Advertisement

- United States

- /

- Semiconductors

- /

- NasdaqGS:ON

Is ON Semiconductor Set for a Comeback After Recent EV Partnerships and Price Drop?

Simply Wall St

Reviewed by Bailey Pemberton

- Ever wondered if ON Semiconductor might offer surprising value right now? Let’s dig into what’s really happening beneath the surface before you make your next move.

- The shares have been on a rollercoaster lately, dropping 4.9% over the last week even after a small 1.6% bounce over the past month, and are still down 18.8% year-to-date.

- Market sentiment seems to be shifting as big headlines, like the expanding push into electric vehicles and partnerships with major automakers, continue to make waves for ON Semiconductor. These developments are feeding speculation about the company’s growth profile and how much risk investors are really taking on.

- On our valuation checks, ON Semiconductor earns a 3 out of 6 for being undervalued. Let’s dive into what that means and stick around for a better way to see ON’s true worth before we wrap up.

Find out why ON Semiconductor's -27.9% return over the last year is lagging behind its peers.

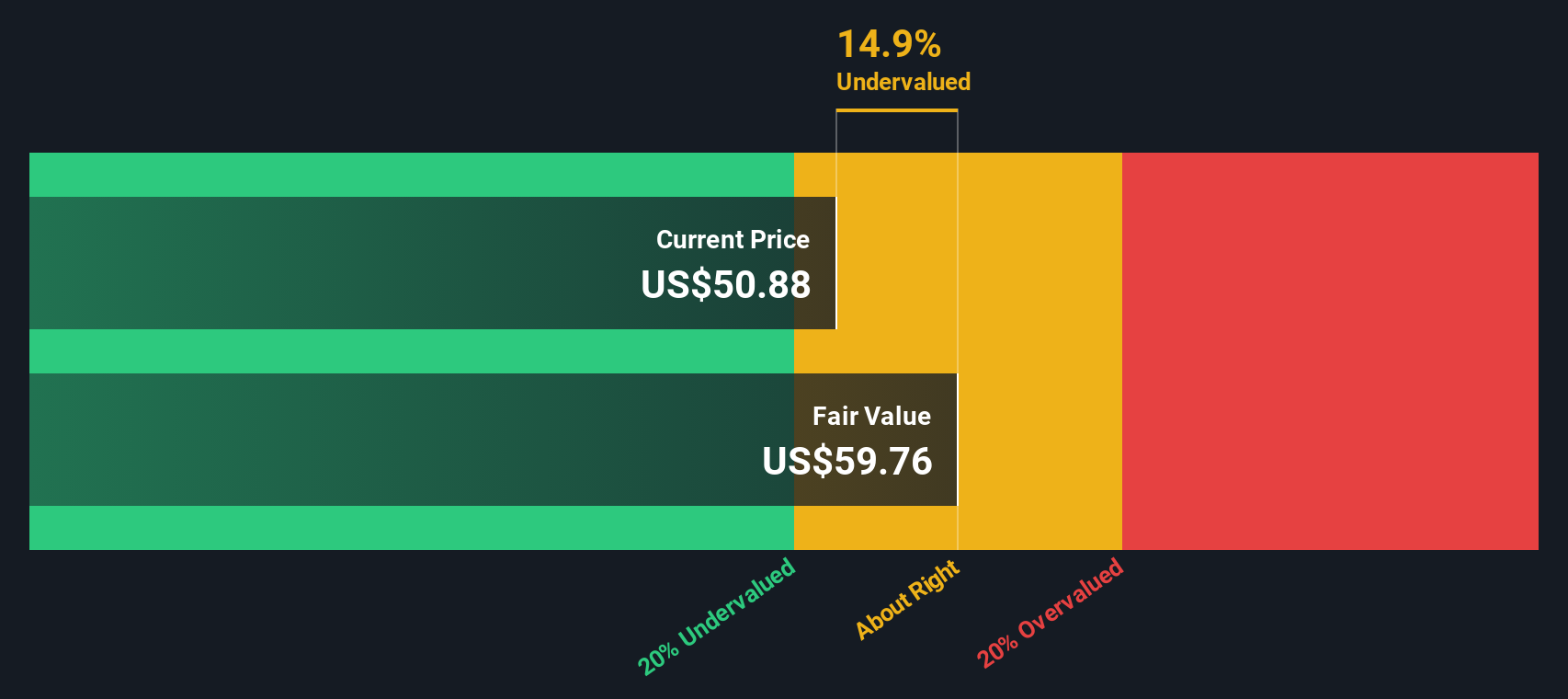

Approach 1: ON Semiconductor Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model is a common method investors use to estimate a stock’s intrinsic value by projecting the company’s future cash flows and discounting them back to today’s value. This approach looks beyond short-term market swings and focuses on how much cash ON Semiconductor is expected to generate over the coming years.

According to the DCF analysis, ON Semiconductor posted a free cash flow of $961.7 million over the last twelve months. Analyst forecasts suggest that annual free cash flow will grow significantly, reaching approximately $2.33 billion by 2029. Projections for the next ten years, with inputs from both analysts and internal estimates, help build a more complete picture of the long-term cash potential.

After extrapolating these cash flows using a 2 Stage Free Cash Flow to Equity model and discounting them appropriately, the estimated intrinsic value for ON Semiconductor comes out to $59.78 per share. With the current share price trading about 16.2% below this estimate, the DCF suggests the stock is undervalued at present.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests ON Semiconductor is undervalued by 16.2%. Track this in your watchlist or portfolio, or discover 845 more undervalued stocks based on cash flows.

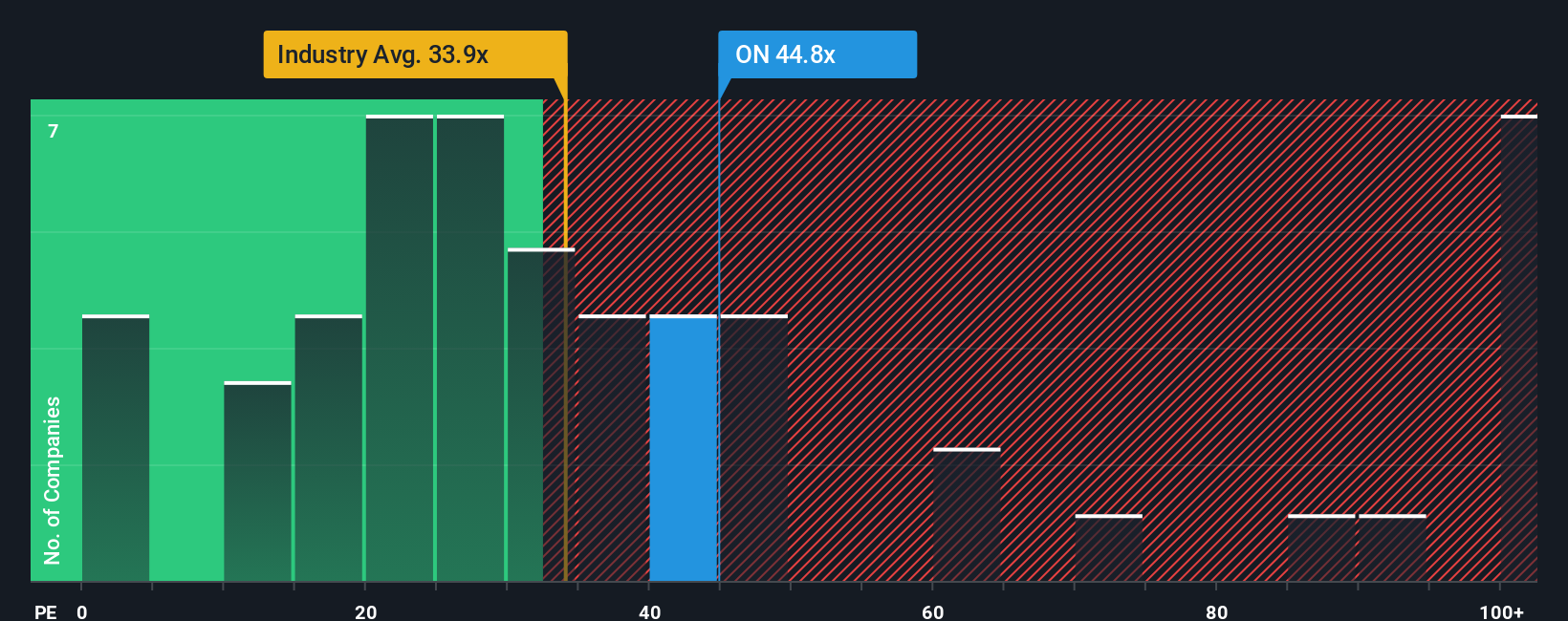

Approach 2: ON Semiconductor Price vs Earnings

For profitable companies like ON Semiconductor, the Price-to-Earnings (PE) ratio is a favored tool for valuation. It relates the company's current share price to its earnings per share, showing how much investors are willing to pay for a dollar of profits. A higher PE can suggest the market expects faster growth or sees less risk, while a lower PE might signal the opposite.

ON Semiconductor currently trades at a PE ratio of 44x. That is noticeably higher than the semiconductor industry average of 36.1x, but below the average of its listed peers, which comes in at 51.7x. These simple comparisons help put ON’s valuation in context, but they do not take all of the company-specific factors into account.

This is where Simply Wall St's "Fair PE Ratio" comes in. Unlike a plain industry or peer comparison, the Fair Ratio (here, 47.9x) takes into account ON's earnings outlook, profit margins, industry positioning, market cap, and risk profile. This tailored approach offers a more balanced view of what a reasonable valuation should be for ON in today’s market.

With ON’s current PE of 44x being close to its Fair Ratio of 47.9x, the stock looks to be valued about right based on this metric. While not deeply discounted, it also is not trading at unreasonable levels given the company’s fundamentals and outlook.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1412 companies where insiders are betting big on explosive growth.

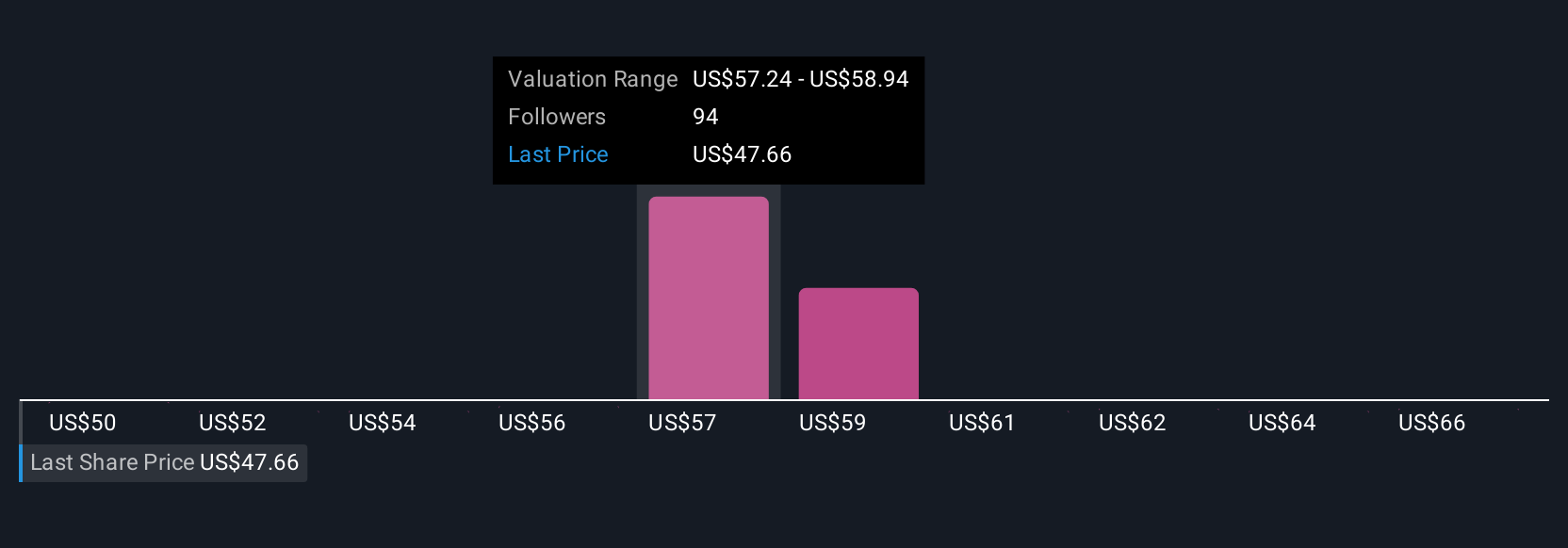

Upgrade Your Decision Making: Choose your ON Semiconductor Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. Narratives are simply the stories you form about a company, your own perspective on how ON Semiconductor’s business will evolve, including your assumptions about its future revenue, profit margins and ultimately its fair value.

Unlike traditional metrics that only show you the numbers, Narratives help you connect the company’s unique story, such as expanding into electric vehicles, shifting product mix, or facing market risks, to your financial forecast, resulting in a more personalized and actionable estimate of fair value. This method is designed to be easy and accessible, and millions of investors use Narratives every day on the Simply Wall St Community page to guide their decisions.

Narratives make it simple to decide when to buy or sell. Just compare your own Fair Value to the current Price, and Narratives are automatically updated as new news or earnings are released. For ON Semiconductor, for example, investors might set a Fair Value as high as $70 if they’re optimistic about AI and EV growth, or as low as $40 if they're concerned about market risks. This gives you a transparent way to see where your view sits on the spectrum.

Do you think there's more to the story for ON Semiconductor? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:ON

ON Semiconductor

Provides intelligent sensing and power solutions in Hong Kong, Singapore, the United Kingdom, the United States, and internationally.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor