- United States

- /

- Semiconductors

- /

- NasdaqGM:MRAM

Is Everspin Technologies (NASDAQ:MRAM) Using Too Much Debt?

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that Everspin Technologies, Inc. (NASDAQ:MRAM) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for Everspin Technologies

What Is Everspin Technologies's Debt?

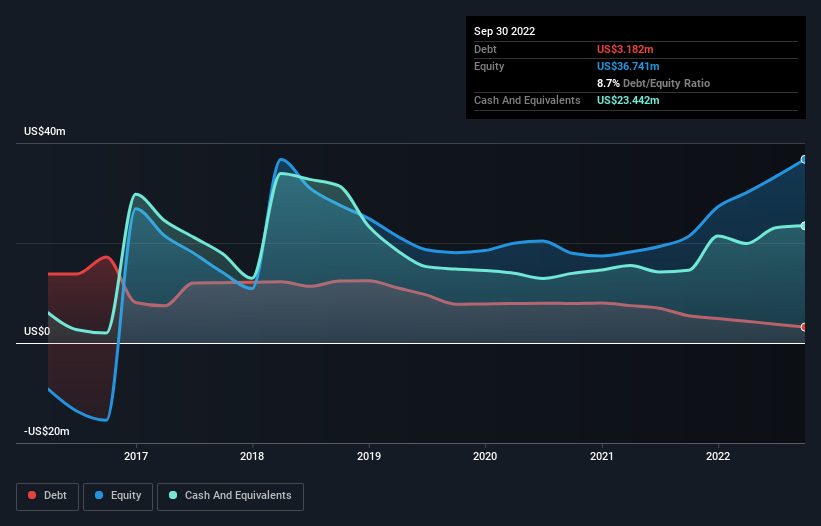

You can click the graphic below for the historical numbers, but it shows that Everspin Technologies had US$3.18m of debt in September 2022, down from US$5.46m, one year before. But it also has US$23.4m in cash to offset that, meaning it has US$20.3m net cash.

A Look At Everspin Technologies' Liabilities

The latest balance sheet data shows that Everspin Technologies had liabilities of US$11.0m due within a year, and liabilities of US$6.08m falling due after that. Offsetting these obligations, it had cash of US$23.4m as well as receivables valued at US$12.6m due within 12 months. So it actually has US$19.0m more liquid assets than total liabilities.

This surplus suggests that Everspin Technologies is using debt in a way that is appears to be both safe and conservative. Because it has plenty of assets, it is unlikely to have trouble with its lenders. Simply put, the fact that Everspin Technologies has more cash than debt is arguably a good indication that it can manage its debt safely.

Even more impressive was the fact that Everspin Technologies grew its EBIT by 14,686% over twelve months. That boost will make it even easier to pay down debt going forward. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Everspin Technologies's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. Everspin Technologies may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Over the last two years, Everspin Technologies actually produced more free cash flow than EBIT. There's nothing better than incoming cash when it comes to staying in your lenders' good graces.

Summing Up

While it is always sensible to investigate a company's debt, in this case Everspin Technologies has US$20.3m in net cash and a decent-looking balance sheet. The cherry on top was that in converted 125% of that EBIT to free cash flow, bringing in US$8.9m. The bottom line is that we do not find Everspin Technologies's debt levels at all concerning. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. Be aware that Everspin Technologies is showing 3 warning signs in our investment analysis , and 1 of those is significant...

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if Everspin Technologies might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGM:MRAM

Everspin Technologies

Manufactures and sells magnetoresistive random access memory (MRAM) technologies in the United States, Japan, Hong Kong, Germany, Singapore, China, Canada, and internationally.

Flawless balance sheet with moderate growth potential.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

15,000% Nevada's Gold Miner Play

A great prediction written on the 21st of July 2025

Best bet on Rare Earth - Currently priced to perfection, invest if thesis holds at $35-40

Popular Narratives

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion