Advertisement

- United States

- /

- Semiconductors

- /

- NasdaqGS:LRCX

Should Investors Reconsider Lam Research After 114% Rally and Next-Gen Chip Expansion News?

Simply Wall St

Reviewed by Bailey Pemberton

- Ever wondered if Lam Research is still a smart buy after all its recent buzz? Let’s cut through the noise and see where value and opportunity might really lie with this stock.

- After powering up 114.2% so far this year and delivering a massive 119.1% return over the past 12 months, the share price suggests investors are pricing in high growth or shifting risk perceptions.

- Market confidence has been bolstered by sector-wide excitement about chip demand and government initiatives supporting semiconductor manufacturers. Recently, Lam Research was highlighted in headlines surrounding new fabrication contracts and expansion into next-generation chip technologies, both of which are fueling speculation about its long-term trajectory.

- Lam Research currently boasts a valuation score of 3 out of 6, based on our comprehensive valuation checks. This means it is undervalued on half the metrics we track. We’ll walk through each valuation approach, but stick around to the end for an even better way to see if Lam Research is truly worth your investment.

Approach 1: Lam Research Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates a company's true worth by forecasting its future cash flows and then "discounting" them back to their value today. This approach aims to reveal the present value of all the money the company is expected to generate in the years ahead.

For Lam Research, the most recent reported Free Cash Flow (FCF) is around $5.7 Billion. Analyst predictions cover cash flow growth for the next five years, after which projections are extrapolated by Simply Wall St. By 2030, Lam’s FCF is expected to reach $7.9 Billion. These rising figures reflect well on the company's operational momentum, but the real test is how these numbers stack up when considering today's share price.

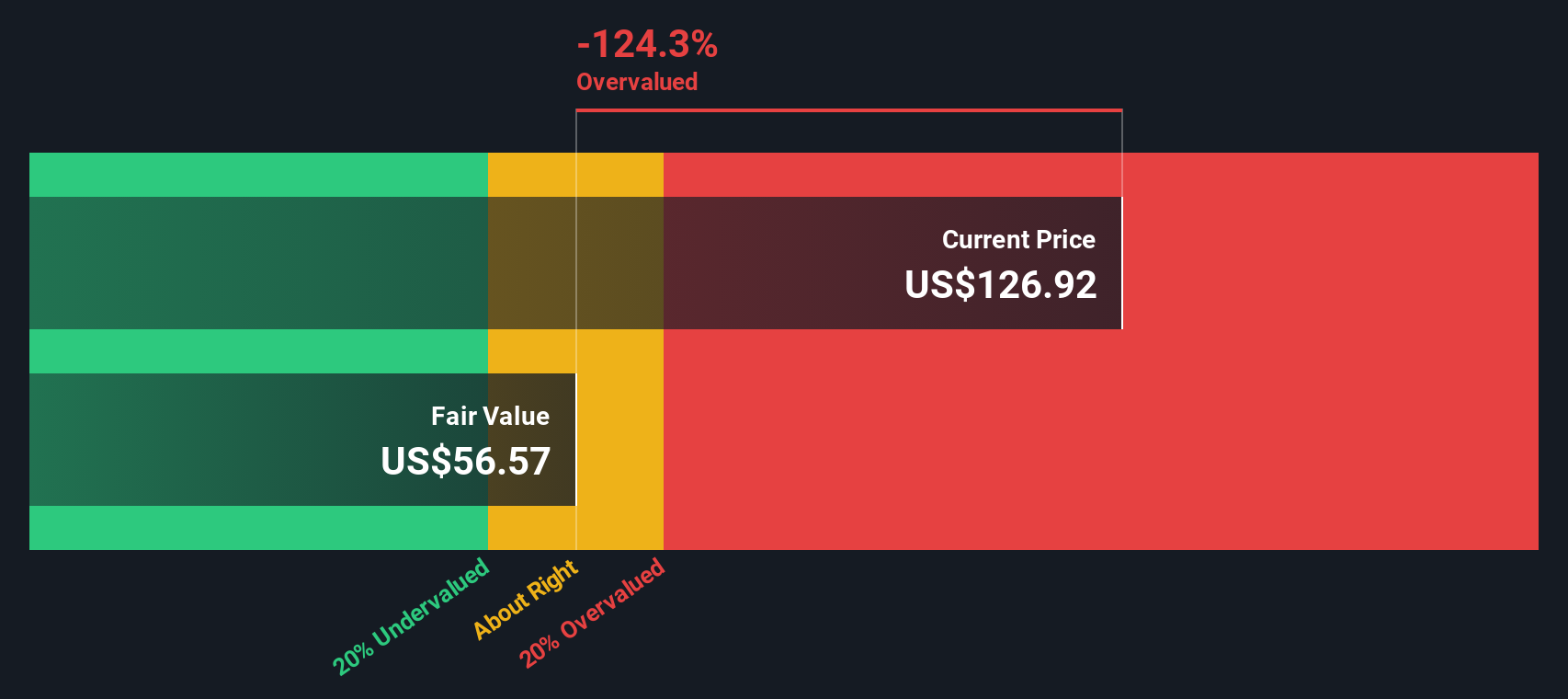

Based on the DCF model's projections and methodology, Lam Research’s estimated intrinsic value comes in at $64.18 per share. Compared to the current share price, this implies the stock is 141.7% overvalued. The market price is significantly higher than what the model suggests is justified by future cash flows.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Lam Research may be overvalued by 141.7%. Discover 926 undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Lam Research Price vs Earnings

The Price-to-Earnings (PE) ratio is a widely used measure for valuing consistently profitable companies like Lam Research. It gives investors a way to assess how much they are paying today for each dollar of the company’s reported earnings. Companies with strong earnings growth and lower risk profiles typically command higher PE ratios. In contrast, slower growth or higher risk might justify a lower valuation.

Lam Research’s current PE ratio stands at 33.5x. In comparison, its peers average a slightly higher 37.1x and the broader semiconductor industry sits at around 35.8x. These comparisons provide some context, but do not account for all the nuances that could affect Lam’s fair value.

This is where Simply Wall St’s proprietary Fair Ratio comes in. By considering a combination of earnings growth, profit margins, the company’s size, risks, and its industry, the Fair Ratio offers a more holistic view than just comparing with peers or industry averages. For Lam Research, the Fair Ratio is calculated at 34.1x, almost exactly in line with the current multiple.

With the actual PE ratio just slightly below the Fair Ratio, Lam Research’s valuation on this metric looks entirely reasonable in today’s market.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1434 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Lam Research Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let’s introduce you to Narratives. Narratives are a simple yet powerful tool that let you connect your own view or “story” about a company with the actual numbers, such as your expected fair value, future revenue, earnings, and profit margins.

Instead of just crunching ratios, a Narrative helps you express why you believe a company’s future looks strong or risky, and links these views directly to a financial forecast and estimated fair value. On Simply Wall St’s Community page, millions of investors use Narratives to map out their investment case, compare their outlook with others, and decide if the stock fits their strategy.

Narratives are actionable—they let you track where the current Price sits versus your Fair Value, making it easier to spot buy and sell moments based on your outlook. As real-world news, earnings, or company developments occur, your Narrative can update dynamically, so your perspective always stays relevant.

For Lam Research, for example, some investors see strong long-term growth and set a bullish fair value of $135 per share, while others focus on risk and competitive pressure, setting their fair value as low as $80 per share. Your personal Narrative is both your forecast and your guide.

Do you think there's more to the story for Lam Research? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:LRCX

Lam Research

Designs, manufactures, markets, refurbishes, and services semiconductor processing equipment used in the fabrication of integrated circuits in the United States, China, Korea, Taiwan, Japan, Southeast Asia, and Europe.

Outstanding track record with flawless balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

75 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

44 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8147.4% undervalued

9 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

89 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

926 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative