Advertisement

- United States

- /

- Semiconductors

- /

- NasdaqCM:RGTI

Assessing Rigetti Computing (RGTI) Valuation After Recent Share Price Volatility

Simply Wall St

Reviewed by Simply Wall St

Rigetti Computing: Stock Snapshot After Recent Moves

Rigetti Computing (RGTI) has drawn attention after recent trading moves, prompting investors to reassess how its quantum computing as a service model and current financial profile line up with their risk tolerance and time horizon.

See our latest analysis for Rigetti Computing.

Recent trading has been choppy, with a 1-day share price return of a 2.10% decline and a 90-day share price return of a 55.95% decline. However, the 1-year total shareholder return is very large, which indicates that longer term momentum is still meaningful despite near term volatility.

If Rigetti’s price swings have caught your attention, it can be useful to compare it with other quantum adjacent names and the broader high growth tech and AI stocks that are also focused on turning advanced computing into durable business models.

With Rigetti posting a very large 1 year return, ongoing annual revenue growth of 54% and an analyst price target sitting above the last close, you have to ask: is there still a buying opportunity here, or is future growth already priced in?

Price-to-Book of 21.9x: Is it justified?

Rigetti’s shares last closed at US$24.72, and at that price the stock trades on a P/B of 21.9x compared with much lower benchmarks in its space.

P/B compares a company’s market value to its net assets. This is a common reference point for hardware heavy areas like semiconductors where tangible assets matter. A higher P/B usually suggests the market is assigning extra value to future potential relative to the current balance sheet.

For Rigetti, that premium P/B sits against a backdrop of ongoing losses, a negative return on equity and forecasts that do not point to profitability over the next three years. That combination means the market price is placing a high value on future revenue growth and the quantum computing opportunity, even though current earnings do not support the valuation.

The contrast with peers is sharp. Rigetti’s 21.9x P/B is well above the US Semiconductor industry average of 4.3x and also ahead of the peer group average of 7.1x. This indicates investors are paying a much higher multiple of book value than is typical for the sector.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-book of 21.9x (OVERVALUED)

However, that story can change quickly if revenue growth slows or losses stay heavy, given net income of US$350.964 million against just US$7.494 million in revenue.

Find out about the key risks to this Rigetti Computing narrative.

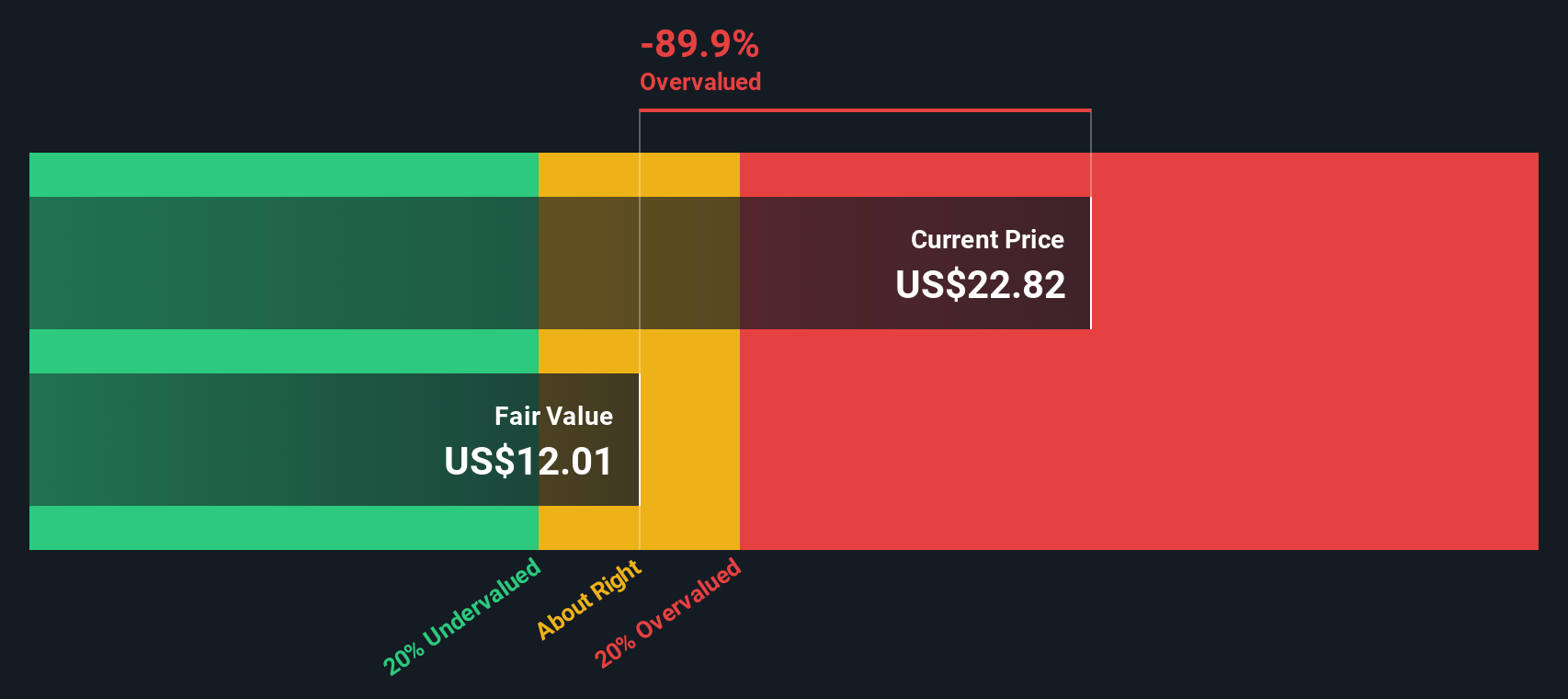

Another View: Discounted Cash Flow Signals a Different Story

While the 21.9x P/B ratio makes Rigetti look expensive next to semiconductor peers, our DCF model points the other way. At a last close of US$24.72, the shares are trading about 45% below an estimated fair value of US$45.31, which frames today’s price as a possible mismatch. Which signal do you think matters more for you, the balance sheet multiple or the long term cash flow view?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Rigetti Computing for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 882 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Rigetti Computing Narrative

If you see the data differently or prefer to base decisions on your own work, you can pull the numbers together and build a full story in just a few minutes, Do it your way.

A great starting point for your Rigetti Computing research is our analysis highlighting 2 key rewards and 4 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Rigetti has sparked your curiosity, do not stop here. Use the Simply Wall St Screener to spot other opportunities that fit your style before the market moves on.

- Target potential value opportunities by scanning these 882 undervalued stocks based on cash flows to find cases where price aligns with underlying cash flows and fundamentals.

- Spot emerging opportunities at the frontier of computation by checking out these 29 quantum computing stocks to see companies that are pushing quantum technologies into real world use cases.

- Boost your income focus by reviewing these 12 dividend stocks with yields > 3% which currently offer yields above 3% alongside detailed fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqCM:RGTI

Rigetti Computing

Through its subsidiaries, builds quantum computers and the superconducting quantum processors the United States, the United Kingdom, rest of Europe, Asia, and internationally.

Excellent balance sheet with slight risk.

Similar Companies

Market Insights

Advertisement

Weekly Picks

JO

Jolt_Communications on Myseum ·

The Future of Social Sharing Is Private and People Are Ready

Fair Value:US$7.9577.1% undervalued

25 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TO

Tokyo on ASML Holding ·

EU#3 - From Philips Management Buyout to Europe’s Biggest Company

Fair Value:€1.31k7.1% undervalued

29 followersusers have followed this narrative

4 commentsusers have commented on this narrative

11 likesusers have liked this narrative

YI

yiannisz on Booking Holdings ·

Booking Holdings: Why Ground-Level Travel Trends Still Favor the Platform Giants

Fair Value:US$5.47k8.5% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

CO

composite32 on Shell ·

A fully integrated LNG business seems to be ignored by the market.

Fair Value:UK£36.122.6% undervalued

38 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

EM

emndy on Presco ·

High Quality Business and a true compounding machine

Fair Value:₦2.2k25.7% undervalued

10 followersusers have followed this narrative

2 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CL

Clive_Thompson on Roche Holding ·

Roche Holding AG To Benefit From Strong Drug Pipeline In 2027 And Beyond

Fair Value:CHF 430.0118.4% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on Otokar Otomotiv ve Savunma Sanayi ·

Otokar is the first choice for tactical armored land vehicles to meet Europe's defense industry needs.

Fair Value:₺668.1135.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OO

OOO97 on Neo Performance Materials ·

Undervalued Key Player in Magnets/Rare Earth

Fair Value:CA$25.3324.4% undervalued

72 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$253.0224.5% undervalued

1048 followersusers have followed this narrative

6 commentsusers have commented on this narrative

31 likesusers have liked this narrative

AN

AnalystConsensusTarget on Amazon.com ·

AMZN: Acceleration In Cloud And AI Will Drive Margin Expansion Ahead

Fair Value:US$295.6119.1% undervalued

1344 followersusers have followed this narrative

5 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Trending Discussion

KT

Ktre on Freeport-McMoRan ·

Barrick will also need Newmont to fund the capital for Fourmile, according to a person aware of the development which the miner has been touting as its future flagship asset and will also become part of the IPO. During a call with analysts in October 2025, Newmont's incoming CEO Natasha Viljoen said the company was waiting for some information from Barrick before committing additional capital. Barrick’s effort to restructure, potentially by splitting into two entities, is one of the most anticipated mining stories of 2026, given strong investor interest in gold bullion with prices hitting successive record highs. The company is expected to outline its plans in February during its Q4 earnings.

0

|0