Advertisement

- United States

- /

- Semiconductors

- /

- NasdaqGS:LSCC

Is Lattice Semiconductor’s Surge Justified After New Partnerships and a 40% Rally?

Simply Wall St

Reviewed by Bailey Pemberton

- Wondering if Lattice Semiconductor is worth a closer look? You're not alone, especially with investors buzzing about its current price compared to future prospects.

- The stock has climbed 30.4% year-to-date and soared 40.6% over the last year, highlighting a powerful blend of momentum and changing sentiment.

- In recent weeks, the company has been in the spotlight thanks to strong industry demand for programmable chips, as well as new partnerships with major tech firms. These announcements have fueled optimism around Lattice's strategic position in the rapidly evolving semiconductor landscape.

- But here's where it gets interesting: Lattice currently scores 0 out of 6 on our valuation checks, indicating it may be fully valued by traditional measures. We'll break down how those scores are calculated and hint at a smarter approach to valuation that could reshape your view by the end of this article.

Lattice Semiconductor scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Lattice Semiconductor Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company's intrinsic value by projecting its future cash flows and discounting them to reflect today's dollars. This approach gives investors a way to look beyond headline profits and focus on a company's ability to generate real cash over time.

For Lattice Semiconductor, the DCF uses a two-stage Free Cash Flow to Equity model. Currently, the company is generating Free Cash Flow of $129.2 million, with analysts projecting rapid growth in coming years. For example, by 2027, cash flow is expected to reach $228.9 million, and over the next decade, Simply Wall St extrapolates further annual increases, with discounted estimates ranging from around $188.9 million in 2026 to $125.7 million in 2035. All figures are in US dollars.

