Brett Heffes has been the CEO of Winmark Corporation (NASDAQ:WINA) since 2016, and this article will examine the executive's compensation with respect to the overall performance of the company. This analysis will also assess whether Winmark pays its CEO appropriately, considering recent earnings growth and total shareholder returns.

Check out our latest analysis for Winmark

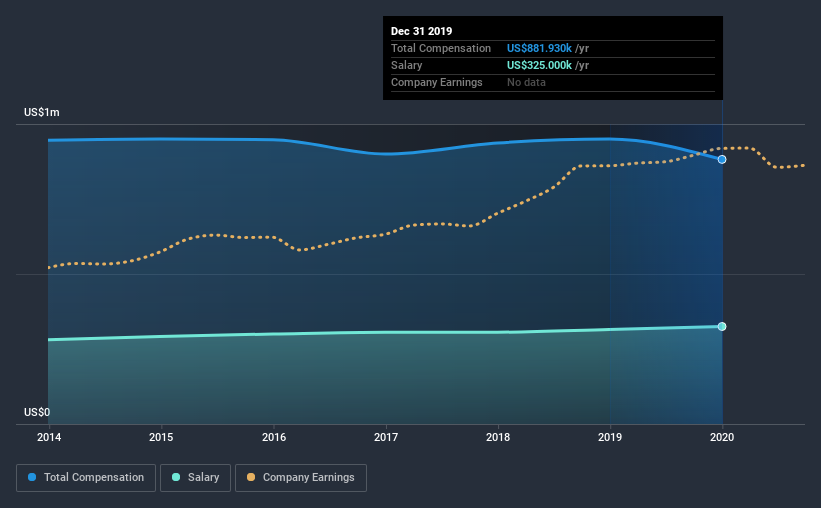

Comparing Winmark Corporation's CEO Compensation With the industry

At the time of writing, our data shows that Winmark Corporation has a market capitalization of US$696m, and reported total annual CEO compensation of US$882k for the year to December 2019. That's a slight decrease of 7.1% on the prior year. While this analysis focuses on total compensation, it's worth acknowledging that the salary portion is lower, valued at US$325k.

For comparison, other companies in the same industry with market capitalizations ranging between US$400m and US$1.6b had a median total CEO compensation of US$2.6m. This suggests that Brett Heffes is paid below the industry median. Moreover, Brett Heffes also holds US$20m worth of Winmark stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

| Component | 2019 | 2018 | Proportion (2019) |

| Salary | US$325k | US$315k | 37% |

| Other | US$557k | US$635k | 63% |

| Total Compensation | US$882k | US$950k | 100% |

Talking in terms of the industry, salary represented approximately 20% of total compensation out of all the companies we analyzed, while other remuneration made up 80% of the pie. Winmark is paying a higher share of its remuneration through a salary in comparison to the overall industry. If total compensation is slanted towards non-salary benefits, it indicates that CEO pay is linked to company performance.

A Look at Winmark Corporation's Growth Numbers

Over the past three years, Winmark Corporation has seen its earnings per share (EPS) grow by 13% per year. Its revenue is down 7.4% over the previous year.

This demonstrates that the company has been improving recently and is good news for the shareholders. While it would be good to see revenue growth, profits matter more in the end. Although we don't have analyst forecasts, you might want to assess this data-rich visualization of earnings, revenue and cash flow.

Has Winmark Corporation Been A Good Investment?

We think that the total shareholder return of 47%, over three years, would leave most Winmark Corporation shareholders smiling. As a result, some may believe the CEO should be paid more than is normal for companies of similar size.

To Conclude...

As we noted earlier, Winmark pays its CEO lower than the norm for similar-sized companies belonging to the same industry. Since EPS growth is heading in a positive direction; many would agree with our assessment that the pay is modest. Plus, we can't ignore the impressive shareholder returns, and won't be surprised if some shareholders were to reward such excellent all-around performance with a raise.

CEO compensation is a crucial aspect to keep your eyes on but investors also need to keep their eyes open for other issues related to business performance. We've identified 2 warning signs for Winmark that investors should be aware of in a dynamic business environment.

Switching gears from Winmark, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

If you decide to trade Winmark, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Winmark might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NasdaqGM:WINA

Winmark

A resale company operates as a franchisor for small business in the United States and Canada.

Slight with acceptable track record.