Advertisement

- United States

- /

- Specialty Stores

- /

- NYSE:WRBY

Is Warby Parker's Shift to Profitability and Higher Sales Guidance Changing the WRBY Investment Case?

Simply Wall St

Reviewed by Sasha Jovanovic

- Warby Parker reported third quarter 2025 earnings, showing US$221.68 million in sales and a move to US$5.87 million net income from a net loss a year earlier, with basic and diluted earnings per share rising to US$0.05.

- The company also raised its full-year 2025 net revenue outlook to US$871 million–US$874 million, citing strong business momentum and approximately 13% projected revenue growth.

- We'll explore how Warby Parker's shift to profitability and increased revenue guidance influences its investment case going forward.

We've found 16 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Warby Parker Investment Narrative Recap

To invest in Warby Parker, you need to believe in its ability to sustainably grow revenue and profits by standing out in a crowded eyewear market. The company’s move into profitability and raised revenue guidance is encouraging for the near-term growth catalyst of expanding its customer base and store footprint; however, the risk of slower e-commerce momentum as digital competition mounts still looms, and the latest earnings do not materially change that risk factor for now.

Among recent announcements, the partnership with Google for AI-powered eyewear remains the most relevant catalyst in context of this earnings news, offering the possibility of creating a fresh revenue stream with higher margins. This initiative fits neatly with Warby Parker’s push for innovation, but as with many early-stage ventures, execution risk remains high for non-core products.

In contrast, the risk of increased fixed costs from rapid retail expansion is something investors should be mindful of if store performance...

Read the full narrative on Warby Parker (it's free!)

Warby Parker's outlook anticipates $1.2 billion in revenue and $85.4 million in earnings by 2028. This scenario implies a 14.8% annual revenue growth rate and an increase in earnings of $94.6 million from the current level of -$9.2 million.

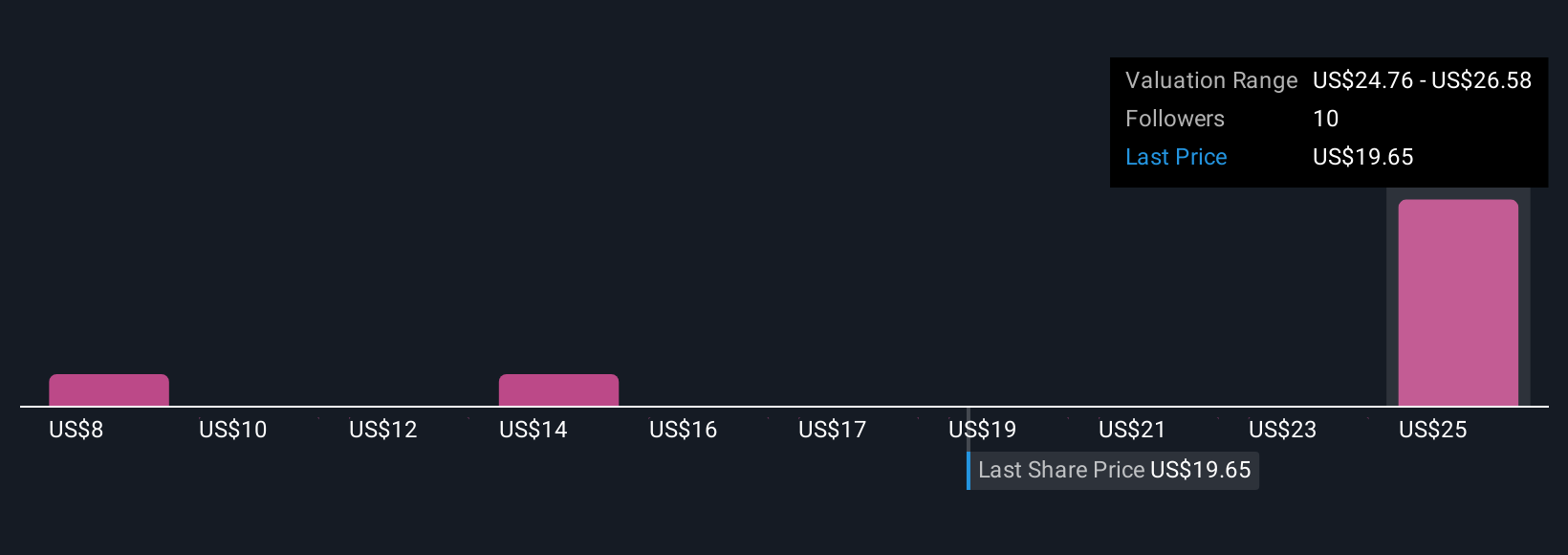

Uncover how Warby Parker's forecasts yield a $25.08 fair value, a 48% upside to its current price.

Exploring Other Perspectives

Five members of the Simply Wall St Community produced fair value estimates for Warby Parker ranging from US$8.37 to US$25.60 per share. Some investors point to the risk that increased digital competition could persistently pressure sales growth, raising questions about how sustainable current momentum truly is if online trends falter.

Explore 5 other fair value estimates on Warby Parker - why the stock might be worth less than half the current price!

Build Your Own Warby Parker Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Warby Parker research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Warby Parker research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Warby Parker's overall financial health at a glance.

Ready For A Different Approach?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 37 best rare earth metal stocks of the very few that mine this essential strategic resource.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- AI is about to change healthcare. These 32 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Warby Parker might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:WRBY

Flawless balance sheet with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor