- United States

- /

- Software

- /

- NasdaqGS:ADBE

Adobe (NasdaqGS:ADBE) Expands Firefly AI and Partners with Infosys for Enhanced Marketing Solutions

Reviewed by Simply Wall St

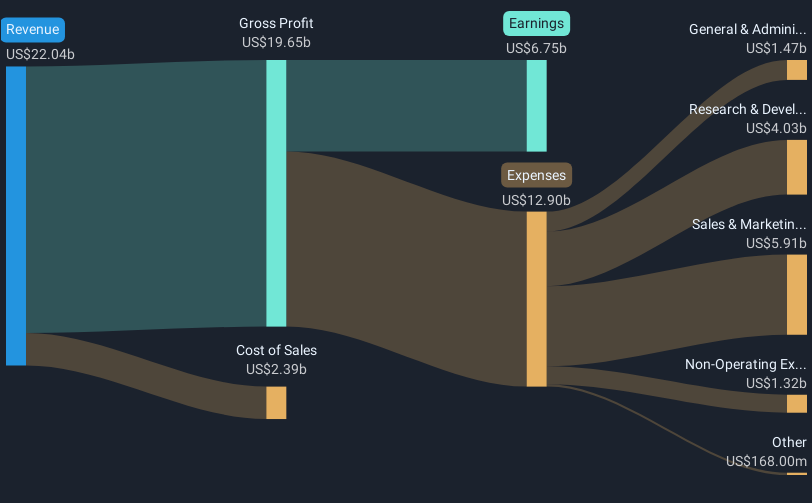

Adobe (NasdaqGS:ADBE) recently announced a strategic collaboration with Infosys to harness AI for marketing transformation, and expanded its Firefly platform to mobile, offering advanced AI-assisted features. These initiatives, alongside robust earnings showing revenue and net income growth, appear aligned with Adobe’s content creation and marketing focus. Market volatility due to geopolitical tensions and interest rate decisions has seen tech stocks generally rise, but Adobe's stock remained flat over the last quarter, reflecting broader market trends. The company's share repurchases and key partnerships, while positive, seemed to counterbalance market uncertainties without greatly influencing its overall stock performance.

Buy, Hold or Sell Adobe? View our complete analysis and fair value estimate and you decide.

The recent strategic collaboration between Adobe and Infosys to leverage AI for marketing, along with the expansion of Adobe's Firefly platform to mobile, could bolster Adobe's growth narrative. These advancements could generate new user engagement and improve product stickiness, potentially enhancing revenue and margin through increased upsell opportunities. The integration of AI-assisted features may drive future earnings growth as more enterprises prioritize content personalization.

Over the past three years, Adobe's total shareholder return, including dividends, was 5.42%. This longer-term performance offers a broader context compared to the recent flat stock movement, highlighting Adobe's resilience in a volatile market primarily driven by geopolitical tensions and interest rate decisions. Within the past year, Adobe underperformed the broader US market and the US software industry, delivering lower returns relative to both. Analysts estimate Adobe's fair value at US$493.43, indicating a potential upside, with its current share price at US$382.98. That said, this level remains 0.8% above the bearish price target of US$380.0.

Understand Adobe's earnings outlook by examining our growth report.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:ADBE

Outstanding track record and undervalued.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion