Advertisement

- United States

- /

- Office REITs

- /

- NYSE:KRC

Kilroy Realty (KRC): How Analyst Upgrades Are Shaping the Latest Valuation Narrative

Simply Wall St

Reviewed by Simply Wall St

Analyst coverage of Kilroy Realty (KRC) has ramped up recently, as major firms such as Wells Fargo, BMO Capital, RBC Capital, and Jefferies have adjusted their ratings and forecasts. This recent activity has led investors to take a closer look at the company’s prospects.

See our latest analysis for Kilroy Realty.

Momentum has gradually returned to Kilroy Realty’s shares, with a year-to-date share price return of 7.6% and a standout one-year total shareholder return of 9.5%. Recent moves, such as the Board’s decision to affirm the quarterly dividend, have reinforced confidence. However, long-term shareholders are still catching up from a challenging five-year total return of -13.3%.

If you’re looking for more opportunities beyond the real estate sector, now may be a good time to broaden your perspective and discover fast growing stocks with high insider ownership

With analyst attention sharpening and the stock trading close to consensus price targets, the question remains: is Kilroy Realty’s current valuation an attractive entry point, or is the market already anticipating future growth?

Most Popular Narrative: 10% Undervalued

With Kilroy Realty’s most widely followed narrative anchoring fair value at $42.93, the stock’s last close of $42.89 lands within cents of that estimate. This highlights how current expectations are shaping perceptions of opportunity and risk just beneath the surface.

The need for ongoing significant ESG investments to keep buildings compliant with tenant and investor sustainability demands may strain capital expenditures. Failure to keep up could risk reputation and occupancy, while maintaining compliance may weigh on net margins. Industry-wide stagnant or declining rents and persistent tenant downsizing trends accelerate vacancy, necessitating costly repositioning of assets and increasing capital requirements, which will constrain FFO growth and elevate refinancing risks in a risk-averse capital market.

Want to unlock the financial puzzle behind this valuation? The most crucial forecasts driving the narrative focus on compressed profits, tightened margins, and a sharp shift in the company’s future earnings landscape. Missing the real drivers could mean missing the next big move in Kilroy’s share price.

Result: Fair Value of $42.93 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, a faster recovery in key West Coast markets or surging demand from AI and biotech tenants could significantly improve Kilroy Realty’s growth outlook.

Find out about the key risks to this Kilroy Realty narrative.

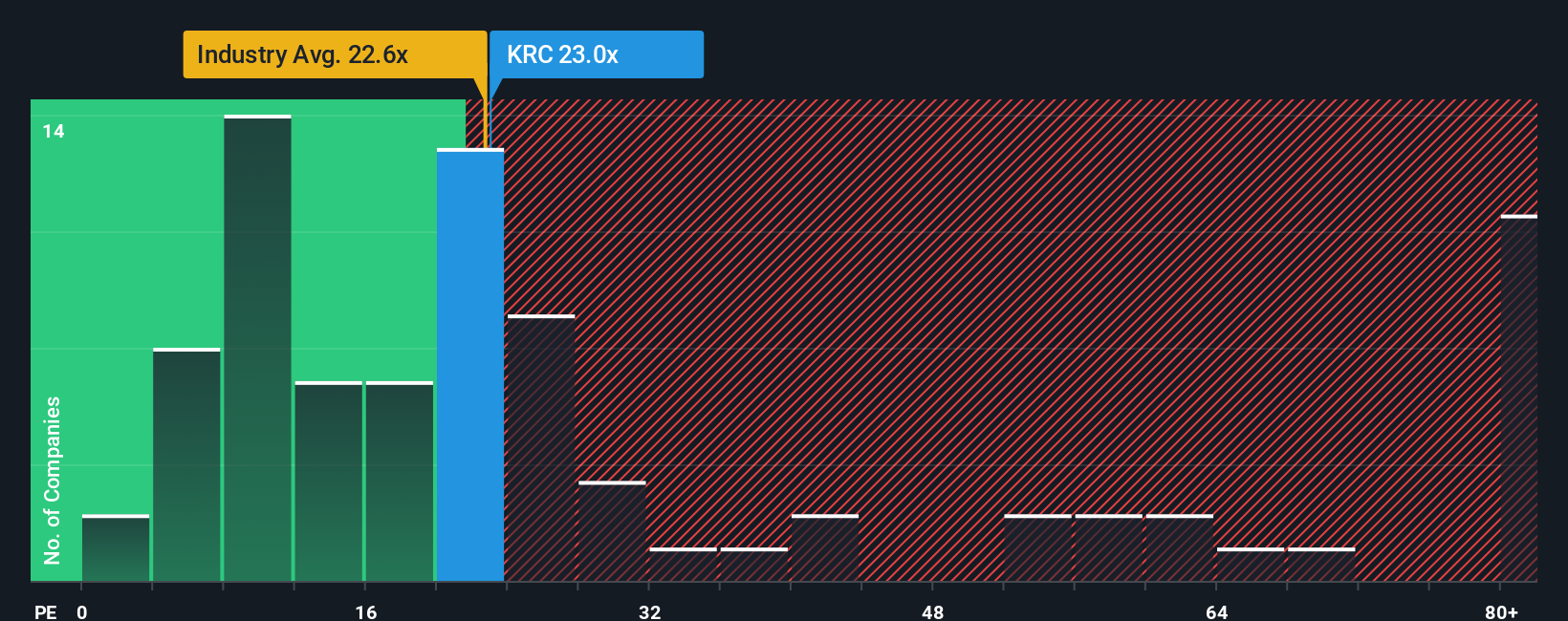

Another View: Comparing Market Multiples

While our fair value estimate suggests Kilroy Realty is trading at a discount, a look at the price-to-earnings ratio reveals a more nuanced story. Kilroy’s ratio stands at 15.8x, which is good value compared to both the global industry average of 22.9x and peers at 32.8x. However, it is almost identical to the fair ratio of 15.5x, which the market could trend toward. This suggests that upside might be limited if broader sentiment cools. Are markets already pricing in all the positives, or is there room for surprise?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Kilroy Realty Narrative

If the story outlined here does not match your own findings, or you want to dig even deeper, you can quickly form your own view and narrative straight from the data. Do it your way

A great starting point for your Kilroy Realty research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Smart moves start with smart research. If you want your portfolio to keep up with the market’s leaders, you owe it to yourself to see what else is out there.

- Zero in on long-term income potential by targeting these 15 dividend stocks with yields > 3% that offer yields above 3%, giving your portfolio an edge in any market.

- Tap into accelerating innovation by checking out these 25 AI penny stocks where demand for next-generation technology could mean opportunities for strong performance in the future.

- Supercharge your search for undervalued opportunities by reviewing these 920 undervalued stocks based on cash flows that the market has yet to fully appreciate.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Kilroy Realty might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:KRC

Kilroy Realty

Kilroy is a leading U.S. landlord and developer, with operations in San Diego, Los Angeles, the San Francisco Bay Area, Seattle, and Austin.

6 star dividend payer and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative