Advertisement

- United States

- /

- Software

- /

- NasdaqGS:APP

Will AppLovin's (APP) Array Exit Refocus the Spotlight on Its Core AI Ad Platform?

Reviewed by Sasha Jovanovic

- Earlier this month, AppLovin shut down its Array app distribution tool following allegations and regulatory concerns that the software enabled some apps to be downloaded on user devices without consent, prompting investigations and scrutiny from authorities including the SEC.

- Despite the controversy, analysts and investors have focused on AppLovin’s core advertising technology and AI-driven Axon platform, viewing the removal of Array as alleviating risk and highlighting the company's future growth potential in digital advertising and e-commerce.

- We'll explore how the discontinuation of Array amid regulatory scrutiny impacts AppLovin's investment narrative and outlook for its core platform.

AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

AppLovin Investment Narrative Recap

To own AppLovin, investors need confidence in its AI-powered Axon platform driving long-term growth in digital advertising and e-commerce, while also recognizing the risks of regulatory scrutiny over data practices. The decision to discontinue Array following consent concerns and ongoing SEC investigations heightens regulatory focus but does not appear to materially impact the biggest near-term catalyst: international and vertical expansion of the Axon Ads Manager. The company's core product rollout remains the central story, although regulatory uncertainty hangs over the outlook.

Most relevant to these events is AppLovin's recent launch of the Axon Ads Manager, a self-service tool initially available via referral. This freshly announced platform, powered by AI for data-driven ad targeting, aims to open new revenue streams and expand beyond gaming into e-commerce, aligning closely with the core growth catalyst many investors are watching.

However, beneath strong product momentum, investors should be aware that intensifying regulatory oversight following Array’s shutdown could...

Read the full narrative on AppLovin (it's free!)

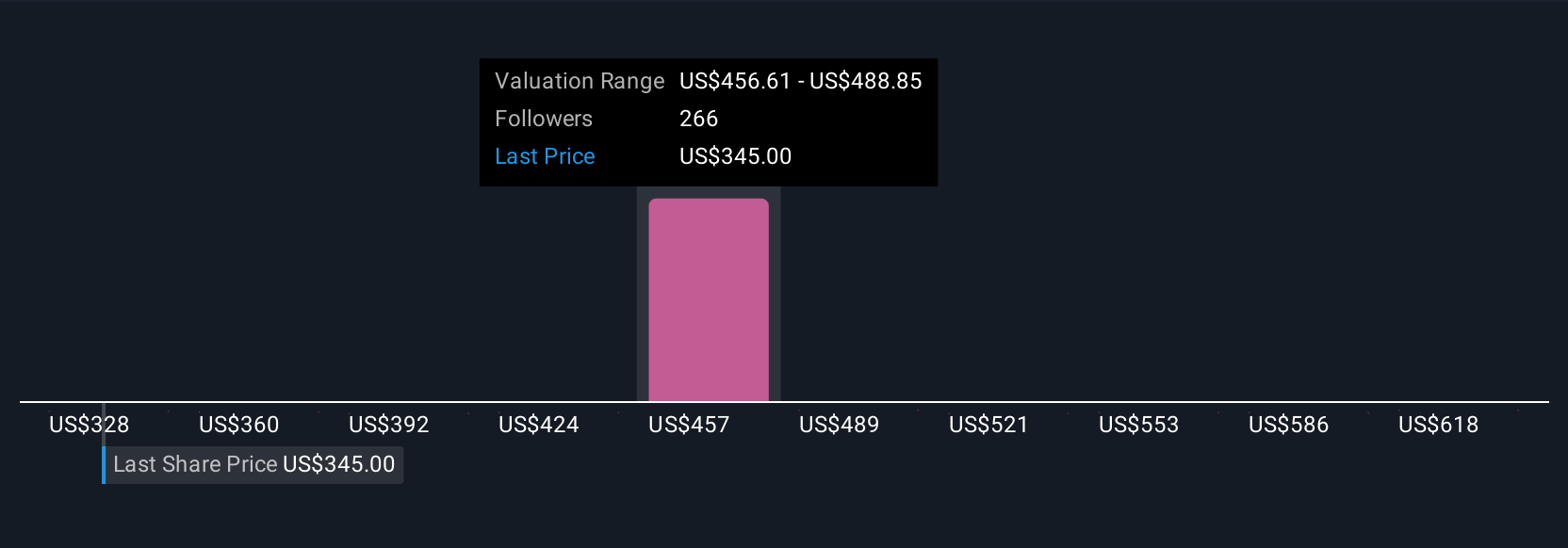

AppLovin's narrative projects $10.5 billion revenue and $6.2 billion earnings by 2028. This requires 22.2% yearly revenue growth and a $3.7 billion earnings increase from $2.5 billion today.

Uncover how AppLovin's forecasts yield a $613.59 fair value, in line with its current price.

Exploring Other Perspectives

Simply Wall St Community members submitted 25 fair value estimates for AppLovin, ranging from US$318 to US$663 per share. As regulatory scrutiny increases, your outlook on AppLovin’s data practices and platform expansion could shape your expectations for future performance, consider the full spectrum of community insights before deciding.

Explore 25 other fair value estimates on AppLovin - why the stock might be worth 47% less than the current price!

Build Your Own AppLovin Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- Our free AppLovin research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate AppLovin's overall financial health at a glance.

No Opportunity In AppLovin?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- We've found 20 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:APP

AppLovin

Provides end-to-end artificial intelligence-powered advertising solutions for businesses in the United States and internationally.

Exceptional growth potential with flawless balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Eva Live ·

This small cap is building the AI workforce of the future

Fair Value:US$7.4352.0% undervalued

74 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22042.4% undervalued

24 followersusers have followed this narrative

6 commentsusers have commented on this narrative

26 likesusers have liked this narrative

WO

woodworthfund on Kraft Heinz ·

Kraft Heinz (KHC): Less Drama, More Ketchup

Fair Value:US$3532.7% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

CA

Canderous on PetroTal ·

Beyond 2026, Beyond a Double

Fair Value:CA$1.8168.5% undervalued

26 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

Recently Updated Narratives

DE

DeathSmiIes on New Horizon Aircraft ·

HORIZON AIRCRAFT (HOVR) Institutional Investor Package August 1, 2025 — Confidential Review Draft

Fair Value:US$2087.6% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

Coward_Nutlick on Elicio Therapeutics ·

Very Bullish

Fair Value:US$10090.1% undervalued

20 followersusers have followed this narrative

3 commentsusers have commented on this narrative

2 likesusers have liked this narrative

KA

kapirey on KKR ·

Incluso con un colapso brutal del crédito KKR mantendría beneficios relevantes

Fair Value:US$84.4512.2% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8590.1% undervalued

114 followersusers have followed this narrative

2 commentsusers have commented on this narrative

31 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$268.6118.3% undervalued

1193 followersusers have followed this narrative

7 commentsusers have commented on this narrative

34 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22042.4% undervalued

24 followersusers have followed this narrative

6 commentsusers have commented on this narrative

26 likesusers have liked this narrative