Advertisement

Unfortunately for shareholders, when eMagin Corporation (NYSEMKT:EMAN) reported results for the period to December 2020, its auditors, McGladrey LLP - RSM LLP, expressed uncertainty about whether it can continue as a going concern. Thus we can say that, based on the results to that date, the company should raise capital or otherwise raise cash, without much delay.

Given its situation, it may not be in a good position to raise capital on favorable terms. So shareholders should absolutely be taking a close look at how risky the balance sheet is. The biggest concern we would have is the company's debt, since its lenders might force the company into administration if it cannot repay them.

View our latest analysis for eMagin

How Much Debt Does eMagin Carry?

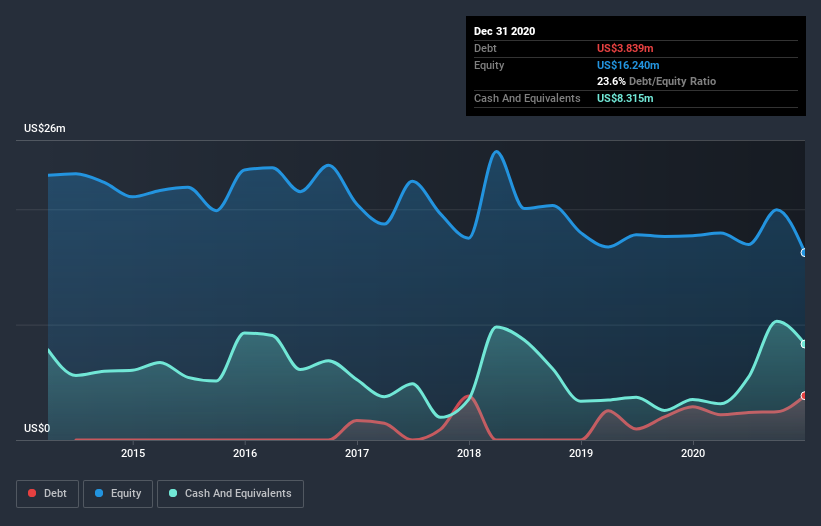

You can click the graphic below for the historical numbers, but it shows that as of December 2020 eMagin had US$3.84m of debt, an increase on US$2.89m, over one year. However, it does have US$8.32m in cash offsetting this, leading to net cash of US$4.48m.

How Strong Is eMagin's Balance Sheet?

According to the last reported balance sheet, eMagin had liabilities of US$14.3m due within 12 months, and liabilities of US$17.1m due beyond 12 months. Offsetting these obligations, it had cash of US$8.32m as well as receivables valued at US$6.58m due within 12 months. So its liabilities total US$16.5m more than the combination of its cash and short-term receivables.

Since publicly traded eMagin shares are worth a total of US$300.1m, it seems unlikely that this level of liabilities would be a major threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time. Despite its noteworthy liabilities, eMagin boasts net cash, so it's fair to say it does not have a heavy debt load! When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if eMagin can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Over 12 months, eMagin reported revenue of US$29m, which is a gain of 10%, although it did not report any earnings before interest and tax. We usually like to see faster growth from unprofitable companies, but each to their own.

So How Risky Is eMagin?

Statistically speaking companies that lose money are riskier than those that make money. And we do note that eMagin had an earnings before interest and tax (EBIT) loss, over the last year. And over the same period it saw negative free cash outflow of US$6.0m and booked a US$11m accounting loss. Given it only has net cash of US$4.48m, the company may need to raise more capital if it doesn't reach break-even soon. Overall, we'd say the stock is a bit risky, and we're usually very cautious until we see positive free cash flow. We're too cautious to want to invest in a company after an auditor has expressed doubts about its ability to continue as a going concern. That's because companies should always make sure the auditor has confidence that the company will continue as a going concern, in our view. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. For instance, we've identified 4 warning signs for eMagin (1 can't be ignored) you should be aware of.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

If you’re looking to trade eMagin, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NYSEAM:EMAN

eMagin

eMagin Corporation engages in the design, develop, manufacture, and market of organic light emitting diode (OLED) miniature displays on-silicon micro displays, virtual imaging products that utilize OLED micro displays, and related products in the United States and internationally.

Imperfect balance sheet and overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor