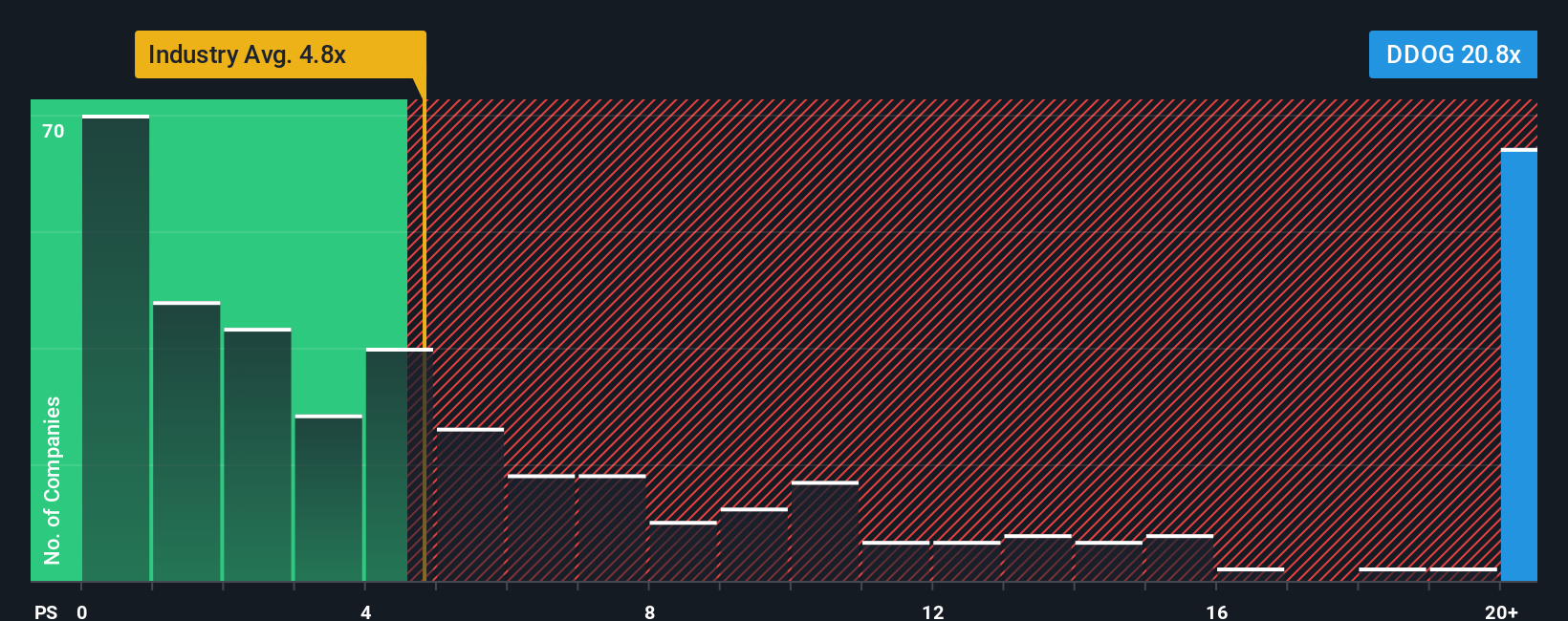

Another View: Valuation by Sales Ratio

Taking a look from a price-to-sales perspective, Datadog comes out as expensive. Its ratio stands at 17.5 times sales, much higher than the peer average of 7.2 times and the industry’s 4.9 times. That is well above the fair ratio of 15.5 times that the market might ultimately target. Does this premium signal lasting quality, or possible over-exuberance?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Datadog Narrative

If the current analysis doesn’t match your take or you want to test your own assumptions, you can dive into the data and shape your own view in just a few minutes. Do it your way.

A great starting point for your Datadog research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Stay ahead of the curve and give yourself the edge by seeking out fresh investment angles before the crowd. Don’t miss out on opportunities only found through creative stock hunting. Incredible growth stories and solid value plays await just beyond the obvious choices.

- Accelerate your hunt for tomorrow’s winners with these 914 undervalued stocks based on cash flows, which signals exceptional value potential hidden in plain sight.

- Tap into growth at the intersection of healthcare and technology by reviewing these 30 healthcare AI stocks, helping shape next-generation medical breakthroughs.

- Plug into the future of finance by considering these 81 cryptocurrency and blockchain stocks, shaping secure payment systems and decentralized innovation across industries.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:DDOG

Datadog

Operates an observability and security platform for cloud applications in the United States and internationally.

Excellent balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0775.1% undervalued

126 followersusers have followed this narrative

1 commentusers have commented on this narrative

21 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9822.7% undervalued

40 followersusers have followed this narrative

0 commentsusers have commented on this narrative

32 likesusers have liked this narrative

KO

Kouj on CSL ·

CSL: The Dip Is the Opportunity

Fair Value:AU$1559.0% undervalued

17 followersusers have followed this narrative

0 commentsusers have commented on this narrative

13 likesusers have liked this narrative

GA

GavrielH on DHT Holdings ·

DHT Holdings, inc: Strait of Hormuz Risk Amidst US-Israel vs Iran Tensions Spikes VLCC Rates.

Fair Value:US$3653.2% undervalued

14 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

VE

Vestra on MasTec ·

MasTec Inc. (MTZ): The Infrastructure Super-Cycle and the $19 Billion Backlog Milestone

Fair Value:US$33613.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SA

Sax on Super Retail Group ·

Fair Value Intriguingly Set at $11.54 for SUL Investors

Fair Value:AU$13.431.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on Dell Technologies ·

Dell Technologies (DELL): The AI Infrastructure Super-Cycle and the $50 Billion Server Milestone

Fair Value:US$193.521.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.378.4% undervalued

53 followersusers have followed this narrative

3 commentsusers have commented on this narrative

28 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9822.7% undervalued

40 followersusers have followed this narrative

0 commentsusers have commented on this narrative

32 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$59633.6% undervalued

1309 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative

Trending Discussion

DA

daqui_luis on Corticeira Amorim S.G.P.S ·

Great analysis on a great and solid company with a dominant position in the Cork Market.

1

|0