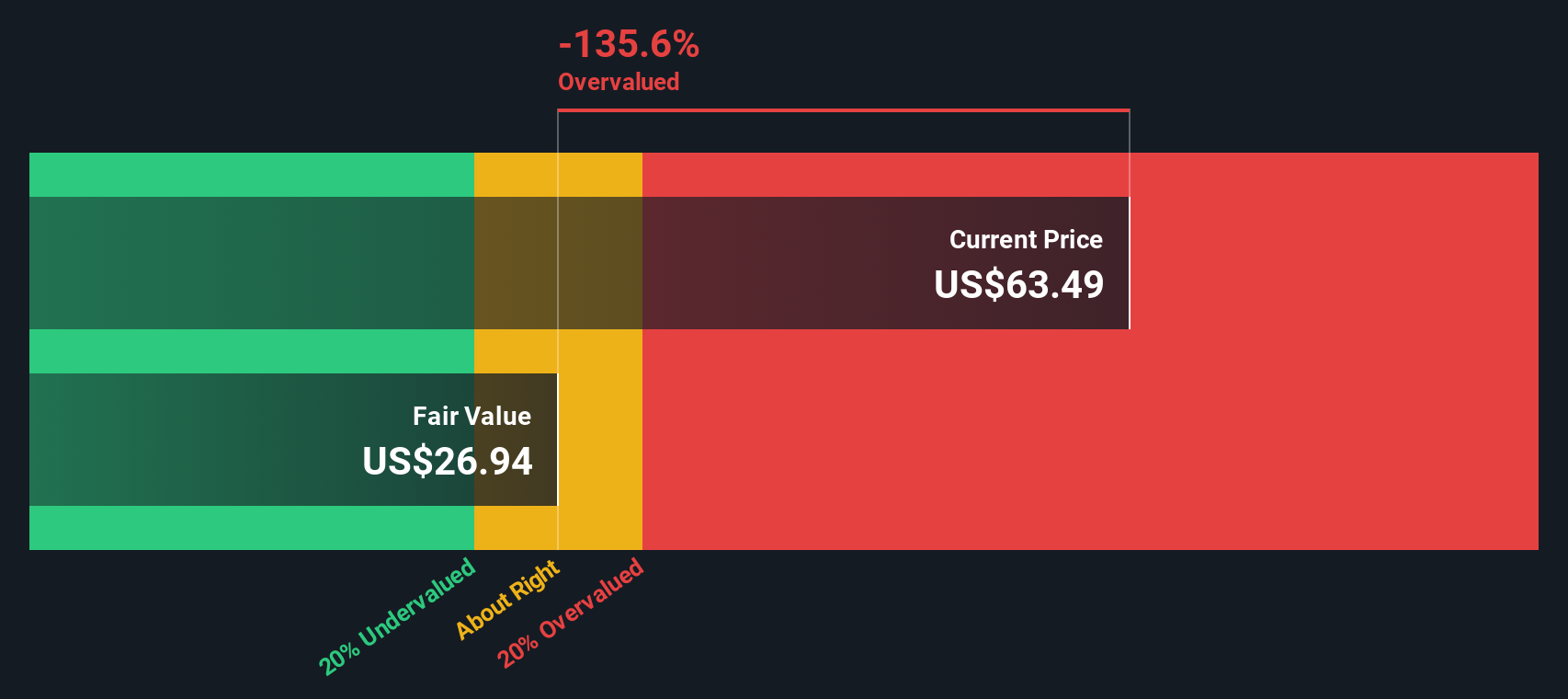

Bringing these forecasts together, the DCF calculation suggests an intrinsic value of $25.30 per share. However, with Lattice's actual share price currently well above this mark, the DCF model indicates the stock is about 188% overvalued relative to its projected cash flows. Investors should note that this is a significant premium and suggests the market may already be pricing in very optimistic assumptions for the future.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Lattice Semiconductor may be overvalued by 188.4%. Discover 839 undervalued stocks or create your own screener to find better value opportunities.

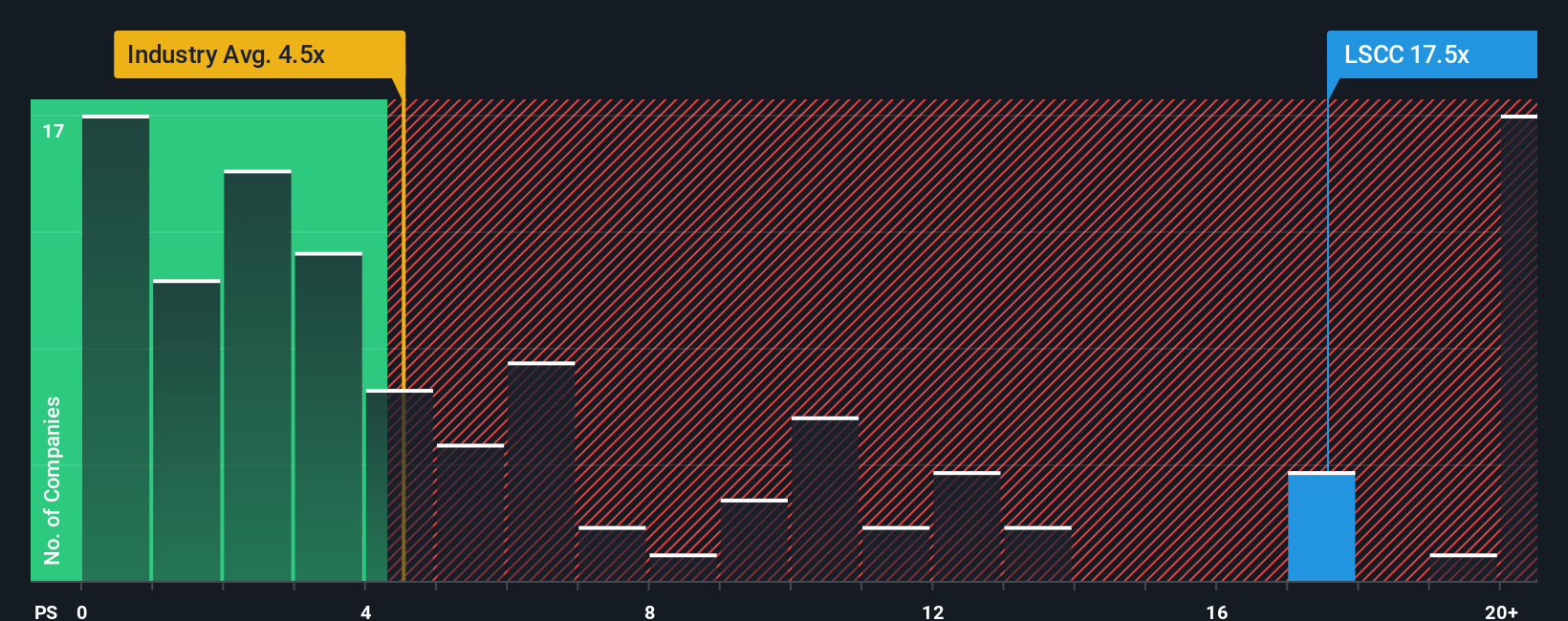

Approach 2: Lattice Semiconductor Price vs Sales

The price-to-sales (P/S) ratio is a widely used valuation tool for profitable companies, especially in dynamic industries like semiconductors where revenue growth often outpaces immediate profits. Since it compares a company’s market capitalisation to its total sales, the P/S ratio gives investors a way to assess value without being skewed by accounting variations or short-term profitability fluctuations.

Expectations for future growth and perceived business risks play a large part in shaping what a “normal” or “fair” P/S ratio should look like for any company. High-growth firms and those with stronger competitive positions usually command higher P/S multiples, reflecting investors’ willingness to pay more for each dollar of sales. Conversely, heightened risks or slowing growth put downward pressure on this ratio.

