Advertisement

- United States

- /

- Residential REITs

- /

- NYSE:CSR

Centerspace (CSR) Earnings Heavily Influenced by $52.9M One-Off Gain, Stoking Skepticism on Profit Quality

Simply Wall St

Reviewed by Simply Wall St

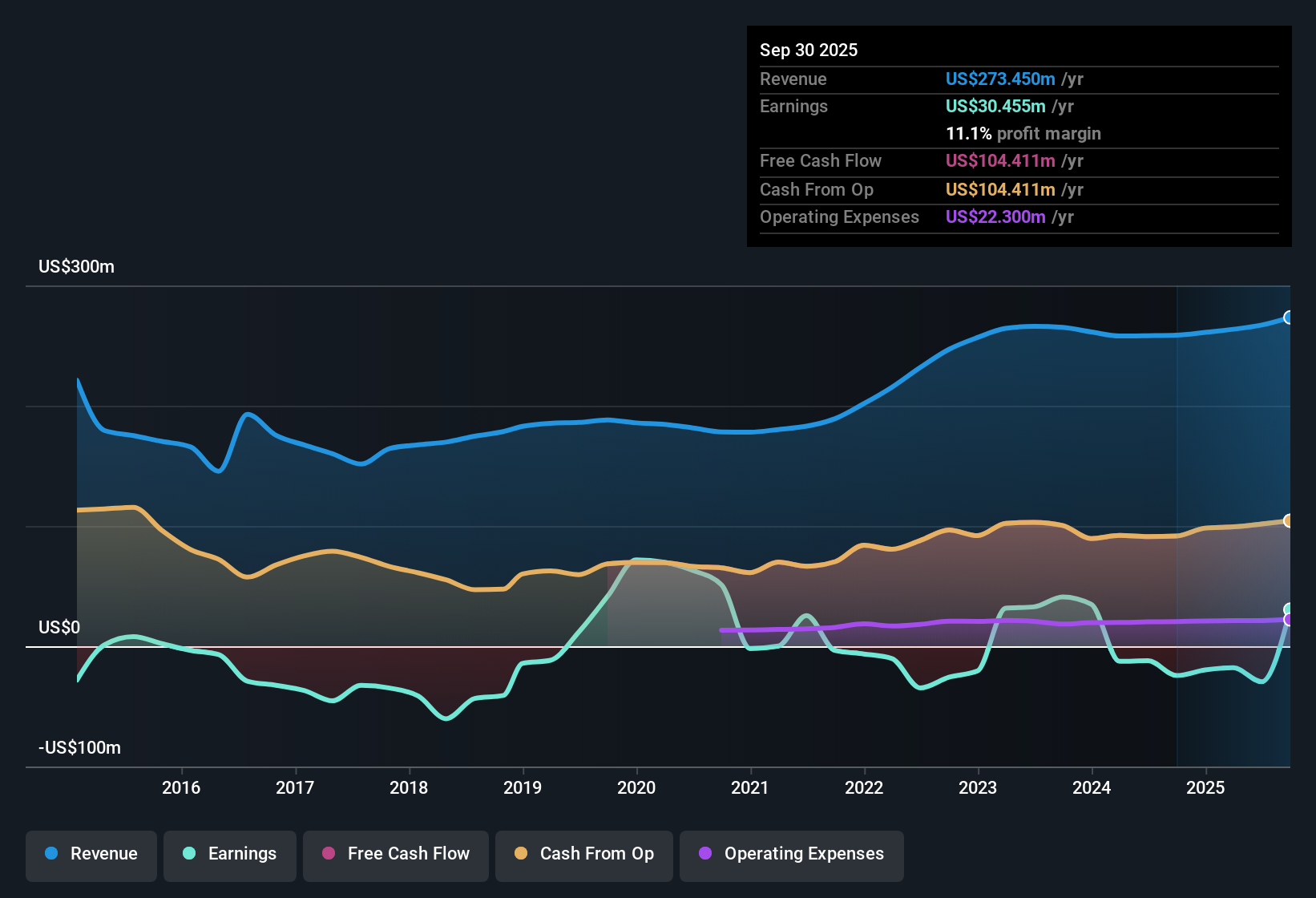

Centerspace (CSR) is forecasting a steep annual earnings decline of 36.6% over the next three years, even as revenue is expected to grow modestly at 2.2% per year, trailing the broader US market’s 10.5% pace. While the company has recently turned profitable, reported net profits were boosted by a one-off gain of $52.9 million. Its average annual earnings have fallen by 16% over the past five years. With growth rates lagging and profit quality impacted by non-recurring items, investors may view the headline numbers with a dose of caution this quarter.

See our full analysis for Centerspace.Next up, we’ll see how these latest figures compare to the narrative that investors are following on Simply Wall St, highlighting where consensus may meet resistance and where surprises await.

See what the community is saying about Centerspace

Margins Projected to Swing from Negative to Positive

- Profit margins are forecast to climb from -11.0% today to 4.7% in the next three years, reflecting an expected turnaround in core profitability beyond headline earnings figures.

- According to the analysts' consensus view, this margin recovery is supported by ongoing rental demand and demographic shifts in Centerspace’s Midwest and secondary markets.

- Consensus narrative notes demographic trends, such as delayed homeownership, continue to support high occupancy rates and tenant retention. This is helping drive the anticipated margin improvement.

- Management’s focus on recycling capital into newer, higher-growth properties in Salt Lake City and Colorado is expected to boost net operating income margins and provide a buffer against volatility in less stable markets.

- The forecasted positive margin trend, anchored by persistent demand and strategic asset recycling, challenges any lingering pessimism around the company's underlying ability to generate sustainable profits compared to its loss-making past.

- Curious if this profit swing means Centerspace will finally catch up to peers? See how analysts weigh the potential in the full narrative. 📊 Read the full Centerspace Consensus Narrative.

Dividend Risks Surface Amid High Leverage

- Centerspace’s balance sheet targets net debt to EBITDA in the low to mid 7x range, which is high versus most peer REITs. This raises flags about the sustainability of its dividend and flexibility for future growth.

- Analysts' consensus view highlights that while disciplined balance sheet management is a stated goal, persistent high leverage alongside increased exposure to volatile markets (such as Denver) could make the company vulnerable to higher borrowing costs and constrain dividend payouts.

- Bears argue that capital recycling into more institutional markets could expose Centerspace to timing risks on asset sales and higher acquisition cap rates. This creates potential hits to book value and near-term declines in FFO.

- With dividend sustainability already a risk in the consensus view, any missteps in executing this geographic transformation could pressure both income investors and those looking for capital gains.

Valuation Gap: Discount to DCF and Analyst Target

- Shares are currently trading at $60.37, which is a 35% discount to the DCF fair value of $92.91 and about a 9.7% discount to the analyst price target of $66.88.

- According to the analysts’ consensus view, this sizable discount may reflect lingering skepticism towards the company’s slower long-term revenue growth (projected at 2.2% annually) and earnings durability, even as select valuation metrics screen as “good value” relative to industry peers.

- Consensus narrative emphasizes that the price-to-earnings ratio of 33.1x is above the North American Residential REITs industry average of 24.9x but below peer averages of 86.2x. This illustrates a nuanced market view balancing perceived risks and rewards.

- Investors are being challenged to weigh long-duration rental demand and portfolio upgrades against ongoing balance sheet and margin pressures when deciding if the current valuation is cheap or a value trap.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Centerspace on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Think you spot a story the numbers don't tell, or want to rethink the trends yourself? Craft your own narrative in just a few minutes. Do it your way

A great starting point for your Centerspace research is our analysis highlighting 2 key rewards and 4 important warning signs that could impact your investment decision.

See What Else Is Out There

Centerspace faces ongoing challenges with high leverage and dividend risks, which leaves its financial health and consistent shareholder payouts in question.

If you want alternatives with stronger fundamentals and less balance sheet strain, check out solid balance sheet and fundamentals stocks screener (1981 results) built to weather volatility and safeguard your investments.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:CSR

Centerspace

An owner and operator of apartment communities committed to providing great homes by focusing on integrity and serving others.

Average dividend payer with slight risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|7.5% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|25.4% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.6% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.0% undervalued

DA

Community Contributor