Advertisement

- United States

- /

- Retail REITs

- /

- NYSE:SPG

Simon Property Group, Inc. Annual Results Just Came Out: Here's What Analysts Are Forecasting For Next Year

It's been a good week for Simon Property Group, Inc. (NYSE:SPG) shareholders, because the company has just released its latest full-year results, and the shares gained 5.8% to US$141. Simon Property Group reported US$5.7b in revenue, roughly in line with analyst forecasts, although statutory earnings per share (EPS) of US$6.81 beat expectations, being 2.9% higher than what analysts expected. Analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. Readers will be glad to know we've aggregated the latest statutory forecasts to see whether analysts have changed their mind on Simon Property Group after the latest results.

See our latest analysis for Simon Property Group

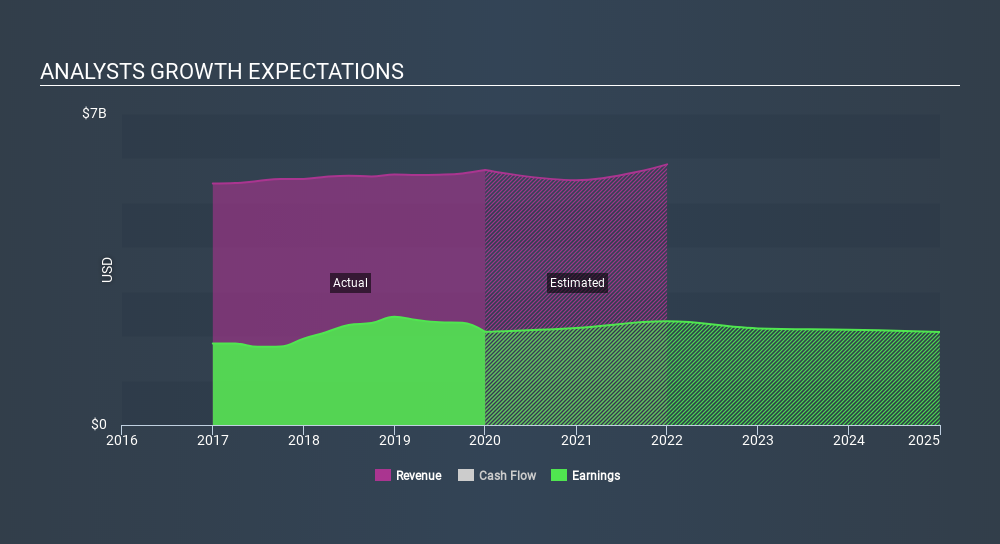

Taking into account the latest results, the current consensus, from the five analysts covering Simon Property Group, is for revenues of US$5.51b in 2020, which would reflect a measurable 4.0% reduction in Simon Property Group's sales over the past 12 months. Statutory earnings per share are expected to rise 3.0% to US$7.02. Yet prior to the latest earnings, analysts had been forecasting revenues of US$5.74b and earnings per share (EPS) of US$6.87 in 2020. If anything, analysts look to have become slightly more optimistic overall; while they decreased their revenue forecasts, EPS predictions increased and ultimately earnings are more important.

There's been no real change to the average price target of US$164, with the lower revenue and higher earnings forecasts not expected to meaningfully impact the company's valuation over a longer timeframe. There's another way to think about price targets though, and that's to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. Currently, the most bullish analyst values Simon Property Group at US$218 per share, while the most bearish prices it at US$140. As you can see, analysts are not all in agreement on the stock's future, but the range of estimates is still reasonably narrow, which could suggest that the outcome is not totally unpredictable.

Another way to assess these estimates is by comparing them to past performance, and seeing whether analysts are more or less bullish relative to other companies in the market. We would highlight that sales are expected to reverse, with the forecast 4.0% revenue decline a notable change from historical growth of 2.7% over the last five years. Compare this with our data, which suggests that other companies in the same market are, in aggregate, expected to see their revenue grow 5.1% next year. So although its revenues are forecast to shrink, this cloud does not come with a silver lining - analysts also expect Simon Property Group to grow slower than the wider market.

The Bottom Line

The biggest takeaway for us from these new estimates is that the consensus upgraded its earnings per share estimates, showing a clear improvement in sentiment around Simon Property Group's earnings potential next year. Unfortunately, analysts also downgraded their revenue estimates, and our data indicates revenues are expected to perform worse than the wider market. Even so, earnings per share are more important to the intrinsic value of the business. Even so, earnings per share are more important to the intrinsic value of the business. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. At Simply Wall St, we have a full range of analyst estimates for Simon Property Group going out to 2021, and you can see them free on our platform here..

It might also be worth considering whether Simon Property Group's debt load is appropriate, using our debt analysis tools on the Simply Wall St platform, here.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NYSE:SPG

Simon Property Group

Simon Property Group, Inc. (NYSE:SPG) is a self-administered and self-managed real estate investment trust (“REIT”).

Established dividend payer and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor