Advertisement

- United States

- /

- Software

- /

- NasdaqGS:ADBE

Is Adobe (ADBE) Pricing Look Interesting After Recent Share Price Slide?

Reviewed by Bailey Pemberton

- If you are wondering whether Adobe's current share price makes sense, this article walks through how its value stacks up using several common methods.

- At a recent closing price of US$293.25, Adobe's share price reflects a 2.6% decline over the last 7 days and sits 12.0% lower over both the last 30 days and year to date, with a 33.0% decline over 1 year and a 22.7% decline over 3 years.

- Over the past few years, Adobe has regularly been in the headlines for its role in creative software and digital experiences. This has kept investor attention on how markets are pricing its long term prospects. Broader sector sentiment and shifts in how investors view growth and risk in software have formed an important backdrop to these moves in Adobe's share price.

- Our valuation framework scores Adobe at 5 out of 6 on our valuation checks. This means it screens as undervalued on most of the measures we test. Next we will walk through those approaches before finishing with a simpler way to keep on top of its value over time.

Find out why Adobe's -33.0% return over the last year is lagging behind its peers.

Approach 1: Adobe Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model looks at the cash Adobe is expected to generate in the future, then discounts those projected cash flows back into today’s dollars to estimate what the business might be worth right now.

For Adobe, the model used here is a 2 stage Free Cash Flow to Equity approach based on cash flow projections. The latest twelve month Free Cash Flow is about US$9.8b. Analyst inputs and extrapolated estimates point to projected Free Cash Flow of roughly US$13.0b in 2030, with annual projections between 2026 and 2035 discounted back to today.

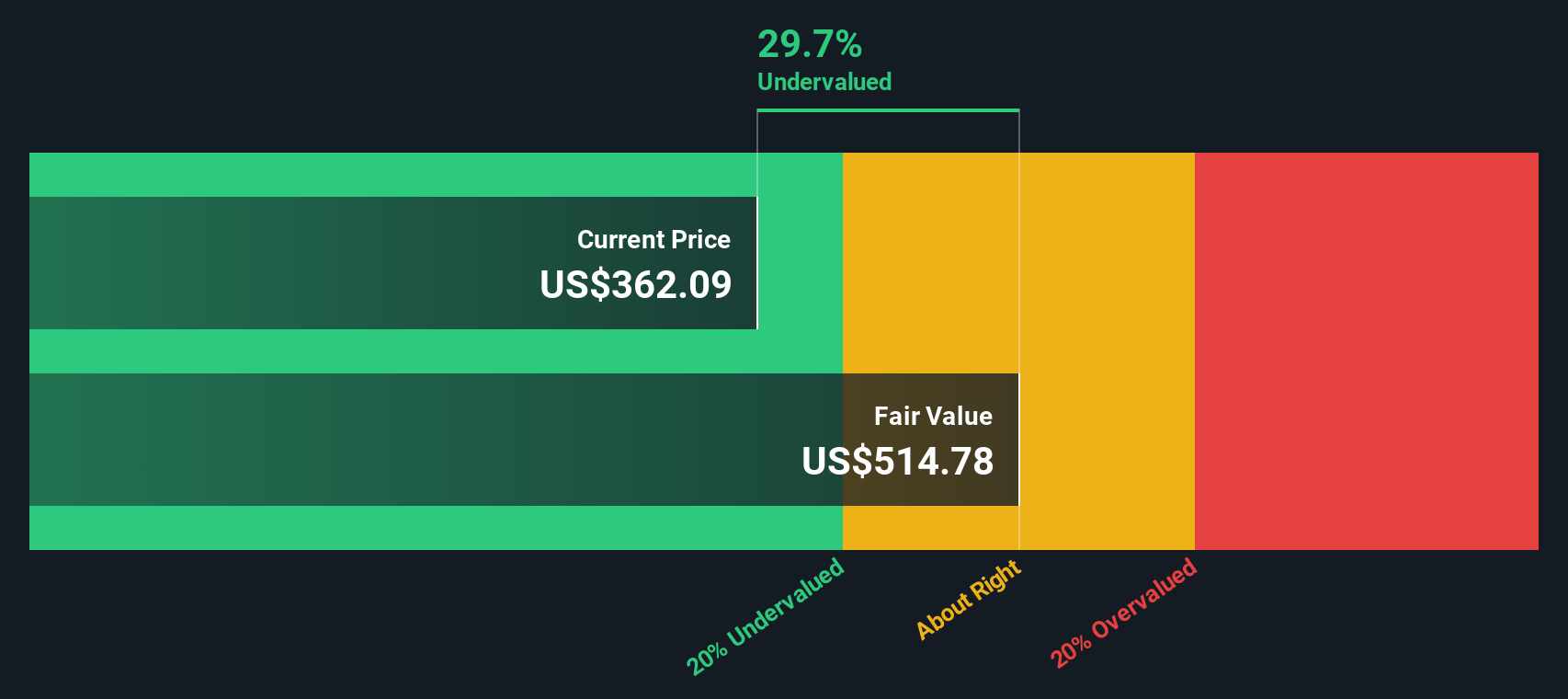

When all those discounted cash flows are added together, the model arrives at an estimated intrinsic value of US$534.75 per share. Compared with the recent share price of US$293.25, the DCF output suggests Adobe trades at a 45.2% discount to this intrinsic estimate, which screens as meaningfully undervalued on this methodology.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Adobe is undervalued by 45.2%. Track this in your watchlist or portfolio, or discover 875 more undervalued stocks based on cash flows.

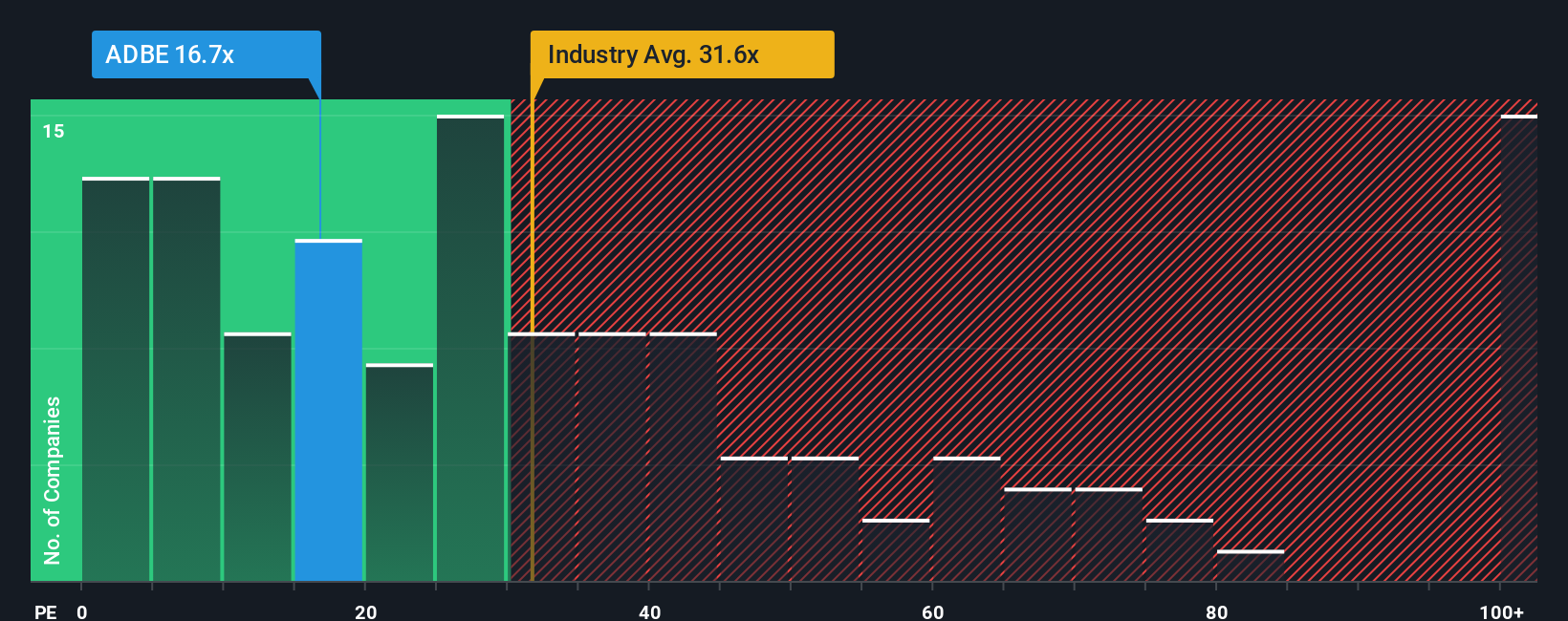

Approach 2: Adobe Price vs Earnings (P/E)

For profitable companies like Adobe, the P/E ratio is a useful way to relate what you pay for each share to the earnings the business is currently generating. It gives you a quick sense of how many dollars investors are willing to pay today for one dollar of annual earnings.

What counts as a “normal” P/E depends a lot on how investors view a company’s growth prospects and risk. Higher expected growth or lower perceived risk can support a higher P/E, while slower growth or higher uncertainty usually points to a lower, more cautious multiple.

Adobe currently trades on a P/E of 16.88x. That sits below both the Software industry average of 28.24x and the peer group average of 50.97x. Simply Wall St’s Fair Ratio for Adobe is 31.03x. This Fair Ratio is a proprietary estimate of the P/E you might expect given factors such as earnings growth characteristics, industry, profit margins, market cap and company specific risks.

Because the Fair Ratio builds those fundamentals in directly, it can be more informative than a simple comparison with peers or the broad industry. With Adobe’s current P/E of 16.88x sitting well below the Fair Ratio of 31.03x, this framework indicates that the shares currently screen as undervalued on a P/E basis.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1426 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Adobe Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple way for you to attach your own story about Adobe to the numbers you see on screen, including your assumed fair value and your expectations for its future revenue, earnings and margins.

A Narrative links three pieces together: what you believe about Adobe as a business, how that belief translates into a financial forecast, and what fair value that forecast implies for the shares.

On Simply Wall St, within the Community page that millions of investors use, Narratives give you an easy tool to compare that fair value to the current price so you can decide whether the gap between them looks attractive enough to act on.

Because Narratives update when new information such as news or earnings is added to the platform, your view on Adobe can stay current without you rebuilding a model each time, and you can see how other investors arrive at very different fair values for the same stock based on their own assumptions about Adobe’s future.

Do you think there's more to the story for Adobe? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:ADBE

Adobe

Operates as a technology company worldwide.

Undervalued with proven track record.

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Cue Biopharma ·

Cue Biopharma (NASDAQ: CUE): The Scientist Behind Xolair Just Gave Cue a Next-Generation Shot at the Same Multi-Billion-Dollar Market

Fair Value:US$7058.5% undervalued

21 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

HE

HedgeY on AST SpaceMobile ·

AST SpaceMobile: The Boldest Direct-to-Cell Bet in Public Markets

Fair Value:US$17045.8% undervalued

43 followersusers have followed this narrative

0 commentsusers have commented on this narrative

13 likesusers have liked this narrative

FU

FundamentalFlow on Onto Innovation ·

Onto Innovation: The Advanced Packaging Chokepoint 51.3% undervalued intrinsic discount

Fair Value:US$38029.2% undervalued

26 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7449.0% undervalued

58 followersusers have followed this narrative

0 commentsusers have commented on this narrative

15 likesusers have liked this narrative

Recently Updated Narratives

AN

AntonioS on IDP Education ·

IDP Education Limited (ASX: IEL) - A contrarian Review

Fair Value:AU$4.6256.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

REElax on Volta Metals ·

Springer REE deposit valuation

Fair Value:CA$3.595.0% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

davidlsander on Atlas Salt ·

Once In A Life Time Deeply Discounted Recession Proof Utility

Fair Value:CA$2.9656.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7449.0% undervalued

58 followersusers have followed this narrative

0 commentsusers have commented on this narrative

15 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9723.3% undervalued

57 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1933.9% undervalued

48 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

Trending Discussion

KA

Karndog on Berkshire Hathaway ·

Abel is also an Energy expert. He's already on the AI train even without "buying tech".

0

|0

SI

Simply Wall St User on Automatic Data Processing ·

This stock with dividend Aristocrat status and real annual increases may require more time to ascert...

0

|0

SI

Simply Wall St User on Access Holdings ·

It's wonderful. It has greatly helped me take informed decisions.

0

|0