- United States

- /

- IT

- /

- NasdaqGS:BCOV

Brightcove Inc. (NASDAQ:BCOV) Released Earnings Last Week And Analysts Lifted Their Price Target To US$4.25

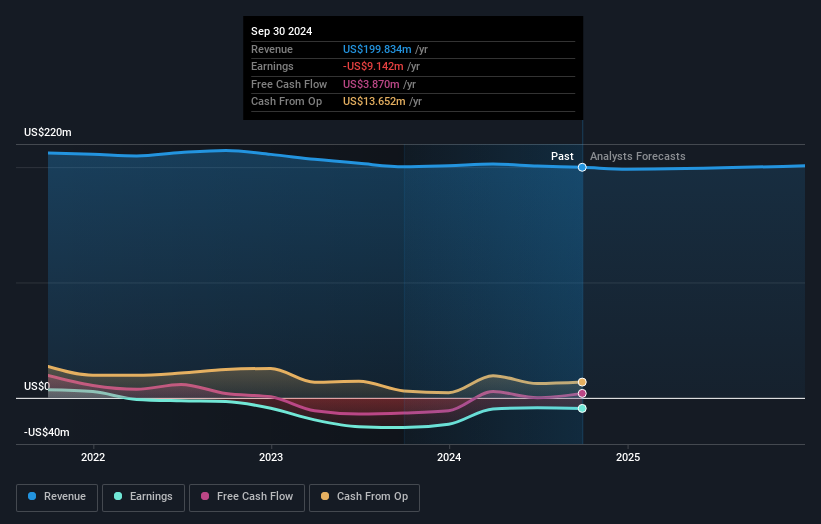

As you might know, Brightcove Inc. (NASDAQ:BCOV) just kicked off its latest third-quarter results with some very strong numbers. Results overall were solid, with revenues arriving 2.9% better than analyst forecasts at US$50m. Higher revenues also resulted in substantially lower statutory losses which, at US$0.07 per share, were 2.9% smaller than the analysts expected. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. We've gathered the most recent statutory forecasts to see whether the analysts have changed their earnings models, following these results.

View our latest analysis for Brightcove

Following last week's earnings report, Brightcove's dual analysts are forecasting 2025 revenues to be US$201.2m, approximately in line with the last 12 months. Per-share losses are expected to explode, reaching US$0.30 per share. Before this earnings announcement, the analysts had been modelling revenues of US$201.0m and losses of US$0.44 per share in 2025. While the revenue estimates were largely unchanged, sentiment seems to have improved, with the analysts upgrading their numbers and making a considerable decrease in losses per share in particular.

The average price target rose 9.7% to US$4.25, with the analysts signalling that the forecast reduction in losses would be a positive for the stock's valuation.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Brightcove's past performance and to peers in the same industry. It's pretty clear that there is an expectation that Brightcove's revenue growth will slow down substantially, with revenues to the end of 2025 expected to display 0.5% growth on an annualised basis. This is compared to a historical growth rate of 1.7% over the past five years. Compare this against other companies (with analyst forecasts) in the industry, which are in aggregate expected to see revenue growth of 9.1% annually. So it's pretty clear that, while revenue growth is expected to slow down, the wider industry is also expected to grow faster than Brightcove.

The Bottom Line

The most important thing to take away is that the analysts reconfirmed their loss per share estimates for next year. On the plus side, there were no major changes to revenue estimates; although forecasts imply they will perform worse than the wider industry. We note an upgrade to the price target, suggesting that the analysts believes the intrinsic value of the business is likely to improve over time.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. At least one analyst has provided forecasts out to 2025, which can be seen for free on our platform here.

Plus, you should also learn about the 2 warning signs we've spotted with Brightcove (including 1 which is concerning) .

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Brightcove might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:BCOV

Brightcove

Provides cloud-based streaming services the Americas, Europe, the Asia Pacific, Japan, India, and the Middle East.

Excellent balance sheet and fair value.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion