- United States

- /

- Semiconductors

- /

- NYSE:TSM

TSMC (NYSE:TSM) Valuation Check After Strong Multi‑Year Rally and Recent Pullback

Reviewed by Simply Wall St

Market context and recent performance

Taiwan Semiconductor Manufacturing (TSM) has quietly kept its uptrend intact, with shares up about 45% over the past year and roughly 3x over the past 3 years, even after recent weekly volatility.

See our latest analysis for Taiwan Semiconductor Manufacturing.

That recent 7 day share price pullback sits against a much stronger backdrop, with a roughly 41% year to date share price return and a powerful multiyear total shareholder return. This suggests momentum is still broadly intact as investors reassess long term growth and supply chain risk.

If TSM has you thinking about the broader chip story, it is also worth seeing how other names stack up by exploring high growth tech and AI stocks.

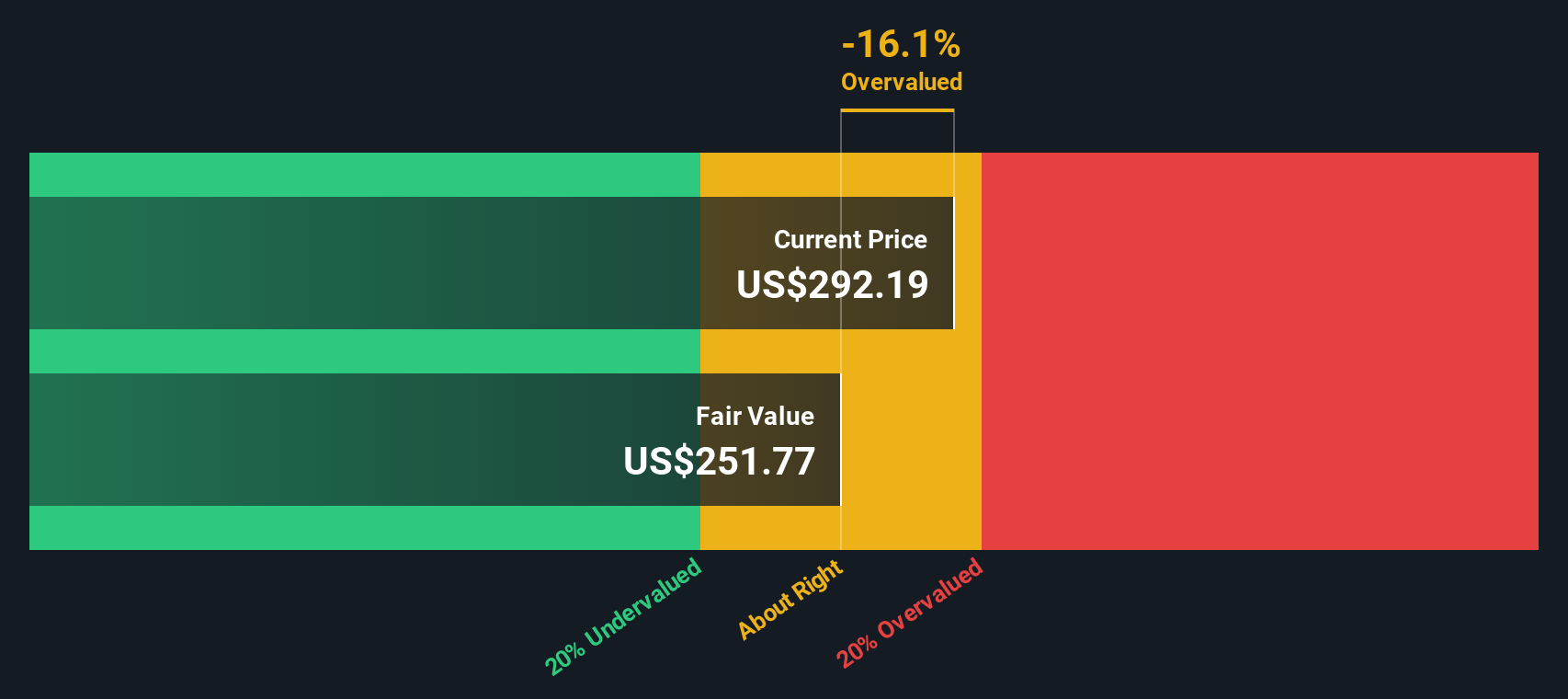

With earnings still growing double digits and the share price sitting about 24% below consensus targets, investors face a key question: is TSM still mispriced, or has the market already baked in the next leg of growth?

Most Popular Narrative Narrative: 8.2% Undervalued

According to oscargarcia, the fair value sits above the latest 284.68 close, implying further upside if TSMC executes on its growth blueprint.

TSMC is the central pillar of the global semiconductor ecosystem, powering the AI revolution with unmatched scale, cutting edge process technology, and disciplined execution. With record profits, dominant client base, and massive expansion underway, both in Taiwan and abroad, it stands as a low risk way to own the AI infrastructure wave.

Curious how sustained double digit growth, thick margins, and a confident profit multiple combine into that valuation call? The key assumptions may surprise you.

Result: Fair Value of $310 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, sustained US China tensions and rising costs from overseas fabs could squeeze margins and quickly change how investors value TSMC’s growth story.

Find out about the key risks to this Taiwan Semiconductor Manufacturing narrative.

Another View: Our DCF Model Flips the Story

While the popular narrative points to upside, our DCF model suggests caution. On our numbers, TSM at $284.68 screens as overvalued versus an estimated fair value of $216.63, raising the question of whether sentiment has run ahead of fundamentals.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Taiwan Semiconductor Manufacturing for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 917 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Taiwan Semiconductor Manufacturing Narrative

If you see the story differently or prefer to dive into the numbers yourself, you can build a fresh narrative in just a few minutes: Do it your way.

A great starting point for your Taiwan Semiconductor Manufacturing research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Before you move on, lock in your next potential opportunity by using our powerful screener tools to uncover stocks that align with your strategy and risk profile.

- Target generous income streams by scanning these 13 dividend stocks with yields > 3% that can help strengthen your portfolio’s cash flow.

- Position yourself early in transformative trends with these 24 AI penny stocks pushing the boundaries of automation and intelligent software.

- Strengthen your margin of safety by reviewing these 917 undervalued stocks based on cash flows where market prices may not yet reflect underlying cash generation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Taiwan Semiconductor Manufacturing might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:TSM

Taiwan Semiconductor Manufacturing

Manufactures, packages, tests, and sells integrated circuits and other semiconductor devices in Taiwan, China, Europe, the Middle East, Africa, Japan, the United States, and internationally.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion