Taiwan Semiconductor Manufacturing (NYSE:TSM) shares have nudged higher recently, gaining nearly 2% over the past week. Investors are watching as the stock continues to show resilience despite modest dips over the past month.

TSMC’s recent gains reflect continued strong momentum that has been building over the past year, with its 1-year total shareholder return soaring past 60% and the latest 90-day share price return showing over 21% growth. While the past month saw a modest pullback, the long-term trend signals investors remain confident about the company’s growth potential and its pivotal role in the global semiconductor industry.

If you’re curious which other leading tech and semiconductor companies have been gaining traction lately, see the full list for free with our curated See the full list for free..

With shares hovering near record highs and a strong track record of growth, investors are left wondering if Taiwan Semiconductor Manufacturing is trading at a rare discount or if future gains are already priced in by the market.

Advertisement

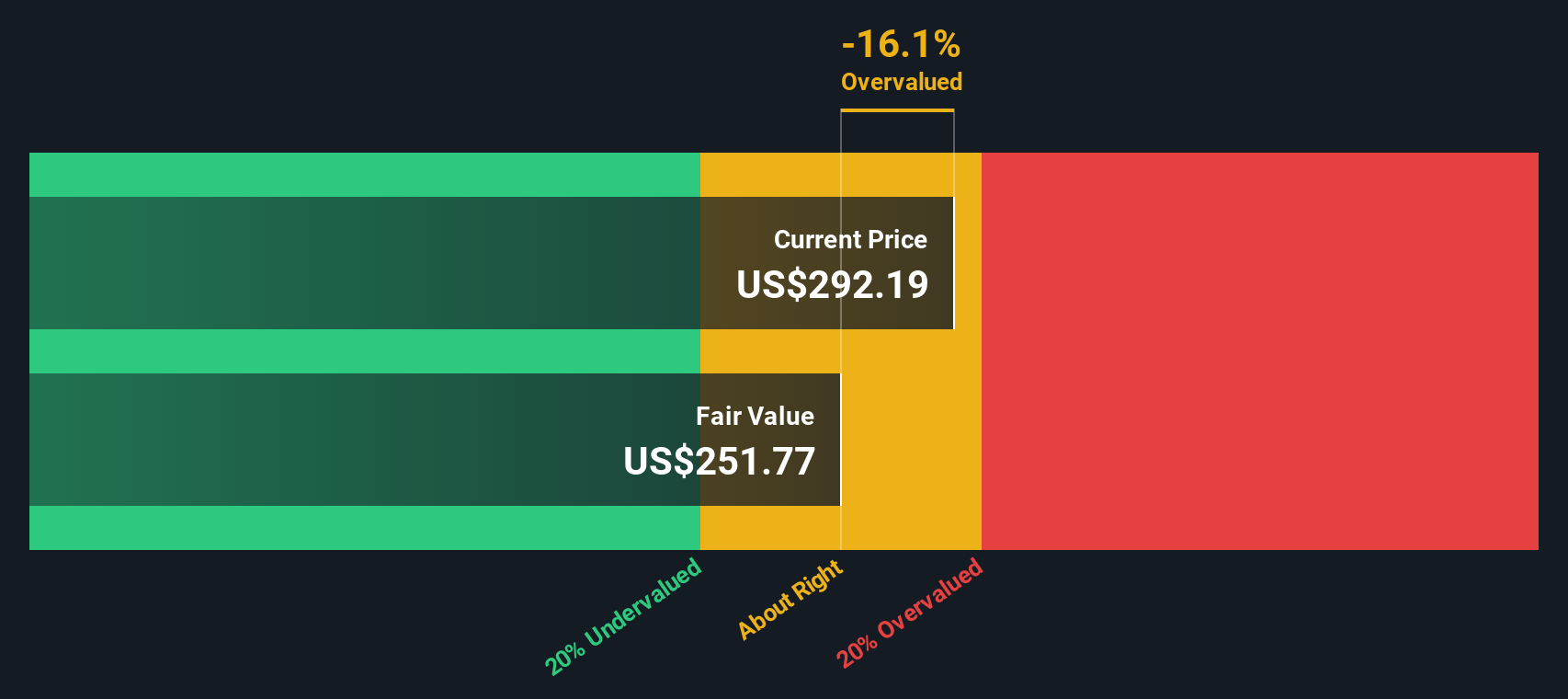

Most Popular Narrative: 6.5% Undervalued

According to oscargarcia’s widely followed narrative, Taiwan Semiconductor Manufacturing’s fair value is set notably higher than its recent $289.96 close. This suggests there is still some headroom left before reaching what the narrative considers full value. The story focuses on the company’s scale, AI-driven growth trajectory, and disciplined capital deployment as driving factors for this estimate.

TSMC is the central pillar of the global semiconductor ecosystem, powering the AI revolution with unmatched scale, cutting-edge process technology, and disciplined execution. With record profits, dominant client base, and massive expansion underway, both in Taiwan and abroad, it stands as a low-risk way to own the AI infrastructure wave. Although geopolitical and trade risks loom, its moat, margins, and market position offer a rare combination of growth, profitability, and stability.

Want to know why this valuation is turning heads? It is all about jaw-dropping earnings momentum, industry-leading margins, and enormous expansion bets that could reshape TSMC’s profit profile. See what bold numbers this narrative is built on and why investors are buzzing.

However, geopolitical friction and higher operating costs from global expansion could still challenge TSMC’s growth story. These factors may present potential risks for investors.

Another View: SWS DCF Model Offers a Cautious Take

Our SWS DCF model provides a different perspective and estimates Taiwan Semiconductor Manufacturing's fair value at $220.08. This suggests the current price may be outpacing long-term cash flow fundamentals, raising the question of whether the recent optimism could expose investors to a downside surprise.

Build Your Own Taiwan Semiconductor Manufacturing Narrative

If these viewpoints do not quite match your take, you can dive into the data and quickly craft your own unique narrative in just a few minutes. Do it your way.

A great starting point for your Taiwan Semiconductor Manufacturing research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Don’t miss out on the next big opportunity. Use the Simply Wall Street Screener and put top-rated stocks and creative strategies at your fingertips.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Taiwan Semiconductor Manufacturing might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Manufactures, packages, tests, and sells integrated circuits and other semiconductor devices in Taiwan, China, Europe, the Middle East, Africa, Japan, the United States, and internationally.