Catalysts

About Nayax

Nayax provides an end to end cashless payments and commerce enablement platform for automated and self service retail globally.

What are the underlying business or industry changes driving this perspective?

- Rapid adoption of EV charging, car wash, amusement and other higher ticket unattended verticals is lifting transaction value per device and processing revenue. This may support sustained double digit top line growth and higher gross profit dollars.

- The global shift from cash to digital and contactless payments, combined with Nayax's expanding installed base of more than 1.4 million connected devices, is driving recurring processing and SaaS revenue toward a larger share of the mix and supporting rising EBITDA margins.

- The scaling of next generation hardware such as VPOS Media and embedded UNO Mini readers with OEM partners in EV charging and smart coolers broadens the addressable market and may accelerate hardware revenue while maintaining hardware margins in the low to mid 30 percent range.

- Expansion into embedded banking, working capital solutions and e commerce for EV and retail customers is expected to increase ARPU and deepen customer relationships, which may support higher recurring revenue per customer and improved net income over time.

- Disciplined M&A focused on Latin America, Europe and high value software and distribution assets, together with strong organic growth, is positioned to help drive revenue toward management's 2028 targets while leveraging operating expenses and enhancing free cash flow generation.

Assumptions

This narrative explores a more optimistic perspective on Nayax compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts. How have these above catalysts been quantified?

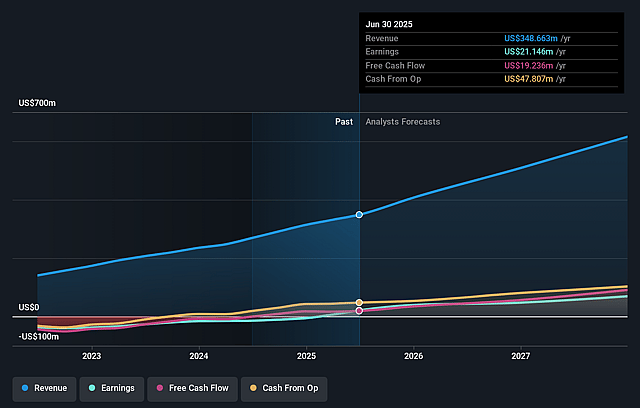

- The bullish analysts are assuming Nayax's revenue will grow by 25.6% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from 6.5% today to 10.7% in 3 years time.

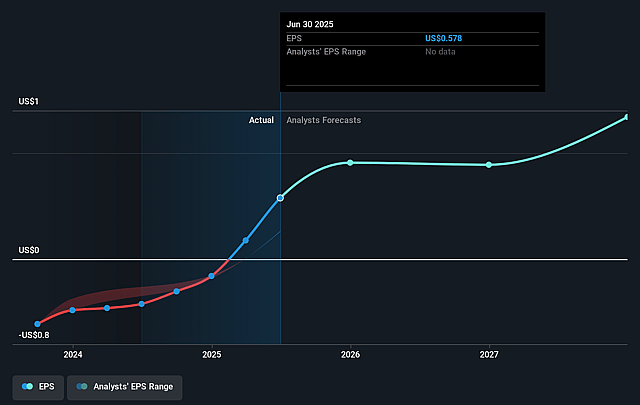

- The bullish analysts expect earnings to reach $78.6 million (and earnings per share of $1.59) by about December 2028, up from $24.0 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $64.9 million.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 37.7x on those 2028 earnings, down from 72.0x today. This future PE is greater than the current PE for the IL Electronic industry at 16.4x.

- The bullish analysts expect the number of shares outstanding to grow by 1.35% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 10.88%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- Long-term growth targets rely heavily on continued rapid expansion in EV charging, car wash, smart coolers and arcade gaming. Any slowdown in EV adoption, changes in consumer behavior, or reduced rollout pace from OEM partners like Autel and cooler manufacturers could limit transaction volumes and device sales, putting sustained double digit revenue growth and processing revenue expansion at risk.

- The strategy assumes ongoing success in consolidating payment volumes under a small group of acquirers and continuously improving smart routing. Structural changes in interchange regulation, pricing pressure from acquirers or weaker negotiating leverage in a more competitive payments landscape could cap or reverse recent processing margin gains and stall net margin expansion.

- Management’s 2028 plan depends on meaningful inorganic revenue contribution and disciplined but active M&A. Repeated delays in closing acquisitions and potential challenges integrating targets across Latin America, Europe and other regions could leave the business more reliant on organic growth than forecast, reducing the likelihood of achieving its long-term revenue and EBITDA margin ambitions and constraining earnings growth.

- The shift into embedded banking, working capital solutions and e commerce introduces new credit, compliance and execution risks. If these products face regulatory setbacks, slower than expected adoption or higher loss rates, they may fail to deliver the expected uplift in ARPU and recurring revenue per customer and instead weigh on net income.

- Nayax’s model is increasingly exposed to macro and competitive dynamics in unattended and self service retail worldwide. Prolonged economic weakness, intensified competition including consolidation among U.S. rivals, or merchant pushback on fees could lead to slower customer additions, higher churn from price sensitive small merchants and weaker pricing power, which would pressure long-term revenue growth and EBITDA margins.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bullish price target for Nayax is ₪180.44, which represents up to two standard deviations above the consensus price target of ₪152.62. This valuation is based on what can be assumed as the expectations of Nayax's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₪180.44, and the most bearish reporting a price target of just ₪124.8.

- In order for you to agree with the more bullish analyst cohort, you'd need to believe that by 2028, revenues will be $732.2 million, earnings will come to $78.6 million, and it would be trading on a PE ratio of 37.7x, assuming you use a discount rate of 10.9%.

- Given the current share price of ₪150.0, the analyst price target of ₪180.44 is 16.9% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Nayax?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.