Currently, Lattice Semiconductor trades at a P/S ratio of 20.44x, which dwarfs both the semiconductor industry average of 5.31x and the peer average of 10.29x. At first glance, this could point to overvaluation. However, Simply Wall St introduces a “Fair Ratio” in this case, 9.34x which is calculated with a proprietary model factoring in Lattice’s sales growth, profit margins, industry conditions, market cap, and specific risk profile. This approach goes beyond simple peer group or industry comparisons by considering all the fundamental variables that actually drive a fair trading multiple for the company.

With Lattice’s actual P/S nearly double its Fair Ratio, the conclusion is clear: the stock currently looks significantly overvalued on this basis.

Result: OVERVALUED

PS ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1408 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Lattice Semiconductor Narrative

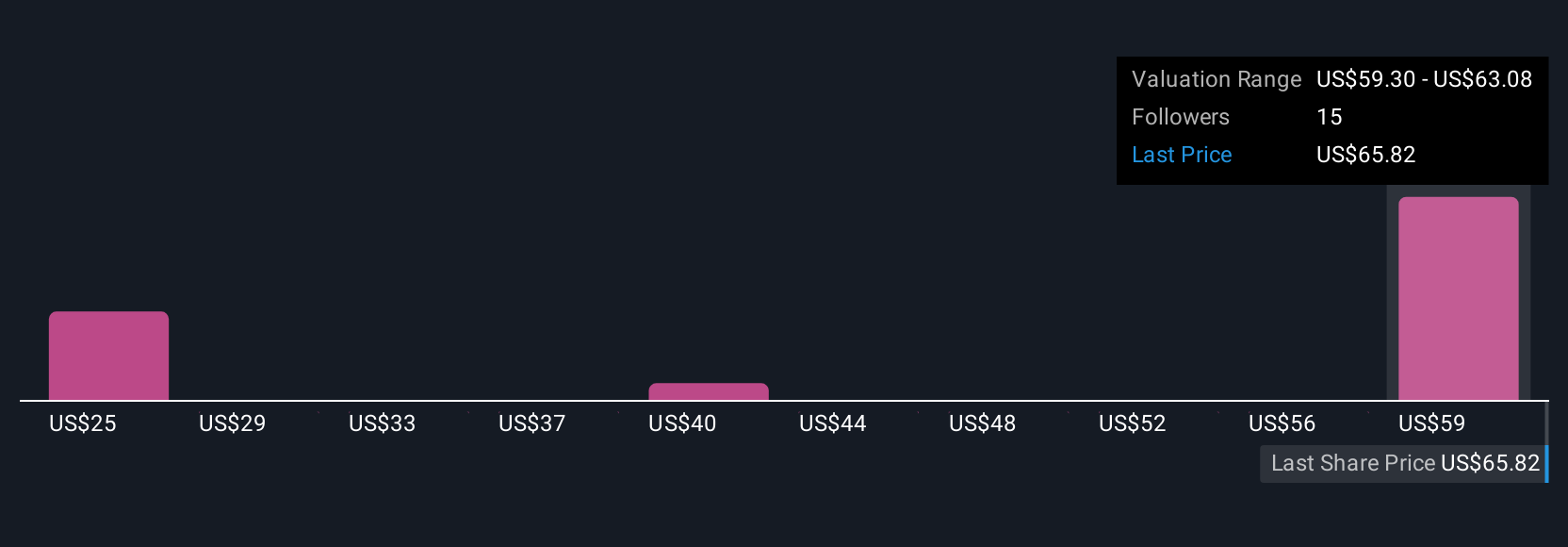

Earlier we mentioned that there's an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is simply a story that ties together your perspective on a business with realistic estimates for its future revenue, earnings, and margins. This ultimately connects the company’s journey to a calculated fair value.

With Narratives, you take the numbers, such as growth rates, profit margins, and risks, and build a forecast while also providing your reasoning. Why do you believe Lattice’s future is bright, or what makes you cautious? Narratives invite you to set assumptions that reflect your own view, making the connection between the "story" and the resulting financial figure clear and personalized.

This approach is accessible right on Simply Wall St’s platform, used by millions of investors in the Community page. When you compare your own Narrative’s Fair Value to the current share price, you can instantly see if Lattice looks like a buy, hold, or sell. Even as news and results change, Narratives are updated dynamically.

For example, one investor with a bullish Narrative for Lattice might believe that booming AI demand and product innovation support a fair value near $72 per share. A more cautious investor, concerned about industry risks, might set their fair value closer to $52. Narratives help you make decisions with confidence, grounded in your own logic and the latest data.

Do you think there's more to the story for Lattice Semiconductor? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:LSCC

Lattice Semiconductor

Develops and sells semiconductor, silicon-based and silicon-enabling, evaluation boards, and development hardware products in Asia, Europe, and the Americas.

Flawless balance sheet with high growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor