Advertisement

- United States

- /

- Real Estate

- /

- NYSE:CBRE

CBRE Group, Inc. Third-Quarter Results Just Came Out: Here's What Analysts Are Forecasting For Next Year

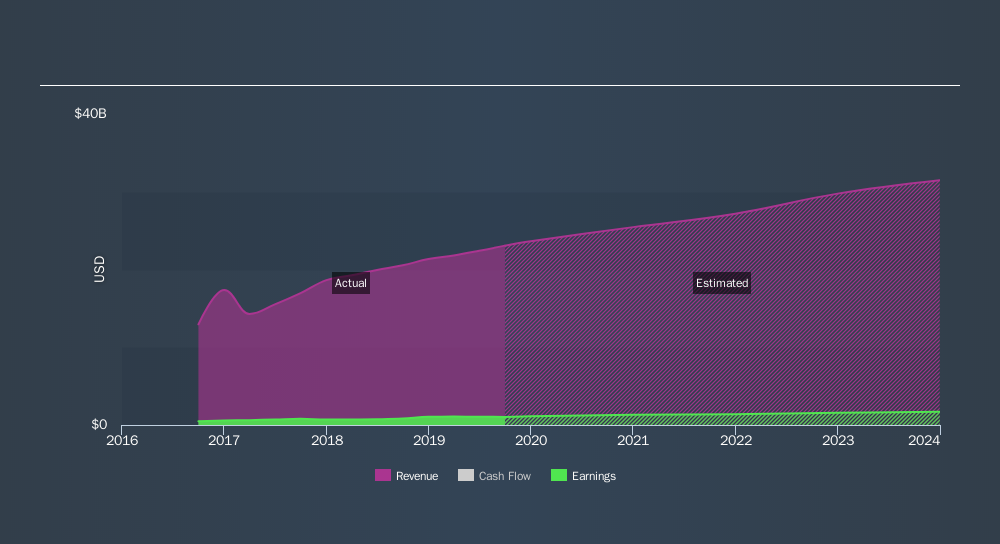

CBRE Group, Inc. (NYSE:CBRE) just released its third-quarter report and things are looking bullish. The company beat expectations with revenues of US$5.9b arriving 3.1% ahead of forecasts. Earnings per share (EPS) were US$0.75, 2.2% ahead of estimates. This is an important time for investors, as they can track a company's performance in its report, look at what top analysts are forecasting for next year, and see whether the latest forecasts would suggest a change of heart on the company. We thought readers would find it interesting to see analysts' latest post-earnings forecasts for next year.

Check out our latest analysis for CBRE Group

After the latest results, the six analysts covering CBRE Group are now predicting revenues of US$25b in 2020. If met, this would reflect a decent 10% improvement in sales compared to the last 12 months. Earnings per share are expected to bounce 25% to US$3.86. In the lead-up to this report, analysts had been modelling revenues of US$25b and earnings per share (EPS) of US$3.77 in 2020. Analysts seem to have become more bullish on the business, judging by their new earnings per share estimates.

There's been no major changes to the consensus price target of US$59.67, suggesting that the improved earnings per share outlook is not enough to have a long-term positive impact on the stock's valuation. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. The most optimistic CBRE Group analyst has a price target of US$70.00 per share, while the most pessimistic values it at US$54.00. Still, with such a tight range of estimates, it suggests analysts have a pretty good idea of what they think the company is worth.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. We would highlight that CBRE Group's revenue growth is expected to slow, with forecast 10% increase next year well below the historical 21%p.a. growth over the last five years. Juxtapose this against the other companies in the market with analyst coverage, which are forecast to grow their revenues (in aggregate) 6.2% next year. So it's pretty clear that, while CBRE Group's revenue growth is expected to slow, it's still expected to grow faster than the market itself.

The Bottom Line

The most important thing to take away from this is that analysts upgraded their earnings per share estimates, suggesting that there has been a clear increase in optimism towards CBRE Group following these results. Fortunately, analysts also reconfirmed their revenue estimates, suggesting sales are tracking in line with expectations - and our data does suggest that CBRE Group's revenues are expected to grow faster than the wider market. The consensus price target held steady at US$59.67, with the latest estimates not enough to have an impact on analysts' estimated valuations.

Still, the long-term prospects of the business are much more relevant than next year's earnings. We have estimates - from multiple CBRE Group analysts - going out to 2023, and you can see them free on our platform here.

You can also see whether CBRE Group is carrying too much debt, and whether its balance sheet is healthy, for free on our platform here.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About NYSE:CBRE

CBRE Group

Operates as a commercial real estate services and investment company in the United States, the United Kingdom, and internationally.

Moderate growth potential with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.1% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|20.9% undervalued

TI

Community Contributor