Advertisement

- United States

- /

- Industrial REITs

- /

- NYSE:PLD

How Margin Pressure and Lowered 2025 Guidance at Prologis (PLD) Has Changed Its Investment Story

Simply Wall St

Reviewed by Simply Wall St

- Prologis recently revised its 2025 earnings guidance downward, expecting diluted earnings per share between US$3.00 and US$3.15 compared to previous estimates of US$3.45 to US$3.70, following the release of its second-quarter results for 2025.

- While second-quarter sales and revenue grew year-on-year, a significant decrease in net income and profit per share indicates rising costs or margin pressure despite robust topline growth.

- To assess the impact of the lowered earnings guidance on the investment outlook, we'll analyze how margin pressure could affect Prologis' future earnings narrative.

Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 25 best rare earth metal stocks of the very few that mine this essential strategic resource.

Prologis Investment Narrative Recap

To be a Prologis shareholder today, you need to believe in continued tenant demand for premium logistics assets despite current macro challenges and margin pressures. The recent downward revision in 2025 earnings guidance highlights that while topline growth remains solid, rising costs and decelerating profit margins are the most crucial near-term risks, directly overshadowing the company’s ability to capture a rapid rebound in leasing activity. For now, the impact is material as it tempers optimism around a swift recovery in earnings momentum and rental growth.

The latest earnings announcement is directly relevant to these concerns: while sales and revenue rose year-on-year for the second quarter, net income dropped from US$861.35 million to US$571.23 million and diluted EPS declined from US$0.92 to US$0.61. This aligns with management's comments on persistent margin pressure and the shifting balance between higher revenue and rising expenses, a key issue for investors monitoring Prologis' ability to sustain operating performance while facing slower leasing and macro uncertainty.

However, if macro trends worsen and leasing activity fails to accelerate as hoped, investors should be aware that ...

Read the full narrative on Prologis (it's free!)

Prologis' outlook anticipates $9.5 billion in revenue and $3.5 billion in earnings by 2028. This scenario assumes a 2.1% annual revenue growth rate and a $0.1 billion increase in earnings from the current $3.4 billion.

Uncover how Prologis' forecasts yield a $119.15 fair value, a 9% upside to its current price.

Exploring Other Perspectives

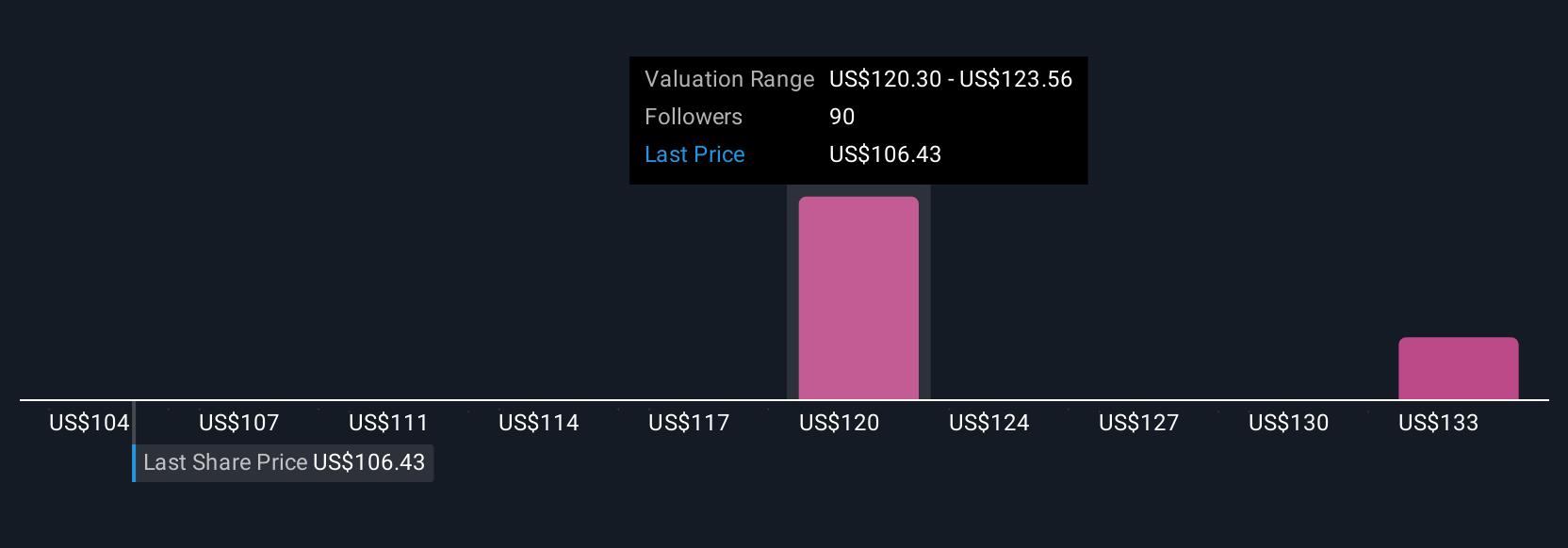

Simply Wall St Community members offered 7 fair value estimates for Prologis, ranging from US$104 to US$136.11 per share. While investor fair value opinions vary widely, recent margin pressure and EPS guidance cuts bring renewed attention to earnings quality and future growth expectations.

Explore 7 other fair value estimates on Prologis - why the stock might be worth 5% less than the current price!

Build Your Own Prologis Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Prologis research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Prologis research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Prologis' overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Outshine the giants: these 20 early-stage AI stocks could fund your retirement.

- These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:PLD

Prologis

Prologis, Inc., is the global leader in logistics real estate with a focus on high-barrier, high-growth markets.

Established dividend payer and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value US$282.83|32.8% undervalued

BL

Community Contributor

Planet Labs: At The Heart Of The Emerging New Space Boom

Fair Value US$11.31|45.4% undervalued

AN

Community Contributor

Exxon in Guyana 5 year forecast Low $135 to High $189

Fair Value US$174.00|37.0% undervalued

AG

Community Contributor