Advertisement

- United States

- /

- Specialty Stores

- /

- NYSE:BBWI

The Bull Case For Bath & Body Works (BBWI) Could Change Following Surging Loyalty Sales and CEO Shift—Learn Why

Simply Wall St

Reviewed by Sasha Jovanovic

- Recently, Bath & Body Works announced that its loyalty program now accounts for 80% of annual sales, and the company appointed a new CEO with a focus on digital transformation to drive growth in both online and in-store channels.

- Management has aggressively reduced debt and the number of shares outstanding using free cash flow, while guiding for modest sales growth and large share repurchases under its new leadership.

- We will now explore how these operational improvements and the emphasis on customer loyalty may strengthen Bath & Body Works’ investment outlook.

The latest GPUs need a type of rare earth metal called Neodymium and there are only 37 companies in the world exploring or producing it. Find the list for free.

Bath & Body Works Investment Narrative Recap

To own shares in Bath & Body Works right now, an investor needs to believe that the company can reignite both revenue and earnings growth by converting strong loyalty engagement into broader customer acquisition, despite recent underperformance in digital sales and softening profit margins. The latest news on management’s renewed digital focus and share buybacks does not substantially change the near-term catalysts or alter the main risk, which remains the business’s challenge to attract new, especially younger, shoppers for sustainable growth.

Of the company's latest moves, the acceleration of digital transformation with a new CEO stands out, particularly given ongoing competitive pressures online and management’s own admission that digital sales have lagged expectations. If improvements to the omnichannel experience and innovations in customer engagement succeed, they could offset some risks, but the ultimate impact will rely on measurable progress in winning new customers and regaining digital momentum.

By contrast, the real concern for investors lies in Bath & Body Works’ continued struggle to expand its customer base, especially as...

Read the full narrative on Bath & Body Works (it's free!)

Bath & Body Works' narrative projects $8.1 billion revenue and $860.7 million earnings by 2028. This requires 3.1% yearly revenue growth and a $132.7 million earnings increase from $728.0 million currently.

Uncover how Bath & Body Works' forecasts yield a $38.83 fair value, a 44% upside to its current price.

Exploring Other Perspectives

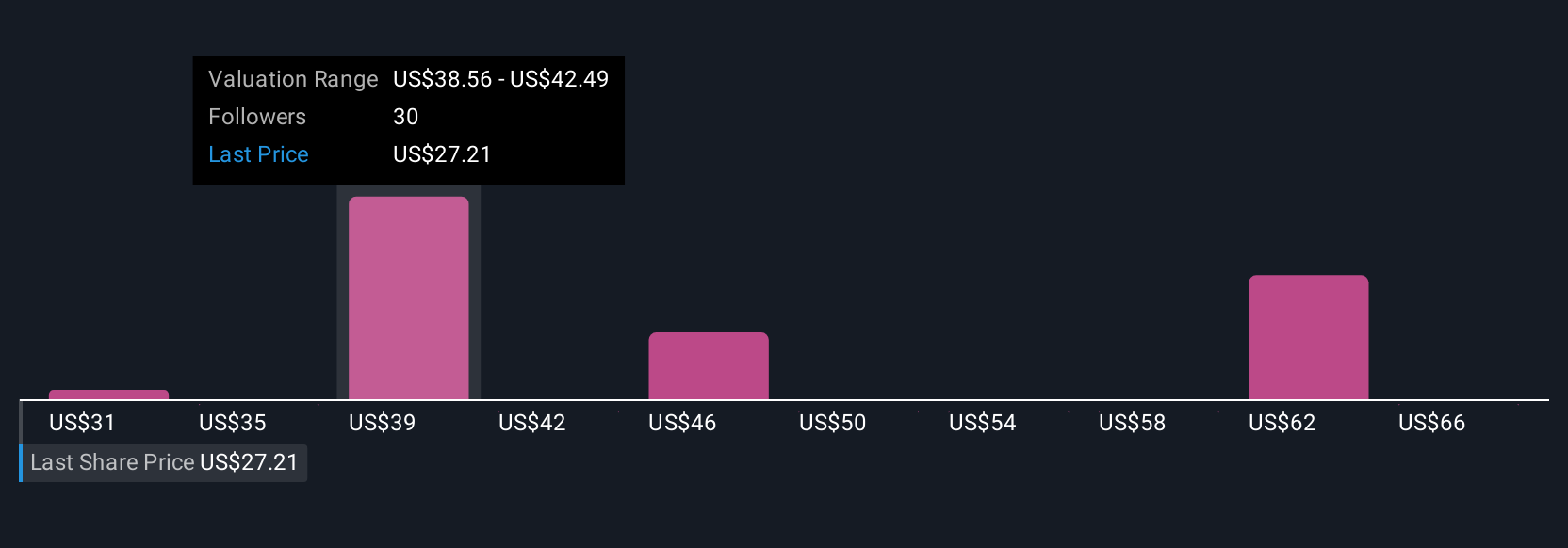

Simply Wall St Community members put Bath & Body Works’ fair value between US$30.70 and US$64.56, with 9 different appraisals spanned across this range. While many see value, the company’s slow customer growth and pressured digital sales may affect future returns, check out more opinions and analysis for a wider view.

Explore 9 other fair value estimates on Bath & Body Works - why the stock might be worth just $30.70!

Build Your Own Bath & Body Works Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Bath & Body Works research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Bath & Body Works research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Bath & Body Works' overall financial health at a glance.

Looking For Alternative Opportunities?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- These 15 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Bath & Body Works might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:BBWI

Bath & Body Works

Operates as a specialty retailer of home fragrance, personal and body care, soaps, and sanitizer products.

Undervalued second-rate dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.4% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|92.1% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|24.2% undervalued

GM

Community Contributor