Advertisement

- United States

- /

- Semiconductors

- /

- NasdaqGS:INTC

Intel's (NASDAQ:INTC) Turnaround Story is Depending on Successful Expansions

After an underwhelming year, Intel Corporation (NASDAQ: INTC) has more optimistic plans for 2022. There will be plenty of catalysts between significant capital investments and a corporate spinoff.

However, the CEO expects the chip shortages to last until 2023 and the corporate turnaround to take 5 years.

Check out our latest analysis for Intel

Latest Developments

Intel's CEO, Pat Gelsinger, has been in the role for less than a year, but he has taken significant steps in the corporate turnaround, planning over US$100b of investments in new chip plants.

Among the ambitious plan is a US$9b worth investment in an advanced semiconductor packaging plant in Italy. The investment planned for 10 years should help the company get a stronger foothold in Europe. Other expansions include France (research and design) and Germany (likely the main fabrication plant). Furthermore, there will be a US$7b investment in Malaysia, where the company hopes to add 4,000 jobs in a new packaging and testing facility.

The ultimate goal is to avoid further semiconductor shortages, which Mr.Gelsinger assumes would last at least another year.

Yet, expansions are not cheap, and this is where Intel plans to bank on taking the Mobileye public. A US$15b investment in Mobileye has reached triple value, and it seems only to be growing as the company partnered up with the startup Udelv, whose transporter vehicle is designed to carry up to 2,000 lbs of goods with an autonomy between 160 and 300 miles.

Estimating the Intrinsic Value of Intel Corporation

Using the most recent financial data, we'll take a look at whether the stock is reasonably priced by taking the expected future cash flows and discounting them to today's value. The Discounted Cash Flow (DCF) model is the tool we will apply to do this.

We generally believe that a company's value is the present value of all cash it will generate in the future. However, a DCF is just one valuation metric among many, and it is not without flaws. If you still have some questions about this type of valuation, look at the Simply Wall St analysis model.

Step by step through the calculation

We use what is known as a 2-stage model, which means we have two different periods of growth rates for the company's cash flows. Generally, the first stage is higher growth, and the second stage is lower. In the first stage, we need to estimate the cash flows to the business over the next ten years. Where possible, we use analyst estimates, but when these aren't available, we extrapolate the previous free cash flow (FCF) from the last estimate or reported value.

We assume companies with shrinking free cash flow will slow their rate of shrinkage and that companies with growing free cash flow will see their growth rate slow over this period. We do this to reflect that growth tends to slow more in the early years than in later years.

Generally, we assume that a dollar today is more valuable than a dollar in the future, and so the sum of these future cash flows is then discounted to today's value:

10-year free cash flow (FCF) estimate

| 2022 | 2023 | 2024 | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | |

| Levered FCF ($, Millions) | US$6.11b | US$4.32b | US$15.6b | US$17.7b | US$19.2b | US$20.4b | US$21.5b | US$22.4b | US$23.2b | US$23.9b |

| Growth Rate Estimate Source | Analyst x10 | Analyst x7 | Analyst x1 | Analyst x2 | Est @ 8.5% | Est @ 6.54% | Est @ 5.16% | Est @ 4.2% | Est @ 3.53% | Est @ 3.06% |

| Present Value ($, Millions) Discounted @ 7.3% | US$5.7k | US$3.8k | US$12.6k | US$13.3k | US$13.5k | US$13.4k | US$13.1k | US$12.7k | US$12.3k | US$11.8k |

("Est" = FCF growth rate estimated by Simply Wall St)

Present Value of 10-year Cash Flow (PVCF) = US$112b

The second stage is also known as Terminal Value; this is the business's cash flow after the first stage. The Gordon Growth formula is used to calculate Terminal Value at a future annual growth rate equal to the 5-year average of the 10-year government bond yield of 2.0%. We discount the terminal cash flows to today's value at the cost of equity of 7.3%.

Terminal Value (TV)= FCF2031 × (1 + g) ÷ (r – g) = US$24b× (1 + 2.0%) ÷ (7.3%– 2.0%) = US$453b

Present Value of Terminal Value (PVTV)= TV / (1 + r)10= US$453b÷ ( 1 + 7.3%)10= US$223b

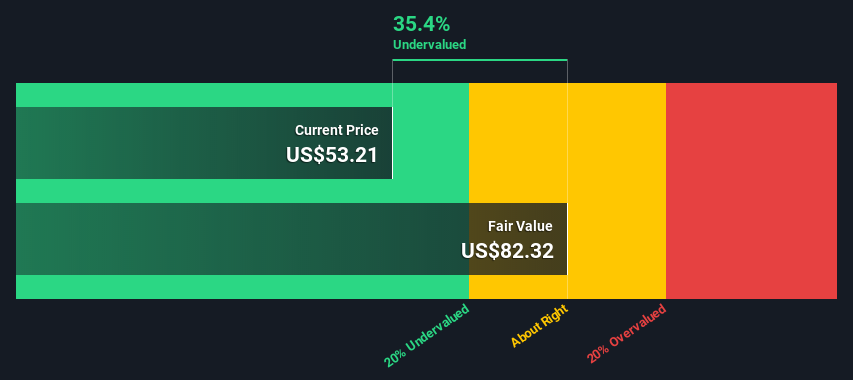

The total value is the sum of cash flows for the next ten years plus the discounted terminal value, which results in the Total Equity Value, which in this case is US$335b. To get the intrinsic value per share, we divide this by the total number of shares outstanding.

Compared to the current share price of US$53.2, the company appears quite good value at a 35% discount to where the stock price trades currently. Valuations are imprecise instruments though, do keep this in mind.

The assumptions

We would point out that the most important inputs to a discounted cash flow are the discount rate and, of course, the actual cash flows.

Furthermore, DCF does not consider the possible cyclicality of an industry or a company's future capital requirements, so it does not give a complete picture of its potential performance. Given that we are looking at Intel as potential shareholders, the cost of equity is used as the discount rate rather than the cost of capital (or the weighted average cost of capital, WACC), which accounts for debt. We've used 7.3% in this calculation, which is based on a levered beta of 1.230. Beta is a measure of a stock's volatility compared to the market as a whole.

Next Steps:

Intel seems to be undervalued at the moment, still keeping on the border of the single-digit price-to-earnings (P/E) ratio. However, much of the turnaround story depends on trust in its leadership. Although less than a year on the job, the new CEO is making big moves - using the firm's assets, thematic opportunities, and favorable government policies.

Yet, valuation is only one side of the coin in building your investment thesis, and it ideally won't be the only piece of analysis you scrutinize for a company. DCF models are not the be-all and end-all of investment valuation. For instance, if the terminal value growth rate is adjusted slightly, it can dramatically alter the overall result. What is the reason for the share price sitting below the intrinsic value?

For Intel, we've compiled three further factors you should further examine:

- Risks: As an example, we've found 1 warning sign for Intel that you need to consider before investing here.

- Future Earnings: How does INTC's growth rate compare to its peers and the broader market? Dig deeper into the analyst consensus number for the upcoming years by interacting with our free analyst growth expectation chart.

- Other High-Quality Alternatives: Do you like a good all-rounder? Explore our interactive list of high-quality stocks to get an idea of what else is out there you may be missing!

PS. The Simply Wall St app conducts a discounted cash flow valuation for every stock on the NASDAQGS every day. If you want to find the calculation for other stocks, just search here.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Stjepan Kalinic and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Stjepan Kalinic

Stjepan is a writer and an analyst covering equity markets. As a former multi-asset analyst, he prefers to look beyond the surface and uncover ideas that might not be on retail investors' radar. You can find his research all over the internet, including Simply Wall St News, Yahoo Finance, Benzinga, Vincent, and Barron's.

About NasdaqGS:INTC

Intel

Designs, develops, manufactures, markets, and sells computing and related products and services worldwide.

Fair value with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor