Advertisement

- United States

- /

- Semiconductors

- /

- NasdaqGS:QCOM

QUALCOMM (NasdaqGS:QCOM) Capitalizes on AI and Automotive Growth Amid Huawei Export License Challenge

QUALCOMM has recently showcased its financial resilience and strategic agility, reporting strong fiscal Q3 performance and making significant strides in automotive and IoT sectors. However, challenges such as the revocation of its license to export to Huawei and slower-than-desired growth rates present hurdles. In the following discussion, we will delve into QUALCOMM's core strengths, critical weaknesses, strategic opportunities, and potential threats to provide a comprehensive analysis of its market position and future prospects.

Click here to discover the nuances of QUALCOMM with our detailed analytical report.

Strengths: Core Advantages Driving Sustained Success for QUALCOMM

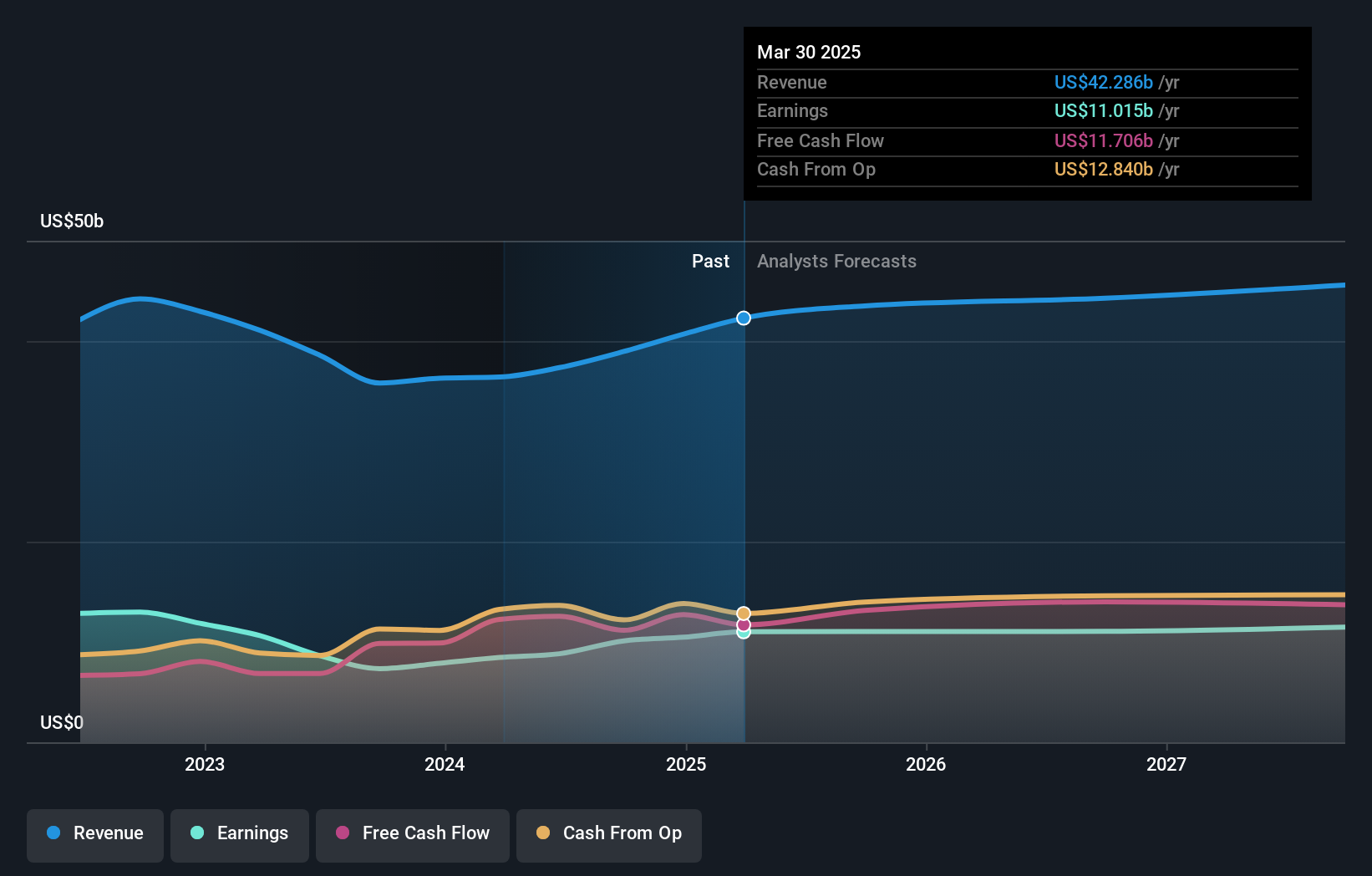

QUALCOMM has demonstrated robust financial health and strategic agility, underscored by its recent performance. In fiscal Q3, the company reported non-GAAP revenues of $9.4 billion and non-GAAP earnings per share of $2.33, surpassing the midpoint of its guidance range, as noted by President and CEO Cristiano Amon in the latest earnings call. The company's diversification strategy, particularly in automotive and IoT sectors, has yielded significant results, with more than 10 new design wins with global automakers in the recent quarter. Additionally, QUALCOMM's focus on AI integration, extending its industry-leading on-device AI solutions to the Snapdragon Digital Chassis, positions it well for future growth. The company's strong market position is further solidified by its substantial stockholder returns, including $1.3 billion in stock repurchases and $949 million in dividends, as highlighted by CFO Akash Palkhiwala. Moreover, QUALCOMM is currently trading at $167.73, significantly below the estimated fair value of $268.72, indicating it may be undervalued in the market. To dive deeper into how QCOM's valuation metrics are shaping its market position, check out our detailed analysis of QCOM's Valuation.

Weaknesses: Critical Issues Affecting QUALCOMM's Performance and Areas for Growth

Despite its strengths, QUALCOMM faces several challenges that could impact its performance. The revocation of its license to export products to Huawei, effective from May 7, will affect revenues in the current and first fiscal quarter of 2025, as stated by CFO Akash Palkhiwala. Additionally, the company expects QCT automotive revenues to remain flat in the fourth fiscal quarter, reflecting market challenges. QUALCOMM's forecasted revenue growth of 8.8% per year is slower than the desired 20% per year, and its earnings growth of 11.2% per year is below the US market average of 15.3% per year. These figures suggest that while QUALCOMM is growing, it is not keeping pace with broader market expectations. Furthermore, the company's current net profit margins of 23.6%, though improved from last year's 22.5%, still indicate room for enhancement. For a more comprehensive look at how these weaknesses could impact QUALCOMM's financial stability, explore our section on the company's Past Performance.

Opportunities: Potential Strategies for Leveraging Growth and Competitive Advantage

QUALCOMM has several strategic opportunities to enhance its market position and capitalize on emerging trends. The expansion into AI PCs, with an expectation that at least 50% of PCs will be AI capable by 2027, presents a significant growth avenue. Amon also highlighted the company's progress towards its $4 billion target in automotive sector revenues by 2026. Collaboration with industry giants like Aramco on connectivity, AI, and advanced computing solutions for industrial and enterprise use cases further strengthens QUALCOMM's market presence. Additionally, the anticipated acceleration in demand for extended and mixed reality devices, driven by new Gen AI use cases, offers another promising growth frontier. These strategic initiatives could significantly bolster QUALCOMM's revenue and market share in the coming years.

Threats: Key Risks and Challenges That Could Impact QUALCOMM's Success

QUALCOMM faces several external threats that could hinder its growth and market share. The competitive landscape in AI and automotive sectors is intensifying, with the company aiming to position itself as a top silicon supplier for these devices, as noted by Amon. Regulatory risks also pose a significant challenge, particularly with long-term agreements like the one extended by Apple through 2027. Economic factors, such as the flat to slightly up forecast for the total handset market from 2023 to 2024, as highlighted by Palkhiwala, could also impact QUALCOMM's revenue streams. Additionally, the company's past earnings growth of 1.7% over the last year, although better than the semiconductor industry's -8.2%, is below its 5-year average of 16.4%, indicating potential volatility in its growth trajectory. These factors underscore the need for strategic vigilance to navigate the evolving market dynamics effectively.

Conclusion

In conclusion, QUALCOMM exhibits a strong financial foundation and strategic adaptability, as evidenced by its solid Q3 performance and successful diversification into the automotive and IoT sectors. Despite facing challenges such as the Huawei export license revocation and slower-than-desired revenue and earnings growth, the company is well-positioned to capitalize on emerging opportunities in AI PCs, automotive, and extended reality markets. However, it must navigate competitive and regulatory risks to sustain its growth trajectory. Given that QUALCOMM is currently trading at $167.73, significantly below its estimated fair value of $268.72, the market may not fully recognize its potential, suggesting a promising outlook for future performance if the company can effectively leverage its strengths and address its weaknesses.

Already own QCOM? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

Valuation is complex, but we're here to simplify it.

Discover if QUALCOMM might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Simply Wall St and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

About NasdaqGS:QCOM

QUALCOMM

Engages in the development and commercialization of foundational technologies for the wireless industry worldwide.

Flawless balance sheet established dividend payer.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

74 followersusers have followed this narrative

7 commentsusers have commented on this narrative

21 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$121.2% undervalued

13 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$245.0% overvalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

NO

Norms70 on Standard Lithium ·

SLI is share to watch next 5 years

Fair Value:€4.59.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

davidlsander on Beam Therapeutics ·

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value:US$15081.9% undervalued

59 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RedhawkCC on Prime Medicine ·

PRME remains a long shot but publication in the New England Journal of Medicine helps.

Fair Value:US$0.0469.1k% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

118 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3925.9% undervalued

962 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

74 followersusers have followed this narrative

7 commentsusers have commented on this narrative

21 likesusers have liked this narrative