Advertisement

- United States

- /

- Specialty Stores

- /

- NasdaqGS:TSCO

Tractor Supply (TSCO) Valuation in Focus After Jefferies Upgrade Highlights Growth Potential

Simply Wall St

Reviewed by Simply Wall St

Tractor Supply (TSCO) got a boost after Jefferies upgraded its rating, highlighting the company’s solid value, competitive pricing, and advantage from sourcing primarily within the U.S. Investors are watching how these strengths might influence stock performance in the future.

See our latest analysis for Tractor Supply.

Tractor Supply’s shares have rebounded modestly on the heels of Jefferies’ upgrade, with a 3.5% gain this week reflecting renewed optimism. While the stock’s year-to-date share price return sits at a healthy 4.6%, its total return over the past year remains slightly negative, but longer-term total shareholder returns have been notably strong: up more than 28% over three years and 121% over five. Momentum appears to be regaining some strength after a tough patch, especially as the company’s operational advantages come into sharper focus.

If Tractor Supply’s story has you curious about what else is picking up speed, now’s the perfect time to discover fast growing stocks with high insider ownership

With shares rebounding and analysts optimistic, the big question for investors is whether Tractor Supply’s current price reflects its long-term growth potential, or if the recent dip offers a compelling buying opportunity before the market catches up.

Most Popular Narrative: 13.8% Undervalued

Tractor Supply’s current share price sits well below the most popular narrative's fair value estimate, setting the stage for big upside according to analyst consensus. This wide gap puts the spotlight on the assumptions that drive this bullish appraisal.

Tractor Supply's strategy to reduce reliance on Chinese imports and diversify its supply chain, from over 90% to closer to 50% by year-end, could mitigate tariff impacts, potentially improving net margins and earnings. Strong transaction growth, unit growth in consumable, usable, and edible categories, and record customer retention indicate sustained demand, likely bolstering future revenue.

What’s fueling those higher expectations? Discover the bold profit margin targets and aggressive revenue growth projections that underpin this price tag. The math behind this narrative could surprise you. See what’s convincing analysts the upside is real.

Result: Fair Value of $63.52 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, ongoing declines in store sales or a more challenging economic backdrop could quickly temper optimism around Tractor Supply’s growth outlook.

Find out about the key risks to this Tractor Supply narrative.

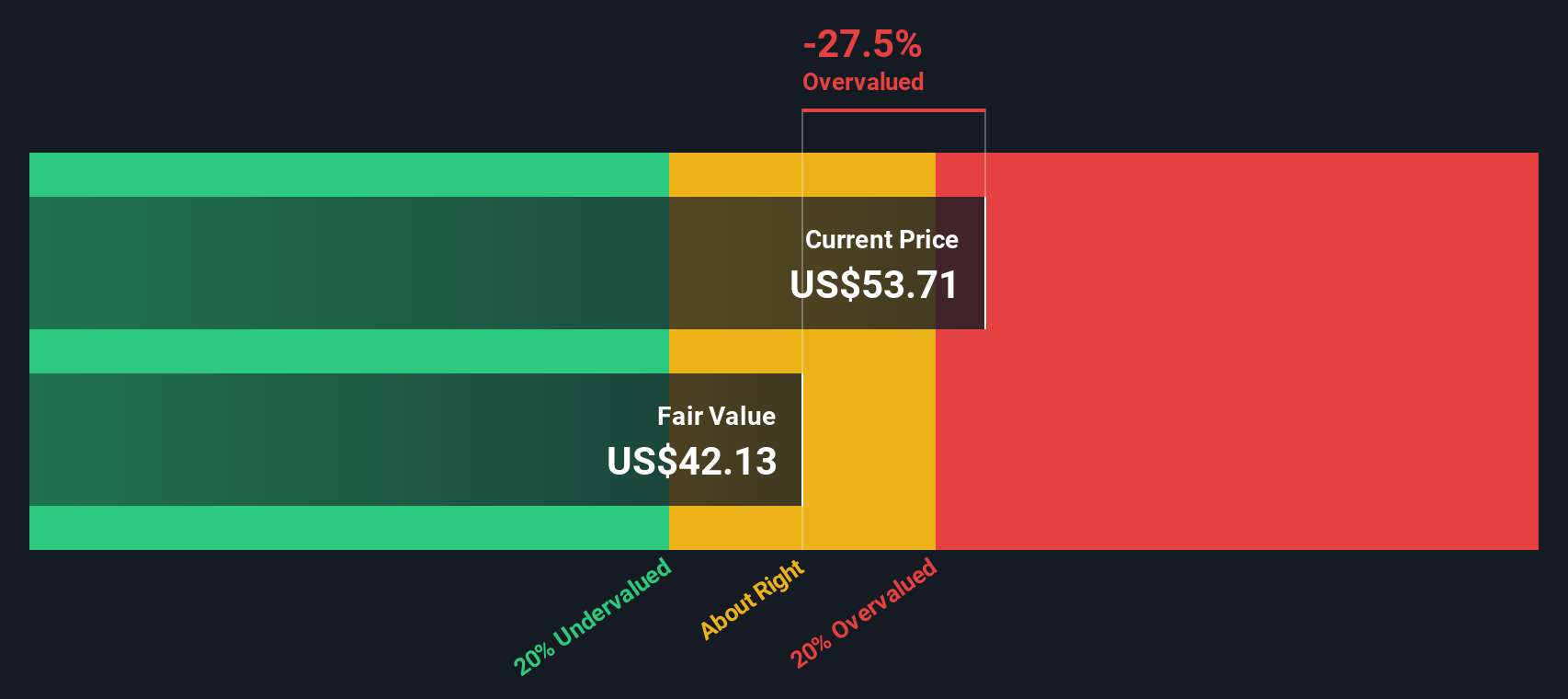

Another View: Testing the Numbers with the SWS DCF Model

While analysts see opportunity based on future earnings multiples, our SWS DCF model presents a more conservative perspective. According to this cash flow-based approach, Tractor Supply currently trades above its estimated fair value, which raises questions about how much future growth is already reflected in the price. Is optimism running ahead of fundamentals, or is there still room for upside?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Tractor Supply for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 914 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Tractor Supply Narrative

Not sold on the consensus or want to dive into the numbers yourself? You can craft your own narrative in just a few minutes. Do it your way

A great starting point for your Tractor Supply research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Stop waiting for the perfect stock. Take charge of your investing strategy by seizing opportunities you might be overlooking right now with these handpicked ideas.

- Capture rapid growth potential with these 25 AI penny stocks as artificial intelligence reshapes companies and industries from the inside out.

- Target impressive returns that outperform traditional savings by checking out these 15 dividend stocks with yields > 3% with yields above 3%.

- Seize untapped opportunities in digital finance by researching these 81 cryptocurrency and blockchain stocks pushing the boundaries of blockchain and cryptocurrency innovation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Tractor Supply might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:TSCO

Tractor Supply

Operates as a rural lifestyle retailer in the United States.

Established dividend payer with acceptable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CE

cementafriend on Constellation Energy ·

Constellation Energy Dividends and Growth

Fair Value:US$348.054.7% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KH

Khagani on CoreWeave ·

CoreWeave's Revenue Expected to Rocket 77.88% in 5-Year Forecast

Fair Value:US$11033.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PO

PortfolioPlus on Bisalloy Steel Group ·

Bisalloy Steel Group will shine with a projected profit margin increase of 12.8%

Fair Value:AU$6.7118.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

935 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

140 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative