Advertisement

- United States

- /

- Semiconductors

- /

- NasdaqGS:KLIC

Does Kulicke and Soffa Industries, Inc.'s (NASDAQ:KLIC) P/E Ratio Signal A Buying Opportunity?

Want to participate in a short research study? Help shape the future of investing tools and receive a $20 prize!

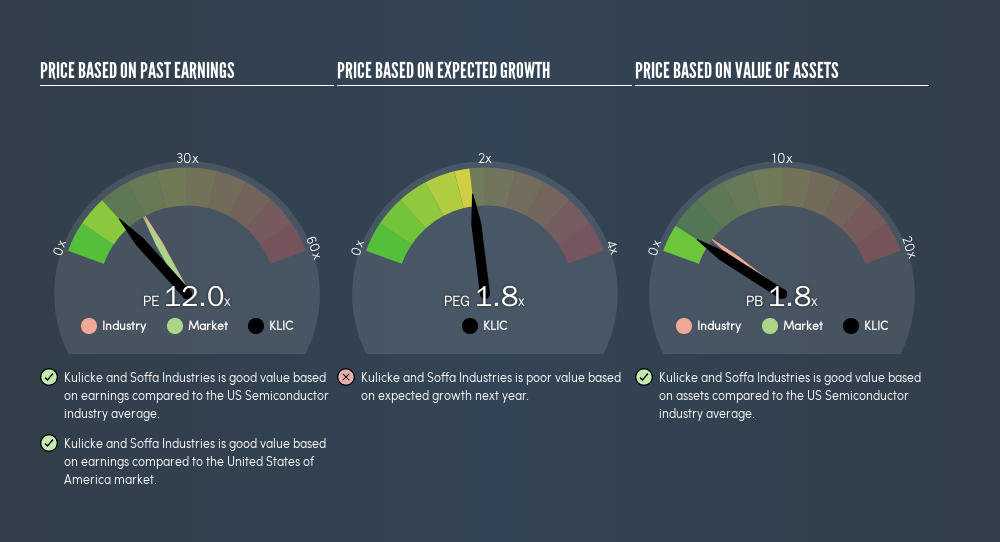

The goal of this article is to teach you how to use price to earnings ratios (P/E ratios). To keep it practical, we'll show how Kulicke and Soffa Industries, Inc.'s (NASDAQ:KLIC) P/E ratio could help you assess the value on offer. Kulicke and Soffa Industries has a P/E ratio of 11.97, based on the last twelve months. That corresponds to an earnings yield of approximately 8.4%.

Check out our latest analysis for Kulicke and Soffa Industries

How Do You Calculate A P/E Ratio?

The formula for price to earnings is:

Price to Earnings Ratio = Share Price ÷ Earnings per Share (EPS)

Or for Kulicke and Soffa Industries:

P/E of 11.97 = $23.35 ÷ $1.95 (Based on the trailing twelve months to December 2018.)

Is A High Price-to-Earnings Ratio Good?

A higher P/E ratio implies that investors pay a higher price for the earning power of the business. That is not a good or a bad thing per se, but a high P/E does imply buyers are optimistic about the future.

How Growth Rates Impact P/E Ratios

Probably the most important factor in determining what P/E a company trades on is the earnings growth. When earnings grow, the 'E' increases, over time. That means even if the current P/E is high, it will reduce over time if the share price stays flat. Then, a lower P/E should attract more buyers, pushing the share price up.

It's nice to see that Kulicke and Soffa Industries grew EPS by a stonking 244% in the last year. And earnings per share have improved by 11% annually, over the last five years. With that performance, I would expect it to have an above average P/E ratio.

How Does Kulicke and Soffa Industries's P/E Ratio Compare To Its Peers?

The P/E ratio essentially measures market expectations of a company. The image below shows that Kulicke and Soffa Industries has a lower P/E than the average (17.7) P/E for companies in the semiconductor industry.

This suggests that market participants think Kulicke and Soffa Industries will underperform other companies in its industry. Many investors like to buy stocks when the market is pessimistic about their prospects. If you consider the stock interesting, further research is recommended. For example, I often monitor director buying and selling.

Remember: P/E Ratios Don't Consider The Balance Sheet

It's important to note that the P/E ratio considers the market capitalization, not the enterprise value. In other words, it does not consider any debt or cash that the company may have on the balance sheet. Theoretically, a business can improve its earnings (and produce a lower P/E in the future), by taking on debt (or spending its remaining cash).

Such spending might be good or bad, overall, but the key point here is that you need to look at debt to understand the P/E ratio in context.

How Does Kulicke and Soffa Industries's Debt Impact Its P/E Ratio?

Since Kulicke and Soffa Industries holds net cash of US$617m, it can spend on growth, justifying a higher P/E ratio than otherwise.

The Verdict On Kulicke and Soffa Industries's P/E Ratio

Kulicke and Soffa Industries has a P/E of 12. That's below the average in the US market, which is 17.5. Not only should the net cash position reduce risk, but the recent growth has been impressive. The below average P/E ratio suggests that market participants don't believe the strong growth will continue.

Investors should be looking to buy stocks that the market is wrong about. If it is underestimating a company, investors can make money by buying and holding the shares until the market corrects itself. So this freevisual report on analyst forecasts could hold the key to an excellent investment decision.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this freelist of companies with modest (or no) debt, trading on a P/E below 20.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About NasdaqGS:KLIC

Kulicke and Soffa Industries

Engages in the design, manufacture, and sale of capital equipment and tools used to assemble semiconductor devices.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|4.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|32.5% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$384.84|21.9% undervalued

BL

Community Contributor