Advertisement

- United States

- /

- Semiconductors

- /

- NasdaqGS:MCHP

How Microchip’s TimePictra 12 Software Pivot At Microchip Technology (MCHP) Has Changed Its Investment Story

Reviewed by Sasha Jovanovic

- Earlier in June 2026, Microchip Technology launched TimePictra 12, a major software upgrade that enhances synchronization management, automation, and visibility for large-scale critical infrastructure timing networks, integrating technologies like BlueSky and SkyWire for precise clock alignment and GNSS monitoring.

- This release effectively broadens Microchip’s timing portfolio beyond hardware, positioning its software platform as a central control layer for complex, high-accuracy network timing architectures across telecoms, data centers, and other infrastructure-heavy sectors.

- Next, we’ll examine how TimePictra 12’s focus on critical infrastructure synchronization could influence Microchip Technology’s existing investment narrative and outlook.

Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

Microchip Technology Investment Narrative Recap

To own Microchip Technology, you generally need to believe in its role as a provider of embedded control and timing solutions across critical infrastructure, industrial and automotive markets. The launch of TimePictra 12 supports that timing and software narrative, but it does not materially change near term catalysts that are still centered on inventory normalization and margin recovery, nor the key risk around elevated leverage and interest costs pressuring earnings and capital allocation flexibility.

The TimePictra 12 release fits alongside Microchip’s recent roll out of PCIe 6.0 and CXL 3.1 XpressConnect retimers, both aimed at high performance, data intensive systems such as AI data centers. Together, these announcements highlight a push to serve infrastructure customers that require reliable timing, secure connectivity and power efficient performance, which could be important as the company works through inventory reductions and seeks to support its guidance for improving profitability.

Yet, against this potential, investors should be aware of the ongoing risk that elevated inventories and related write offs could still...

Read the full narrative on Microchip Technology (it's free!)

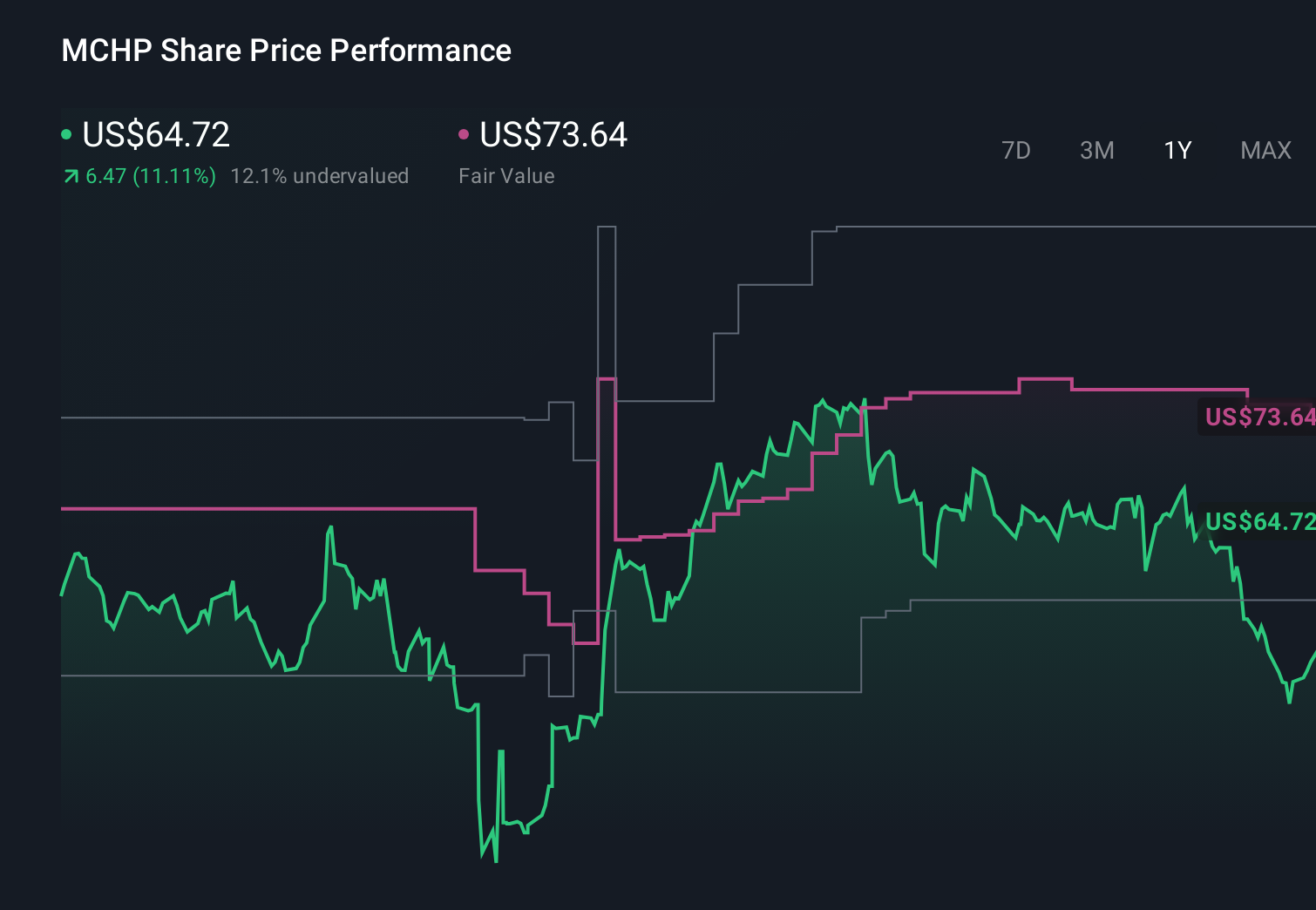

Microchip Technology's narrative projects $7.3 billion revenue and $1.9 billion earnings by 2029.

Uncover how Microchip Technology's forecasts yield a $86.67 fair value, a 16% downside to its current price.

Exploring Other Perspectives

Compared with consensus, the most pessimistic analysts saw 2029 revenue around US$7.2 billion and earnings of US$2.0 billion, yet still flagged that prolonged inventory corrections and restructuring costs could weigh heavily, so you should treat TimePictra 12 as one piece of evidence and compare how it fits with both the upbeat and bearish views before deciding which story feels more realistic.

Explore 5 other fair value estimates on Microchip Technology - why the stock might be worth 34% less than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Microchip Technology research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Microchip Technology research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Microchip Technology's overall financial health at a glance.

Curious About Other Options?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 30 companies in the world exploring or producing it. Find the list for free.

- Capitalize on the AI infrastructure supercycle with our selection of the 49 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:MCHP

Microchip Technology

Develops, manufactures, and sells smart, connected, and secure embedded control solutions in the Americas, Europe, and Asia.

High growth potential second-rate dividend payer.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Conexeu Sciences ·

This small biotech is developing technology that could potentially change how tissue is rebuilt

Fair Value:US$25.3451.9% undervalued

49 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

HE

HedgeY on Quanta Services ·

The Picks-and-Shovels Leader of the Grid Supercycle

Fair Value:US$7104.2% overvalued

52 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

FU

FundamentalFlow on Karman Holdings ·

KRMN — Karman Space & Defense: Down 58% from Peak, Is the Market Mispricing a Hypergrowth Defense Compounder?

Fair Value:US$105.654.8% undervalued

34 followersusers have followed this narrative

2 commentsusers have commented on this narrative

16 likesusers have liked this narrative

DO

Double_Bubbler on Invinity Energy Systems ·

Invinity Energy Systems: All About That BESS

Fair Value:UK£161.9% undervalued

40 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

Recently Updated Narratives

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’sMost Mispriced AI Story

Fair Value:US$7.551.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BR

browser on Space Exploration Technologies ·

SpaceX: A Sober Look at Catalysts, Risks, and Long‑Term Value After the IPO

Fair Value:US$0.4633.5k% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on Abitibi Metals ·

Abitibi Metals’ High-Grade B26 Polymetallic Deposit Trading at a Fraction of Peers, 96% Undervalued?

Fair Value:CA$1.2949.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7443.8% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9639.1% undervalued

60 followersusers have followed this narrative

9 commentsusers have commented on this narrative

17 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1928.8% undervalued

52 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative