Advertisement

- United States

- /

- Specialty Stores

- /

- NYSE:BBY

Best Buy (BBY) Is Up 7.1% After Raising 2026 Revenue Guidance and Maintaining Dividend

Simply Wall St

Reviewed by Sasha Jovanovic

- Best Buy Co., Inc. recently reported its third-quarter results with sales of US$9.67 billion, raised its fiscal 2026 revenue guidance to a range of US$41.65 billion to US$41.95 billion, and announced a US$0.95 regular quarterly dividend payable in January 2026.

- An interesting detail is that, although year-over-year net income fell to US$140 million due in part to a US$171 million impairment, the company improved its outlook for comparable sales and share buybacks.

- We'll assess how Best Buy’s raised full-year revenue and sales guidance could influence expectations for future marketplace growth and profitability.

Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

Best Buy Investment Narrative Recap

To be a shareholder in Best Buy, you need confidence in the company's ability to drive revenue through consumer technology upgrade cycles and capitalize on high-margin service offerings, while effectively managing online competition and shifting industry demand. The recent news of raised revenue guidance and ongoing share buybacks reinforces management's optimism, but the most pressing short-term catalyst remains execution on growth from emerging marketplace and services; the biggest risk continues to be margin pressure from sales mix and intense competition, with recent results having only a modest effect on these themes.

Among recent announcements, Best Buy's updated fiscal 2026 revenue outlook stands out: the company now expects US$41.65 to US$41.95 billion, an increase from prior guidance. This update closely ties to the near-term catalyst of marketplace expansion and service-driven growth, signaling management’s view that demand and competitive positioning are trending in the right direction.

Yet, in contrast to these positive signals, investors should be aware of rising competitive pressure and changes in sales mix that could...

Read the full narrative on Best Buy (it's free!)

Best Buy's outlook anticipates $44.5 billion in revenue and $1.5 billion in earnings by 2028. This is based on a projected 2.3% annual revenue growth rate and nearly doubling of earnings, up $722 million from the current $778 million.

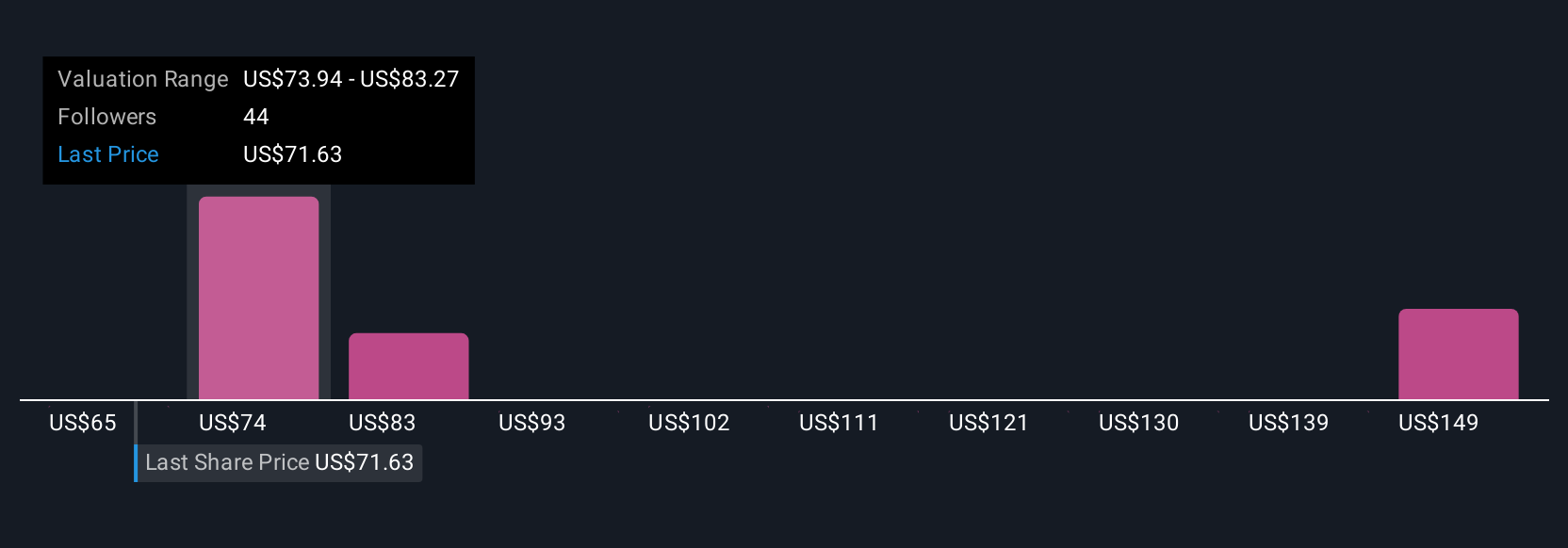

Uncover how Best Buy's forecasts yield a $81.38 fair value, in line with its current price.

Exploring Other Perspectives

Fair value estimates from six members of the Simply Wall St Community range from US$64.62 to US$176.66 per share. With ongoing risks from shrinking gross profit rates and competitive threats to both online and in-store channels, your outlook on Best Buy’s recovery could differ widely from other market participants.

Explore 6 other fair value estimates on Best Buy - why the stock might be worth 19% less than the current price!

Build Your Own Best Buy Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Best Buy research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Best Buy research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Best Buy's overall financial health at a glance.

No Opportunity In Best Buy?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- We've found 14 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 26 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Best Buy might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:BBY

Best Buy

Offers technology products and solutions in the United States, Canada, and internationally.

Flawless balance sheet established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

75 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

44 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8147.4% undervalued

9 followersusers have followed this narrative

2 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

89 followersusers have followed this narrative

11 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

926 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative