Advertisement

- United States

- /

- Specialty Stores

- /

- NYSE:BOOT

Does Boot Barn’s 41% Rally Signal Room for Growth or Caution in 2025?

Simply Wall St

Reviewed by Bailey Pemberton

- Ever wondered if Boot Barn Holdings is trading at a bargain, fully valued, or potentially overhyped? You're not alone. Many investors are asking the same question as the stock grabs attention on Wall Street.

- Shares have climbed 41.3% over the past year and show a 27.0% year-to-date gain. There have been some recent short-term swings, with a 5.4% rise in the last week and only a slight -0.2% dip over the past month.

- This momentum follows sector-wide optimism and reports of resilient consumer spending, which are keeping retailers like Boot Barn in the spotlight. Investors are also focused on the company's expansion plans and continued presence in specialty retail headlines.

- Despite the run-up and increased news coverage, Boot Barn currently scores 0 out of 6 on our valuation checks. This suggests caution may be warranted. Let's review the key valuation approaches, and later, we will explore an additional method for assessing whether Boot Barn is a suitable investment.

Boot Barn Holdings scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Boot Barn Holdings Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company's intrinsic value by projecting its expected future cash flows and discounting them back to today's dollars. This approach helps investors judge whether a stock's current price reflects its long-term earning potential or not.

For Boot Barn Holdings, the DCF analysis relies on two stages of projected free cash flow to equity. The company reported a latest trailing twelve months Free Cash Flow of $58.2 million. Analysts provide detailed estimates for the next several years, with free cash flow forecasted to nearly double to $119.1 million in 2026 and rise modestly to $125.5 million in 2027. After this period, projections involve modest declines and stabilization through extrapolation, with a 10-year forecast landing at $21.9 million by 2035.

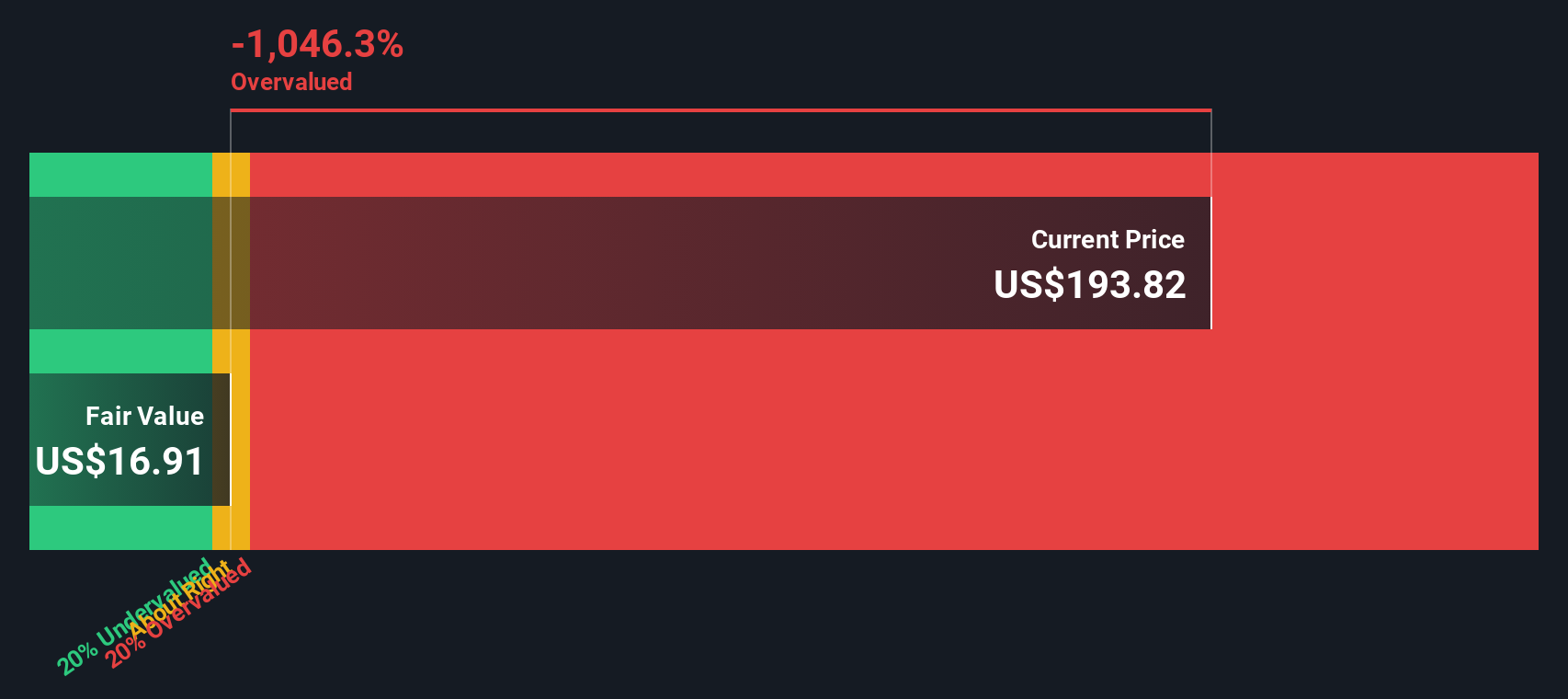

After discounting all future cash flows to present value, the resulting estimated intrinsic value per share is $16.93. With the stock trading far above this estimate, the model implies Boot Barn Holdings is 1,044.5% overvalued on a discounted cash flow basis.

This suggests that even with solid projected cash flows, the current share price far exceeds what the numbers support. Investors should exercise caution if relying only on DCF-driven valuations for this stock.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Boot Barn Holdings may be overvalued by 1044.5%. Discover 920 undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Boot Barn Holdings Price vs Earnings (PE)

The Price-to-Earnings ratio, or PE, is often the preferred multiple for valuing profitable companies like Boot Barn Holdings. This metric takes into account the company’s net earnings, making it especially useful for assessing how much investors are willing to pay for current profits. Growth expectations and risk also play a major role here. Companies with stronger growth prospects and lower perceived risk typically command higher PE ratios, while those facing uncertainty or slower growth tend to trade at lower multiples.

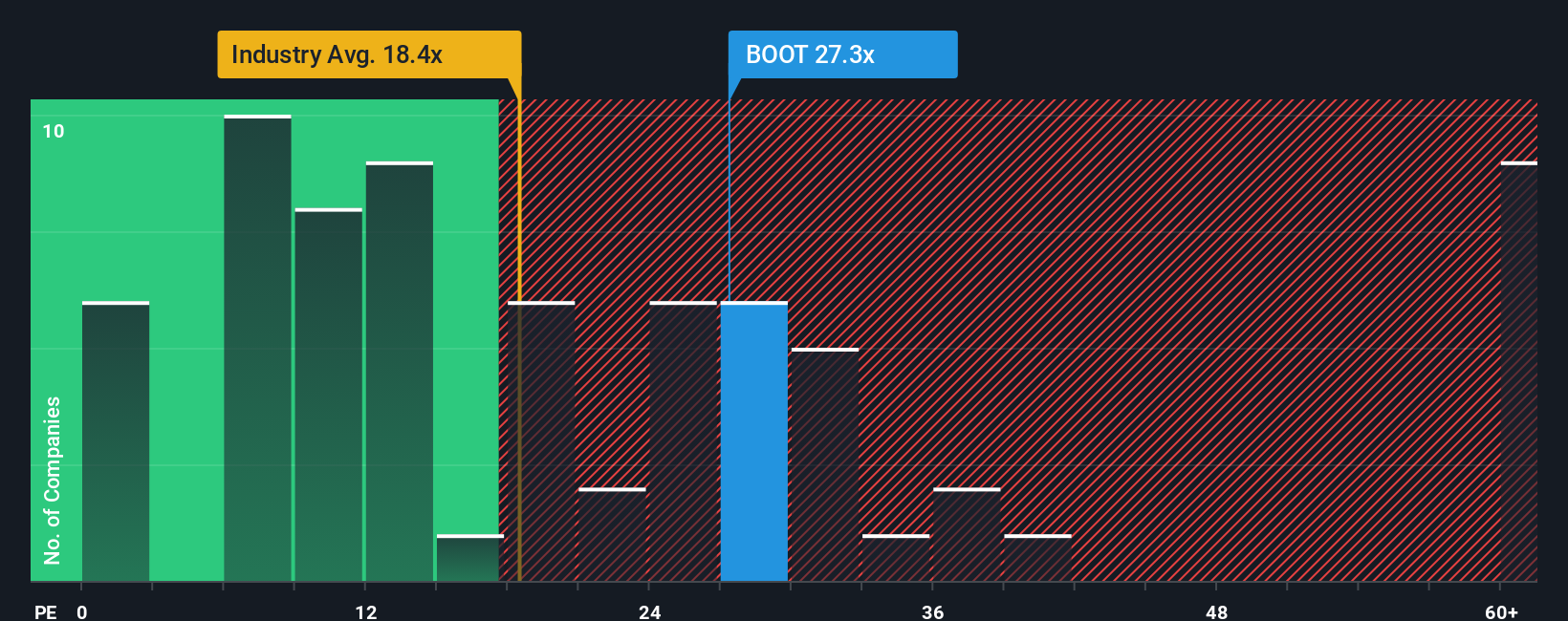

Boot Barn Holdings is currently trading at a PE ratio of 28.4x. To put that in perspective, the specialty retail industry average stands at 18.0x, and the peer group average is 12.9x. Boot Barn’s stock is priced at a significant premium when compared to both its direct competitors and the wider industry. However, relying only on these benchmarks can be misleading if a company’s specific strengths or risks differ from its peers.

