OUTFRONT Media (OUT) is attracting fresh attention after several top brokerages upgraded the stock. Analysts are pointing to a renewed sense of optimism about its business direction and potential growth in the advertising landscape.

OUTFRONT Media has caught investors’ eyes lately, with strong analyst upgrades following upbeat earnings and a newly affirmed dividend. In the last month alone, the stock delivered a powerful 24% share price return, contributing to a solid 26.8% total return over the past year. This signals that fresh momentum is building around its growth story.

With analyst upgrades fueling the rally and shares trading just above consensus price targets, investors face a pivotal question: is OUTFRONT Media undervalued, or is the market already pricing in all its future growth?

Advertisement

Most Popular Narrative: 10.4% Overvalued

According to the most widely followed narrative, the stock’s fair value estimate of $20 stands about 10% below the latest closing price of $22.08. This gap highlights rising market optimism at a time when recent analyst upgrades have translated into tangible share price gains.

OUTFRONT's ongoing digital conversion of static billboards and transit assets to digital displays enables higher ad rotation, dynamic content, and premium pricing. This directly supports accelerated top-line growth and long-term margin expansion.

What is the real reason behind the market’s high hopes? The narrative hinges on the company’s bold technology shift and a margin outlook that might surprise you. Want to see what financial milestones are driving this price target? You’ll have to check the full narrative for the inside story.

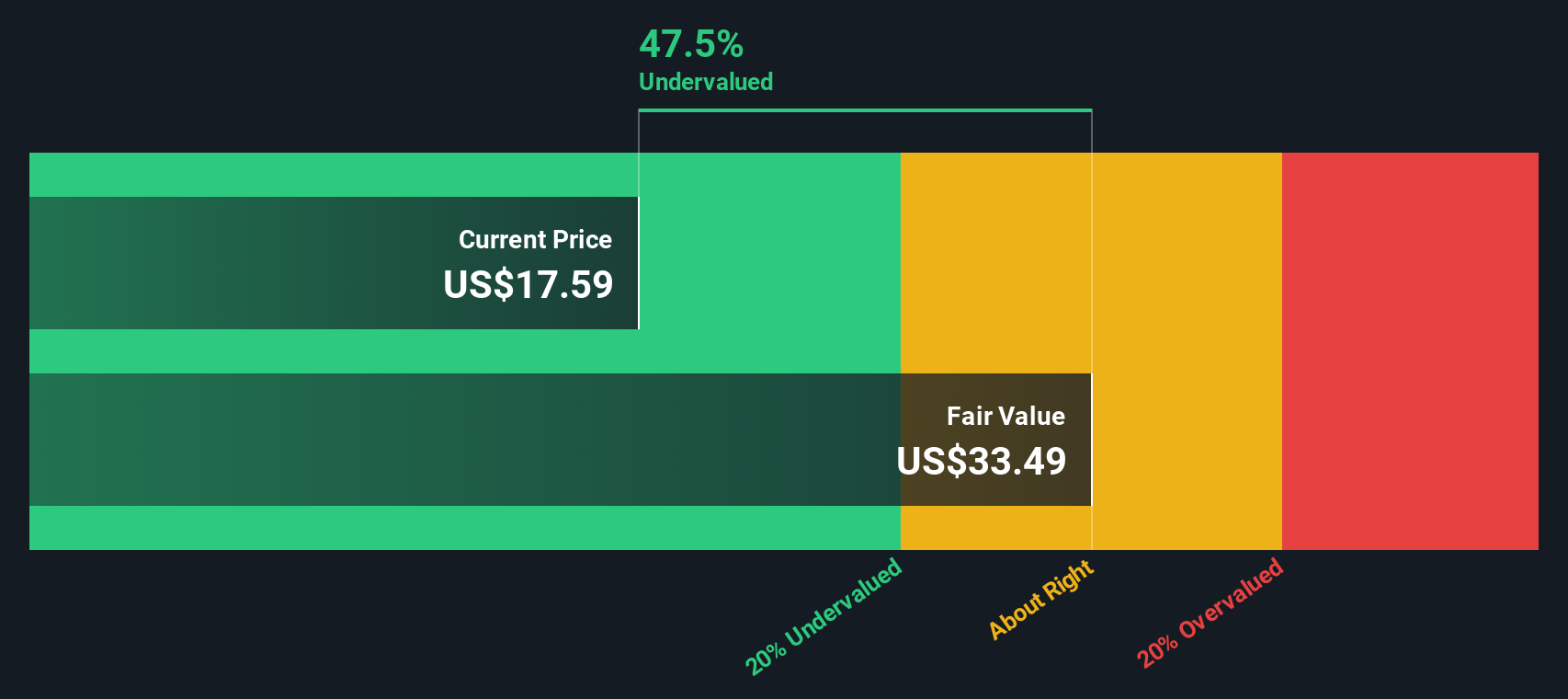

Another View: Discounted Cash Flow Paints a Different Picture

Looking through the lens of our DCF model, things look very different. According to SWS DCF, OUTFRONT Media’s shares are trading about 44% below the model’s fair value estimate. While the market’s favorite analysts see the stock as overvalued, DCF suggests there could be meaningful upside. Which side of the valuation debate will prove right in the end?

If you’re the type who prefers to dig into the numbers and shape your own view, you can easily craft a personalized narrative in just minutes. Do it your way

A great starting point for your OUTFRONT Media research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Looking for More Winning Investment Ideas?

Don’t let your next big opportunity slip away. Use the Simply Wall St Screener to uncover high-potential companies most investors miss and start building a portfolio that stands out.

Ride the innovation wave and spot tomorrow’s leaders with these 25 AI penny stocks as artificial intelligence transforms industries at a rapid pace.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield) • Undervalued Small Caps with Insider Buying • High growth Tech and AI Companies

OUTFRONT is one of the largest and most trusted out-of-home media companies in the U.S., helping brands connect with audiences in the moments and environments that matter most.