Advertisement

- United States

- /

- Semiconductors

- /

- NasdaqGS:LRCX

Stable Earnings Amid Uncertainty - Here is Why Investors are Reconsidering the Lam Research Corporation (NASDAQ:LRCX)

Lam Research Corporation (NASDAQ:LRCX) released earnings recently, and analysts have adjusted their expectations. In this article, we will re-cap the financial performance and compare Lam Research to competitors in the semiconductor industry on a relative basis.

The key takeaways from our analysis are:

- Lam seems to be fairly priced on a PE basis, has stable earnings and implied future earnings growth

- 31% of quarterly revenues are from China, exposing them to current Asian market uncertainty

- The stock kept gaining as the market slumped last week, demonstrating investors confidence after revisiting the fundamentals

Earnings Overview

Earnings season is a great time to test our thesis on a company, and consequently adjust our future expectations. Lam Research published its earnings results on the 20th of April and here are the key highlights:

- Q1 Revenue: US$4.06b - down 4% from Q1 2021

- Net income at US$1.02b, US$4.541 in the last 12 months - up 31.2% from the 12 months prior

- Management expects Q2 revenue to be US$4.2b +/- US$300m

- EPS US$7.3, in line with estimates

After the result, analysts have decreased their price target by 9.7% to US$655, which still implies a 39% upside.

The company saw persistent customer demand - one of their problems was making sure production is keeping up with demand. For this reason, management announced near-term focus to accelerate procurement of parts and continue investment in new products and services.

The geographic distribution of Lam income places 31% of quarterly revenues from China. Given the current uncertainty in the region, the stock may come under pressure until investors are more confident in the stability of operations.

Analysts have made their predictions for the future income of Lam, and it seems that they are expecting revenue growth to pick up late 2023 by 17%, and EPS expected to step up 16% to US$38 in 2023.

Our compiled chart, shows the relationship between current and expected future earnings. As we can see, the stock has been performing well and is expected to keep stable growth in the long term.

View our latest analysis for Lam Research

In order to see what investor can expect from the company, we can compare its performance to the semiconductor industry and other stocks.

Alternatively, we can explore Lam's intrinsic value and see how investors are paying for the future cash flows of the company.

In the segment below, we will compare Lam to related companies for which there is increased momentum.

Peer Comparison

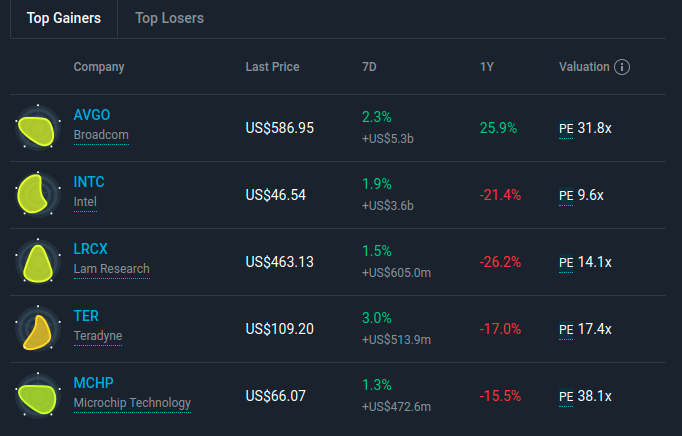

Considering that the market was down by 3.35% last week, finding some gainers may provide a stronger signal of resilience and future potential. While semiconductors were generally in decline, Lam Research managed to stay on the right side of zero along with some peers.

In the chart below, we can see a comparison with other stocks, based on their relative performance and the price which investors are paying for every $1 dollar of earnings.

The semiconductor industry is forecasted to grow annual earnings by 14.5% and has an industry PE of 20.7x. If we drill down to the semiconductor equipment branch, of which Lam is part of - we can see that the median PE is 17.4x and earnings are forecasted to grow by 10.3%.

This gives us a more appropriate baseline with which to compare the metrics below:

The relative comparison reveals that Lam is trading around fair value, and the expected annual earnings growth of 7% give investors an increase to the present value as the cash flows increase with time.

Considering its peers, it seems that Broadcom (NASDAQ:AVGO) and Microchip (NASDAQ:MCHP) are the most exposed to being overbought by investors with a 31.8x and 28.1x PE respectively. The most undervalued PE stock is Intel (NASDAQ:INTC), however it has an expected earnings decline of 6,9% annually.

Conclusion

Lam Research seems to be fairly priced in an industry that has further implied growth. The past 12 months performance has been negative, but the stock has key qualities that make it a good candidate for contrarian investment watchlists.

The stock has some risk exposure, as a sizeable portion of its revenues come from China, which is currently undergoing a hard lockdown across multiple areas with a center in Shanghai.

Supply chain disruptions and high semiconductor demand have the potential to keep prices up as the company develops new projects and relieves supply pressure.

With that in mind, we wouldn't be too quick to come to a conclusion on Lam Research. Long-term earnings power is much more important than next year's profits. We have estimates - from multiple Lam Research analysts - going out to 2024, and you can see them free on our platform here.

That said, it's still necessary to consider the ever-present specter of investment risk. We've identified 1 warning sign with Lam Research , and understanding this should be part of your investment process.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Goran Damchevski and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Goran Damchevski

Goran is an Equity Analyst and Writer at Simply Wall St with over 5 years of experience in financial analysis and company research. Goran previously worked in a seed-stage startup as a capital markets research analyst and product lead and developed a financial data platform for equity investors.

About NasdaqGS:LRCX

Lam Research

Designs, manufactures, markets, refurbishes, and services semiconductor processing equipment used in the fabrication of integrated circuits in the United States, China, Korea, Taiwan, Japan, Southeast Asia, and Europe.

Outstanding track record with flawless balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

44 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8147.4% undervalued

7 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

AU

AuCA on Nova Ljubljanska Banka d.d ·

Nova Ljubljanska Banka d.d will expect a 11.2% revenue boost driving future growth

Fair Value:€20916.5% undervalued

23 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

88 followersusers have followed this narrative

11 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

926 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative