Advertisement

- United States

- /

- Semiconductors

- /

- NasdaqGM:ENPH

We Think Enphase Energy (NASDAQ:ENPH) Can Manage Its Debt With Ease

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Enphase Energy, Inc. (NASDAQ:ENPH) makes use of debt. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for Enphase Energy

How Much Debt Does Enphase Energy Carry?

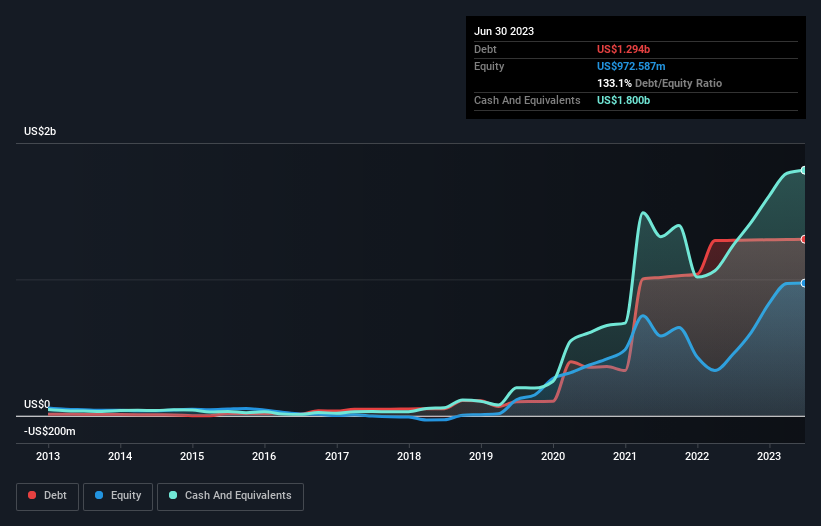

As you can see below, Enphase Energy had US$1.29b of debt, at June 2023, which is about the same as the year before. You can click the chart for greater detail. But on the other hand it also has US$1.80b in cash, leading to a US$506.0m net cash position.

How Healthy Is Enphase Energy's Balance Sheet?

According to the last reported balance sheet, Enphase Energy had liabilities of US$743.6m due within 12 months, and liabilities of US$1.75b due beyond 12 months. Offsetting this, it had US$1.80b in cash and US$558.4m in receivables that were due within 12 months. So its liabilities total US$134.4m more than the combination of its cash and short-term receivables.

Having regard to Enphase Energy's size, it seems that its liquid assets are well balanced with its total liabilities. So it's very unlikely that the US$16.3b company is short on cash, but still worth keeping an eye on the balance sheet. While it does have liabilities worth noting, Enphase Energy also has more cash than debt, so we're pretty confident it can manage its debt safely.

Even more impressive was the fact that Enphase Energy grew its EBIT by 149% over twelve months. That boost will make it even easier to pay down debt going forward. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Enphase Energy's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. While Enphase Energy has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Over the last three years, Enphase Energy actually produced more free cash flow than EBIT. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Summing Up

We could understand if investors are concerned about Enphase Energy's liabilities, but we can be reassured by the fact it has has net cash of US$506.0m. The cherry on top was that in converted 139% of that EBIT to free cash flow, bringing in US$865m. So is Enphase Energy's debt a risk? It doesn't seem so to us. Another factor that would give us confidence in Enphase Energy would be if insiders have been buying shares: if you're conscious of that signal too, you can find out instantly by clicking this link.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Valuation is complex, but we're here to simplify it.

Discover if Enphase Energy might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGM:ENPH

Enphase Energy

Designs, develops, manufactures, and sells home energy solutions for the solar photovoltaic industry in the United States and internationally.

Solid track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Defense AI: A Robotic Response to America’s Security Gaps

Fair Value US$12.00|49.7% undervalued

MA

Community Contributor

Figma (FIG): The S&P 500’s Design Standard Turning Into an All-in-One Platform

Fair Value US$65.70|7.0% overvalued

TI

Community Contributor

Sleep Cycle's Revenue Set to Rise 10% with Strong Revenue Model

Fair Value SEK 38.04|22.5% undervalued

MA

Community Contributor

Has JB Hi-Fi Lost Its Point of Difference?

Fair Value AU$76.00|52.5% overvalued

RO

Community Contributor