Advertisement

Is JD.com (NASDAQ:JD) Using Too Much Debt?

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that JD.com, Inc. (NASDAQ:JD) does use debt in its business. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for JD.com

How Much Debt Does JD.com Carry?

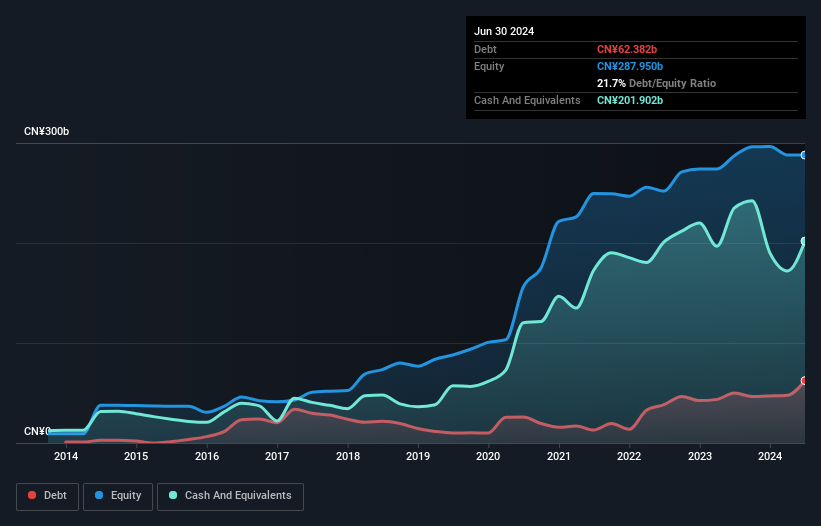

As you can see below, at the end of June 2024, JD.com had CN¥62.4b of debt, up from CN¥50.0b a year ago. Click the image for more detail. However, its balance sheet shows it holds CN¥201.9b in cash, so it actually has CN¥139.5b net cash.

How Strong Is JD.com's Balance Sheet?

The latest balance sheet data shows that JD.com had liabilities of CN¥280.2b due within a year, and liabilities of CN¥83.5b falling due after that. On the other hand, it had cash of CN¥201.9b and CN¥25.1b worth of receivables due within a year. So its liabilities total CN¥136.6b more than the combination of its cash and short-term receivables.

This deficit isn't so bad because JD.com is worth a massive CN¥306.4b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk. While it does have liabilities worth noting, JD.com also has more cash than debt, so we're pretty confident it can manage its debt safely.

In addition to that, we're happy to report that JD.com has boosted its EBIT by 33%, thus reducing the spectre of future debt repayments. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if JD.com can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. JD.com may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Over the last three years, JD.com actually produced more free cash flow than EBIT. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Summing Up

While JD.com does have more liabilities than liquid assets, it also has net cash of CN¥139.5b. The cherry on top was that in converted 154% of that EBIT to free cash flow, bringing in CN¥49b. So is JD.com's debt a risk? It doesn't seem so to us. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. Be aware that JD.com is showing 1 warning sign in our investment analysis , you should know about...

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:JD

JD.com

Operates as a supply chain-based technology and service provider in the People’s Republic of China and Europe.

Good value with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Cue Biopharma ·

Cue Biopharma (NASDAQ: CUE): The Scientist Behind Xolair Just Gave Cue a Next-Generation Shot at the Same Multi-Billion-Dollar Market

Fair Value:US$7065.0% undervalued

41 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9636.2% undervalued

45 followersusers have followed this narrative

8 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Broadcom ·

A Capital Allocation Favorite with Structural Importance

Fair Value:US$651.0541.3% undervalued

43 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

TO

Tokyo on Okta ·

Good foundation, but now it's all about the next steps

Fair Value:US$15123.0% undervalued

90 followersusers have followed this narrative

7 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Recently Updated Narratives

DC

Dc12 on Doximity ·

High physician usership and impressive AI tools

Fair Value:US$33.740.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Rog on CTT - Correios De Portugal ·

Why CTT benefits in multiple ways right now

Fair Value:€6.6710.2% undervalued

0 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

ES

Esteban on Hershey ·

Hershey - fortress brand-and-scale position in U.S. confectionery: protects the downside far better than it compounds the upside

Fair Value:US$85.86111.6% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7446.4% undervalued

65 followersusers have followed this narrative

0 commentsusers have commented on this narrative

15 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9723.5% undervalued

58 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1931.2% undervalued

49 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative