Advertisement

- United States

- /

- Retail Distributors

- /

- NasdaqGS:POOL

Pool (POOL) Draws Earnings Optimism, Is It Still 21% Undervalued?

Analyst Optimism Builds Ahead of Pool Corp Earnings

Recent optimism around Pool (POOL) centers on its upcoming June-quarter earnings report, with expectations for higher revenue and a year over year EPS increase drawing fresh attention to the stock.

See our latest analysis for Pool.

Despite the upbeat earnings expectations, Pool's recent share price performance has been weak, with the stock closing at US$201.17 and the 1 year total shareholder return down 31.18%, which points to fading momentum as investors reassess both growth prospects and risks.

If this earnings story has you reviewing your watchlist, it can be a good moment to widen your search and uncover 18 top founder-led companies

Pool shares have already retreated, and optimism around earnings is starting to rebuild. Is this a chance to step in now, or does the recent slide suggest that investors might still be rewarded for remaining patient on valuation?

Most Popular Narrative: 21.4% Undervalued

Pool's most followed valuation narrative places fair value at $255.91 per share versus the last close at $201.17, framing current earnings optimism against a longer term growth and margin story.

Growing consumer emphasis on home-based leisure and wellness is maintaining structurally elevated demand for pools and related services, driving resilient recurring revenue for maintenance and enhancements, which should support top-line stability and growth even during new construction lulls.

Want to see the full playbook behind that fair value for Pool? It is based on steady revenue expansion, firmer margins, and a richer future earnings multiple. Curious which assumptions really move the model and how buybacks and guidance feed into that story? The complete narrative joins those pieces together in a way the headline numbers alone do not.

Result: Fair Value of $255.91 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, investors in Pool still need to reckon with housing market headwinds and inflation pressures that could restrain new pool construction and squeeze margins if costs stay elevated.

Find out about the key risks to this Pool narrative.

