- United States

- /

- Semiconductors

- /

- NasdaqGS:PLAB

Photronics (PLAB): Assessing Valuation After a Sharp Short-Term Rally

Reviewed by Simply Wall St

Photronics (PLAB) has quietly turned into one of those under the radar chip enablers powering the broader semiconductor cycle, and its recent share performance now has investors asking whether the run still has room.

See our latest analysis for Photronics.

With the share price now at $33.09, Photronics has cooled off a bit after a sharp run, but a 57.12 percent one month share price return and 38.74 percent one year total shareholder return still point to momentum that investors clearly have not ignored.

If Photronics has you thinking about where the next quiet outperformer might come from, it could be worth exploring high growth tech and AI stocks as a curated way to spot similar stories early.

Yet despite that strong run, the stock still trades roughly 31 percent below the average analyst price target. This raises the key question: Is Photronics undervalued or already reflecting its next leg of growth?

Most Popular Narrative: 18.3% Undervalued

Compared with Photronics' last close at $33.09, the most followed narrative pegs fair value meaningfully higher at $40.50, framing the current discount as opportunity rather than excess.

Strategic investments in U.S. capacity and cutting edge production (multi beam mask writer and Texas facility expansion) position Photronics to benefit as major semiconductor fabrication and reshoring initiatives are realized, supporting future revenue growth and margin expansion.

Curious how modest tweaks to growth, margins and the future earnings multiple combine into a much richer valuation story than the share price implies? The narrative blends upgraded revenue trajectories with a punchier profit multiple, then layers in capital intensity and discounting assumptions to justify that higher fair value. Want to see which specific top line path and earnings profile have to materialize to close the gap?

Result: Fair Value of $40.50 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, sustained heavy capex and unpredictable demand swings, especially in Asia, could pressure cash flows and undermine the upgraded growth and valuation narrative.

Find out about the key risks to this Photronics narrative.

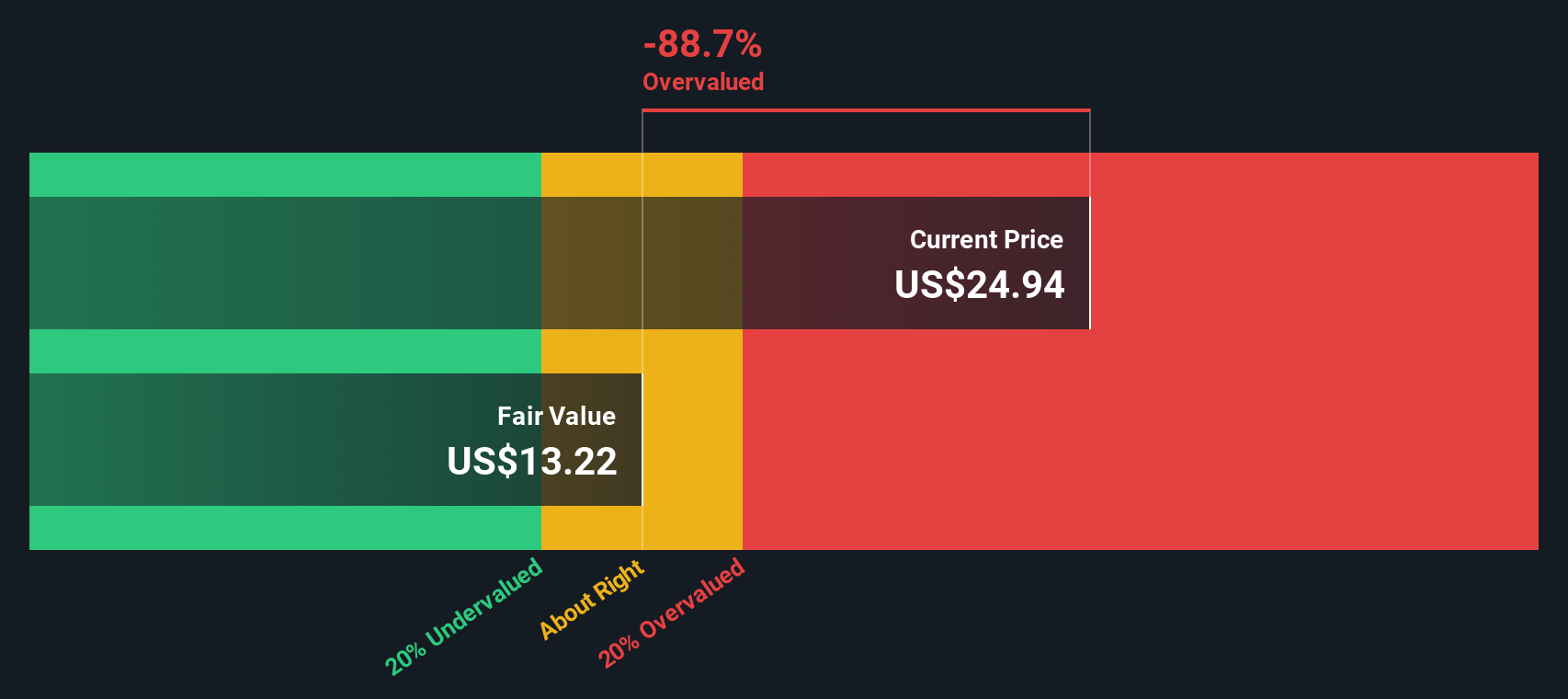

Another View: DCF Flags Overvaluation

While narratives and analyst targets point to upside, our DCF model paints a cooler picture. It suggests fair value nearer $19.15, which is well below the current $33.09 share price and may imply that Photronics is overvalued. Which set of assumptions do you trust more?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Photronics for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 910 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Photronics Narrative

If you see the story differently or want to stress test your own assumptions, you can build a custom narrative in just a few minutes: Do it your way.

A great starting point for your Photronics research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you are serious about compounding your returns, do not stop at Photronics. Use the Simply Wall Street Screener now to uncover your next edge.

- Amplify your growth focus by targeting these 24 AI penny stocks that are shaping the next wave of intelligent software, automation, and data driven infrastructure.

- Secure potential bargains early through these 910 undervalued stocks based on cash flows that pair strong fundamentals with prices still lagging behind their intrinsic value.

- Strengthen your income strategy by hunting for these 12 dividend stocks with yields > 3% that can keep cash flowing into your portfolio year after year.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:PLAB

Photronics

Engages in the manufacture and sale of photomask products and services in the United States, Taiwan, China, Korea, Europe, and internationally.

Flawless balance sheet and fair value.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion