- United States

- /

- Pharma

- /

- NasdaqGM:HROW

Three US Growth Companies With High Insider Ownership

Reviewed by Simply Wall St

In the wake of the Federal Reserve's recent rate cut decision, major U.S. stock indexes have experienced a slight decline as investors digest the implications for future economic growth and inflation control. Amid this backdrop, identifying growth companies with high insider ownership can be particularly appealing to investors seeking stability and alignment of interests between company executives and shareholders. A good stock in today's market often combines robust growth potential with significant insider ownership, indicating confidence from those closest to the company's operations. Here are three U.S. growth companies that exemplify these qualities, offering promising prospects for long-term investment.

Top 10 Growth Companies With High Insider Ownership In The United States

| Name | Insider Ownership | Earnings Growth |

| Atour Lifestyle Holdings (NasdaqGS:ATAT) | 26% | 23.2% |

| GigaCloud Technology (NasdaqGM:GCT) | 25.7% | 24.3% |

| Victory Capital Holdings (NasdaqGS:VCTR) | 10.2% | 32.3% |

| Atlas Energy Solutions (NYSE:AESI) | 29.1% | 42.1% |

| Super Micro Computer (NasdaqGS:SMCI) | 25.7% | 28.0% |

| Hims & Hers Health (NYSE:HIMS) | 13.7% | 40.7% |

| Credo Technology Group Holding (NasdaqGS:CRDO) | 14.1% | 95% |

| EHang Holdings (NasdaqGM:EH) | 32.8% | 81.5% |

| BBB Foods (NYSE:TBBB) | 22.9% | 51.2% |

| Carlyle Group (NasdaqGS:CG) | 29.5% | 22% |

Let's uncover some gems from our specialized screener.

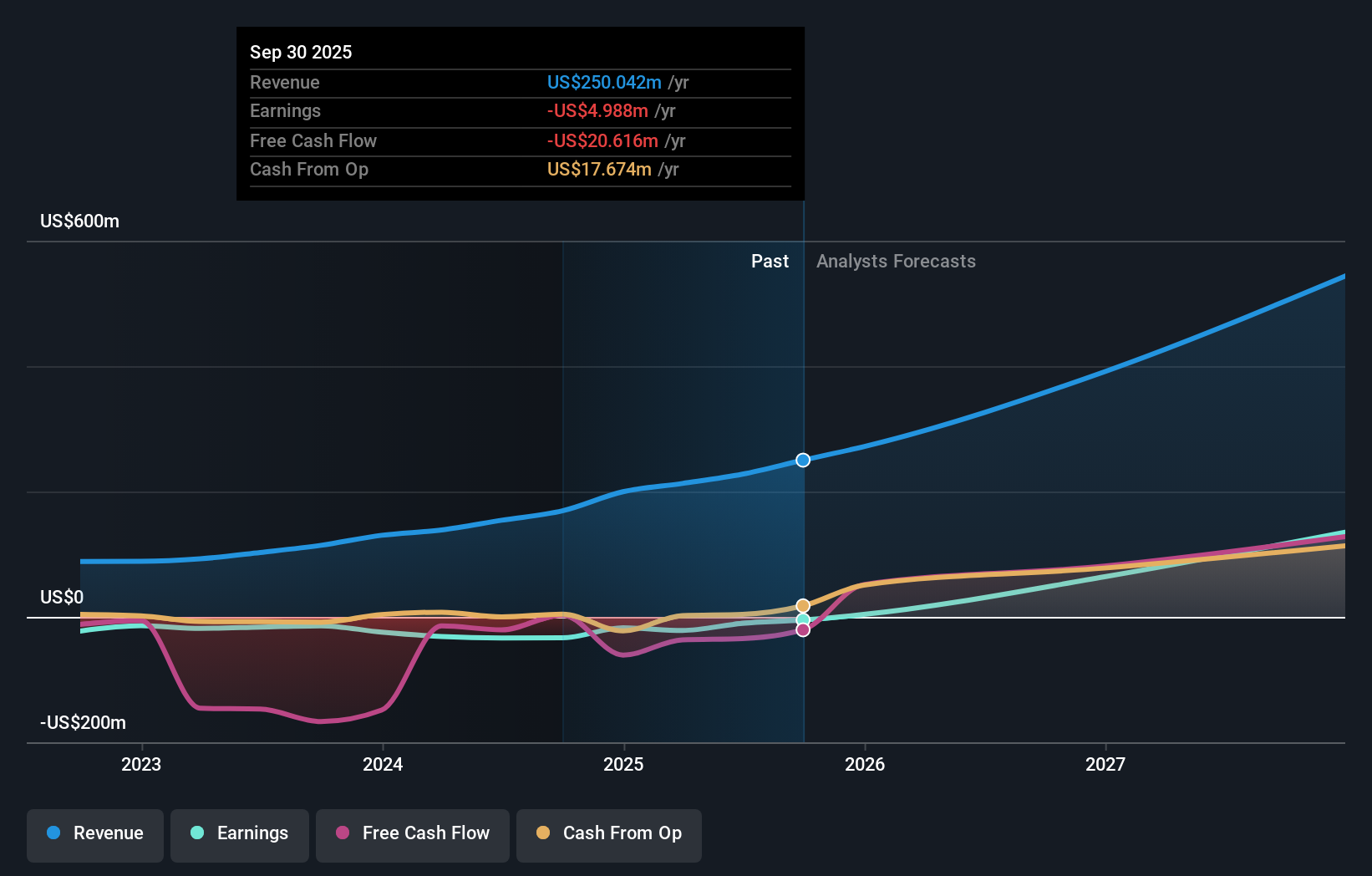

Harrow (NasdaqGM:HROW)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Harrow, Inc., an eyecare pharmaceutical company focused on the discovery, development, and commercialization of ophthalmic products, has a market cap of $1.55 billion.

Operations: Harrow's revenue is primarily derived from the discovery, development, and commercialization of innovative ophthalmic therapies, totaling $154.15 million.

Insider Ownership: 14.3%

Harrow's earnings are forecast to grow 78.4% annually, with revenue expected to increase 33.3% per year, outpacing the US market. Despite trading at 73.9% below its fair value estimate, Harrow remains highly volatile and reported a net loss of US$6.47 million for Q2 2024. Recent presentations at major conferences and new product agreements highlight ongoing efforts to expand its footprint in the healthcare sector.

- Click here to discover the nuances of Harrow with our detailed analytical future growth report.

- According our valuation report, there's an indication that Harrow's share price might be on the cheaper side.

Astera Labs (NasdaqGS:ALAB)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Astera Labs, Inc. designs, manufactures, and sells semiconductor-based connectivity solutions for cloud and AI infrastructure with a market cap of $7.26 billion.

Operations: Astera Labs generates $229.55 million in revenue from its semiconductor-based connectivity solutions for cloud and AI infrastructure.

Insider Ownership: 18.1%

Astera Labs' revenue surged to US$76.85 million in Q2 2024 from US$10.69 million a year ago, while net loss narrowed significantly. The company forecasts revenue between US$95 million and US$100 million for Q3 2024. Despite high volatility, Astera Labs is trading at 30.9% below its fair value estimate and expects to become profitable within three years, with insiders buying more shares recently than selling, indicating confidence in its growth trajectory.

- Click here and access our complete growth analysis report to understand the dynamics of Astera Labs.

- The valuation report we've compiled suggests that Astera Labs' current price could be inflated.

Ibotta (NYSE:IBTA)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Ibotta, Inc. (NYSE: IBTA) is a technology company that provides the Ibotta Performance Network (IPN), enabling consumer packaged goods brands to deliver digital promotions to consumers, with a market cap of $1.85 billion.

Operations: The company's revenue segment is primarily derived from Internet Software, generating $355.21 million.

Insider Ownership: 18.8%

Ibotta's earnings are projected to grow 68.4% annually over the next three years, significantly outpacing the US market. Despite a recent net loss of US$33.97 million in Q2 2024, revenue increased to US$87.93 million from US$77.39 million year-over-year. The company announced a share repurchase program worth up to US$100 million and formed a strategic partnership with Instacart, enhancing its growth potential and market reach through digital coupons integration.

- Unlock comprehensive insights into our analysis of Ibotta stock in this growth report.

- Upon reviewing our latest valuation report, Ibotta's share price might be too pessimistic.

Summing It All Up

- Embark on your investment journey to our 178 Fast Growing US Companies With High Insider Ownership selection here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Harrow might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGM:HROW

Harrow

An eyecare pharmaceutical company, engages in the discovery, development, and commercialization of ophthalmic pharmaceutical products.

High growth potential and fair value.