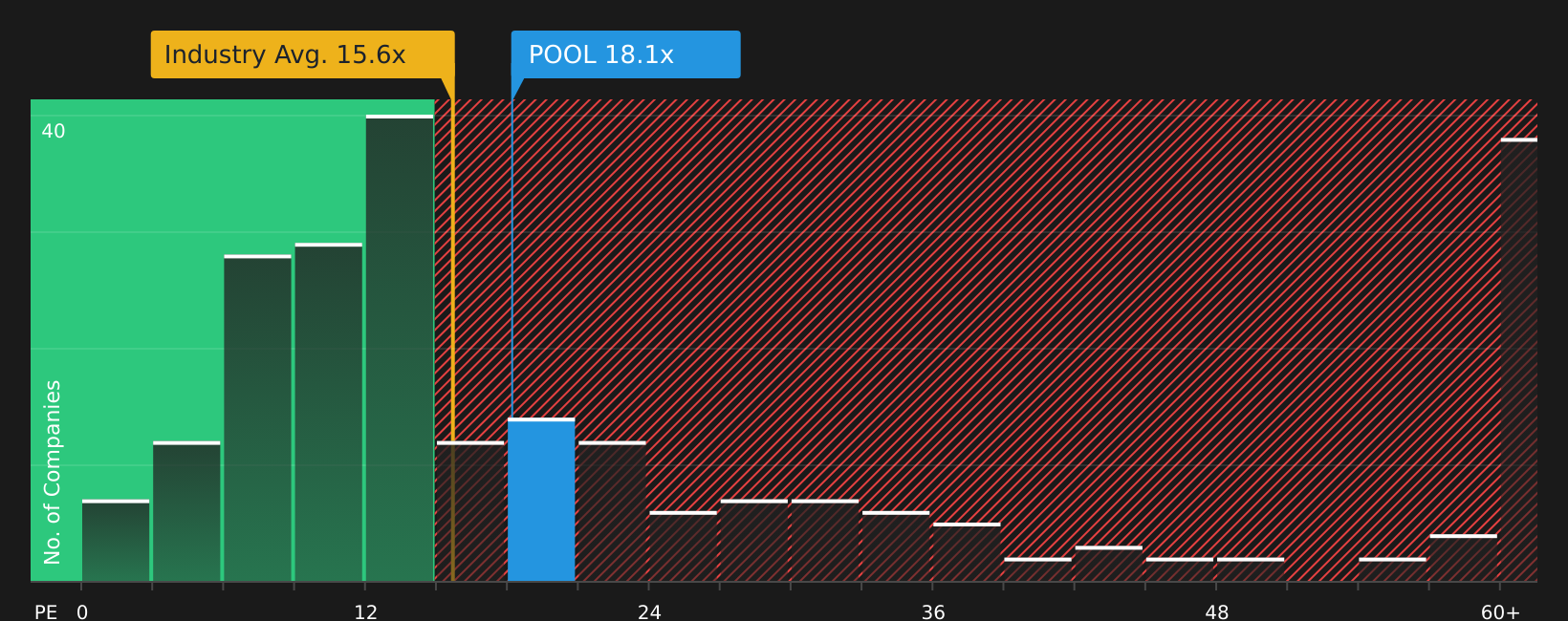

Another View on Pool Using Market Multiples

While the SWS DCF model points to Pool trading 38.3% below its estimated future cash flow value of $326.04, the picture looks different when you just look at what the market is paying for earnings today. On a P/E of 18.1x, Pool trades above both the peer average of 12.8x and the estimated fair ratio of 13.8x. That premium suggests investors are already paying up for the story, which raises the question of how much room is left if sentiment cools or growth underwhelms.

For a closer look at how these earnings multiples stack up against peers and the fair ratio, and what that might mean for valuation risk, See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With Pool carrying both clear risks and appealing rewards, do not wait for the next headline to decide where you stand. Instead, weigh both sides by reviewing the 4 key rewards and 1 important warning sign

Looking for more investment ideas beyond Pool?

If Pool has sharpened your focus on quality, do not stop here. Broaden your watchlist now so you are not late to the next opportunity.

- Target higher quality at sensible prices by scanning 47 high quality undervalued stocks that pair solid fundamentals with more reasonable market expectations.

- Strengthen your income stream by reviewing 8 dividend fortresses that offer substantial yields supported by their current payout profiles.

- Protect your capital with steadier candidates through the 84 resilient stocks with low risk scores that prioritize financial resilience over headline excitement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:POOL

Pool

Distributes swimming pool supplies, equipment, related leisure, irrigation, and landscape maintenance products in the United States and internationally.

Established dividend payer with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

DA

davidlsander on Nevgold ·

The U.S. Government Is Desperate for This Metal. This Tiny Miner Has It -- Its Closest Peer Is Already Worth Double.

Fair Value:US$2.1946.6% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6513.0% undervalued

60 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

JD

JD009 on Celsius Holdings ·

From $5M to $2B: Why the 2024 Crash Was the Best Buying Opportunity in Consumer Stocks

Fair Value:US$55.4347.7% undervalued

20 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

WA

Wavefarer on Accenture ·

High-quality global services company facing an AI-driven valuation reset.

Fair Value:US$30152.3% undervalued

16 followersusers have followed this narrative

1 commentusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

DS

DS2invest on PayPal Holdings ·

PayPal: Undervalued Cash Flow Machine or Value Trap?

Fair Value:US$69.0318.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MI

MineStackr on AbraSilver Resource ·

NAV $4B CAD

Fair Value:CA$3661.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CE

CentryResearch on Centrus Energy ·

Centrus Energy: The Next Nuclear Bottleneck Isn't Reactors. It's Fuel.

Fair Value:US$19017.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75027.5% undervalued

96 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5458.4% undervalued

63 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6513.0% undervalued

60 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Trending Discussion

BE

benjamin_lvieq on PayPal Holdings ·

An investment case is not about loving the product. Its about price vs reality.

2

|0

ST

StoxEurope on Koninklijke Ahold Delhaize ·

I ran Ahold Delhaize through a three-model triangulation — DCF, dividend discount, and residual inco...

1

|0