Advertisement

- United States

- /

- Software

- /

- NasdaqCM:BTDR

A Look At Bitdeer Technologies Group (BTDR) Valuation As It Shifts From Crypto Mining To AI Data Centers

Bitdeer Technologies Group (BTDR) is drawing fresh attention after Bitdeer AI launched NVIDIA GB200 NVL72 infrastructure in Malaysia and began converting several global crypto mining sites into GPU focused AI data centers.

See our latest analysis for Bitdeer Technologies Group.

The share price has been volatile around these AI announcements, with a 26.46% 1 month share price return and 25.80% year to date share price return, set against a 29.67% 1 year total shareholder return decline and 37.99% 3 year total shareholder return gain. Taken together, these figures suggest that recent momentum is rebuilding after earlier setbacks linked to project delays and ongoing class action headlines.

If Bitdeer’s AI pivot has your attention, this could be a good moment to size up other high growth tech and AI names through high growth tech and AI stocks.

With BTDR trading at US$14.53 and an intrinsic value estimate and analyst target both roughly double that level, the key question is simple: is the stock still mispriced, or is the AI pivot already fully reflected in expectations?

Most Popular Narrative: 54.5% Undervalued

With Bitdeer Technologies Group’s fair value narrative sitting around $31.92 against a last close of $14.53, the current price sits well below that framework and puts a spotlight on the growth and margin assumptions behind it.

The planned ramp-up to 40 exahash in self-mining capacity by Q4 2025, leveraging newly developed ASICs and expanded power capacity, is expected to significantly increase Bitcoin production, thereby driving revenue and potentially improving margins due to economies of scale.

Curious what kind of revenue surge and margin shift would need to line up with that power build out to support a fair value more than double the current share price? The most followed narrative leans on aggressive earnings rebuild, richer profitability and a future earnings multiple that still sits below many software peers. Want to see exactly how those moving parts stack together in the model and where expectations start to look stretched or conservative?

Result: Fair Value of $31.92 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, you still need to weigh softer hosting demand and the shareholder class action, either of which could challenge the upbeat earnings and margin reset that are part of this narrative.

Find out about the key risks to this Bitdeer Technologies Group narrative.

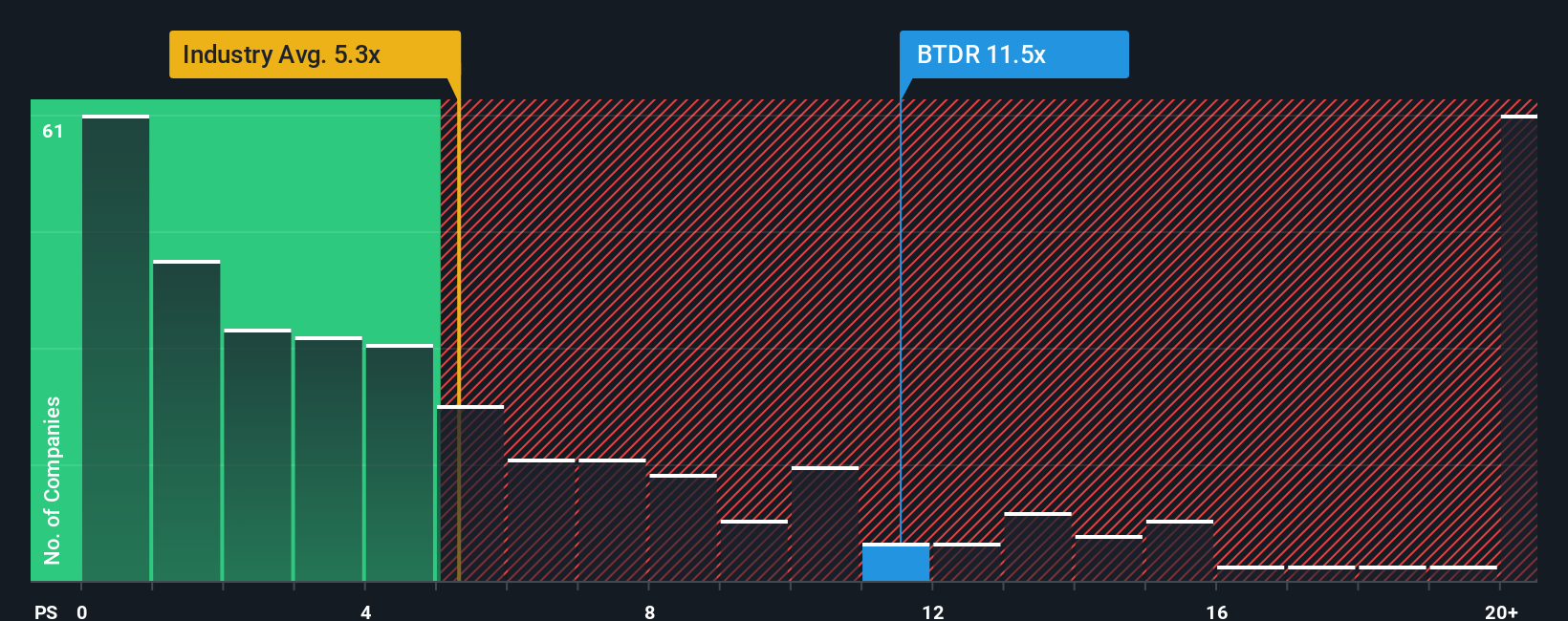

Another Angle on Valuation: Price to Sales Risks

The fair value narrative and SWS DCF model both point to Bitdeer looking cheap against its own cash flow potential, yet the market is already paying a rich price on sales. BTDR trades on a P/S of 7.2x, compared with 4.5x for the wider US Software group and about 4x for direct peers, while the SWS fair ratio sits higher at 10.6x. In plain terms, the current tag already prices in heavier expectations than many comparable names, even if the model suggests more room to run. This raises the question: how much valuation risk are you comfortable carrying if sentiment or forecasts shift?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Bitdeer Technologies Group Narrative

If you see the story differently or would rather lean on your own work, you can pull the same data, pressure test the assumptions and Do it your way in just a few minutes.

A great starting point for your Bitdeer Technologies Group research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Bitdeer might be front of mind right now, but you do not want to miss other opportunities that fit your style, sector focus, and risk comfort.

- Scan for potential bargains that the market may be overlooking by reviewing these 872 undervalued stocks based on cash flows with stronger cash flow support than their current prices suggest.

- Target growth stories at earlier stages by checking out these 3521 penny stocks with strong financials that pair smaller market caps with more resilient financial profiles.

- Position yourself closer to key trends in digital assets by assessing these 19 cryptocurrency and blockchain stocks that link equity exposure to blockchain and cryptocurrency themes.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Bitdeer Technologies Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqCM:BTDR

Bitdeer Technologies Group

Operates as a technology company for blockchain and high-performance computing (HPC) in Singapore, the United States, Bhutan, and Norway.

Moderate risk with limited growth.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0777.3% undervalued

175 followersusers have followed this narrative

1 commentusers have commented on this narrative

26 likesusers have liked this narrative

CL

Clive_Thompson on Hermès International Société en commandite par actions ·

Hermès - Expensive bags, and expensive stock. And the story of €14 billion of bearer shares gone missing.

Fair Value:€1.51k9.6% overvalued

24 followersusers have followed this narrative

1 commentusers have commented on this narrative

23 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$50013.5% undervalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

JO

Jolt_Communications on ZenaTech ·

ZenaTech: A big bet on the rise of AI drones and drones-as-a-service

Fair Value:US$6.8563.4% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Recently Updated Narratives

TR

tripledub on Dusk Group ·

Buying a Dollar for Fifty Cents: The Case for Dusk Group

Fair Value:AU$1.4546.6% undervalued

18 followersusers have followed this narrative

2 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AH

AHaron on Eli Lilly ·

Eli Lilly: A Pipeline-Driven Growth Story Trading 30% Below What the Business Is Actually Worth

Fair Value:US$1.48k38.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on Parker-Hannifin ·

Parker-Hannifin (PH): The "Motion Control" Compounder and the Aerospace Boom

Fair Value:US$1.04k11.1% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9827.3% undervalued

49 followersusers have followed this narrative

0 commentsusers have commented on this narrative

36 likesusers have liked this narrative

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.377.9% undervalued

56 followersusers have followed this narrative

3 commentsusers have commented on this narrative

30 likesusers have liked this narrative

PD

pdixit1 on Vertiv Holdings Co ·

The Infrastructure AI Cannot Be Built Without

Fair Value:US$408.6433.7% undervalued

39 followersusers have followed this narrative

3 commentsusers have commented on this narrative

18 likesusers have liked this narrative

Trending Discussion

OD

Oddlott on lululemon athletica ·

Thankyou for the interesting comments. So what is the world wide including USA growth rate?

0

|0