This is where Simply Wall St’s “Fair Ratio” comes in. The Fair Ratio is a proprietary metric that estimates a stock’s justified PE multiple, factoring in things like earnings growth, profit margins, market cap, risk profile, and industry dynamics. For Boot Barn, the calculated Fair Ratio is 18.6x. Because it accounts for more than just surface comparisons, the Fair Ratio is a more holistic and balanced way to judge valuation.

Comparing Boot Barn Holdings’ current PE of 28.4x to its Fair Ratio of 18.6x, the stock is trading well above the level justified by its fundamentals and outlook. This points to the stock being overvalued on a price-to-earnings basis at present.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1443 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Boot Barn Holdings Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is your personal investment story; it is the perspective you take on a company based on what you believe about its future growth, risks, and unique strengths or challenges. Narratives connect your view of Boot Barn Holdings’ business drivers directly to your own forecasts for revenue, earnings, and margins, and then translate those beliefs into a fair value estimate for the stock.

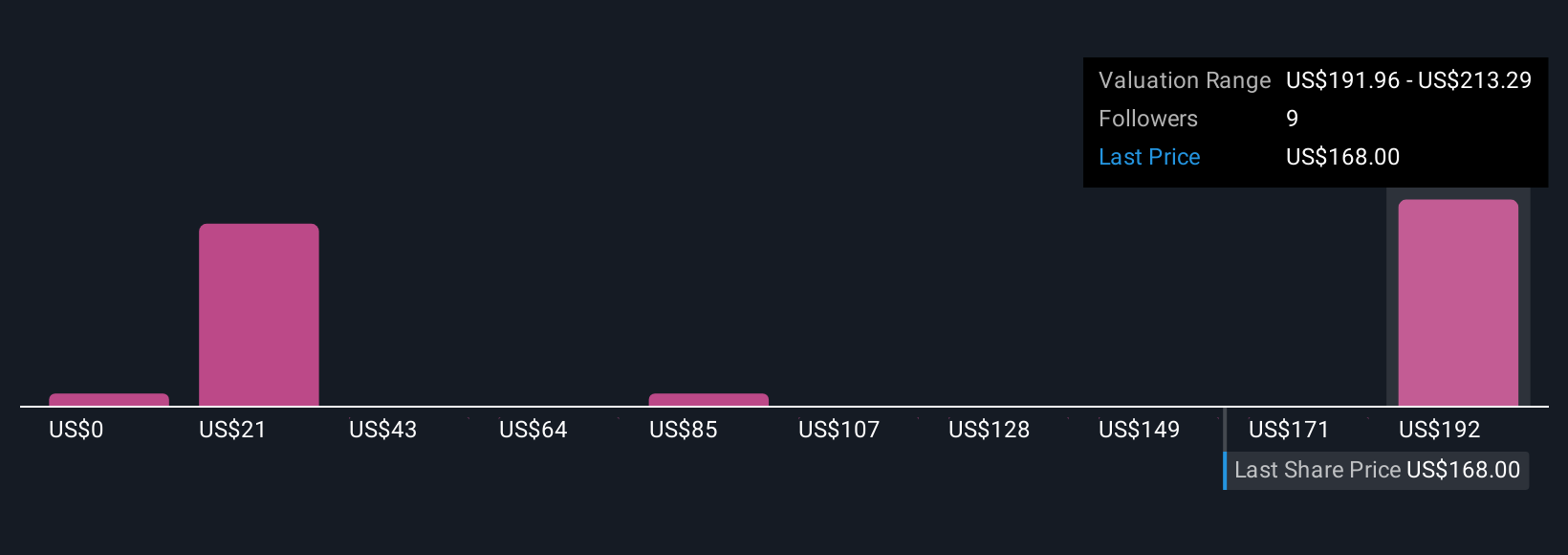

This approach is more powerful because it turns the numbers into a living story that updates as new information emerges, such as news or earnings releases, giving you a dynamic and clear view of whether to buy, hold, or sell. Narratives are accessible to everyone on Simply Wall St’s Community page, where millions of investors are already sharing and refining perspectives. By comparing your Narrative’s fair value with the current share price, you get a simple, actionable signal; if your outlook matches the highest current analyst target for Boot Barn ($254.0), you might see meaningful upside, while the lowest target ($142.0) may signal caution, showing just how much opinions can differ depending on each investor’s story and assumptions.

Do you think there's more to the story for Boot Barn Holdings? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Boot Barn Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:BOOT

Boot Barn Holdings

Operates specialty retail stores in the United States and internationally.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SW

swift11 on DXC Technology ·

CEO: We are winners in the long term in the AI world

Fair Value:US$17.4624.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7924.0% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative