Advertisement

- United States

- /

- Hotel and Resort REITs

- /

- NYSE:AHT

Ashford Hospitality Trust, Inc. Just Reported, And Analysts Assigned A US$2.88 Price Target

Shareholders in Ashford Hospitality Trust, Inc. (NYSE:AHT) had a terrible week, as shares crashed 46% to US$1.00 in the week since its latest full-year results. It looks like the results were pretty good overall. While revenues of US$1.5b were in line with analyst predictions, statutory losses were much smaller than expected, with Ashford Hospitality Trust losing US$1.58 per share. Analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. So we collected the latest post-earnings statutory consensus estimates to see what could be in store for next year.

View our latest analysis for Ashford Hospitality Trust

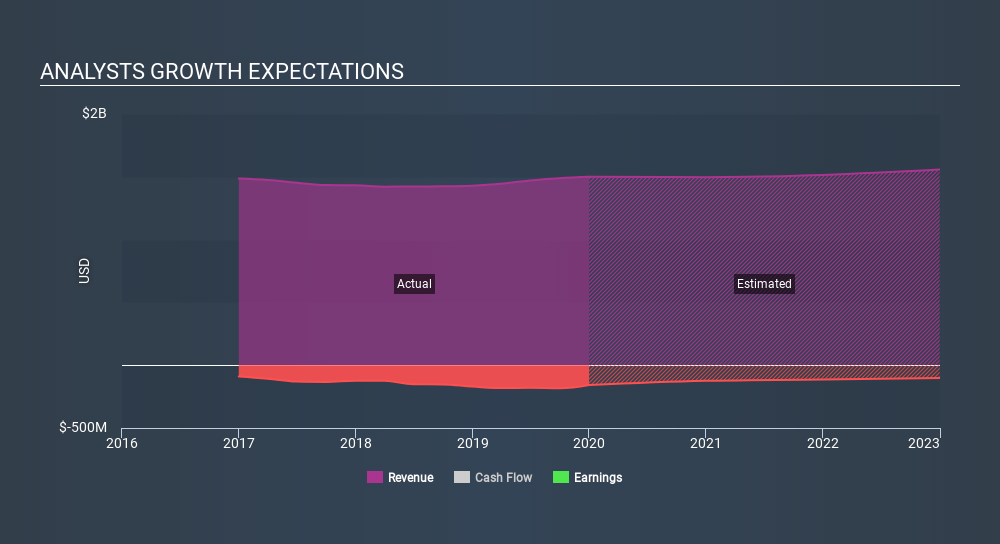

Following last week's earnings report, Ashford Hospitality Trust's five analysts are forecasting 2020 revenues to be US$1.50b, approximately in line with the last 12 months. Per-share statutory losses are expected to explode, reaching US$1.07 per share. Prior to the latest earnings, analysts were forecasting revenues of US$1.52b in 2020, and did not provide an EPS estimate. So we can see that while the consensus made no real change to its revenue estimates, analysts began providing loss per share estimates, suggesting the business' (lack of) earnings is becoming more crucial to the business case following these results.

With the increase in forecast losses for next year, it's perhaps no surprise to see that the average analyst price target dipped 11% to US$2.88, with analysts signalling that growing losses would be a definite concern. The consensus price target just an average of individual analyst targets, so - considering that the price target changed, it would be handy to see how wide the range of underlying estimates is. There are some variant perceptions on Ashford Hospitality Trust, with the most bullish analyst valuing it at US$5.00 and the most bearish at US$1.30 per share. As you can see the range of estimates is wide, with the lowest valuation coming in at less than half the most bullish estimate, suggesting there are some strongly diverging views on how analysts think this business will perform. With this in mind, we wouldn't assign too much meaning to the consensus price target, as it is just an average and analysts clearly have some deeply divergent views on the business.

In addition, we can look to Ashford Hospitality Trust's past performance and see whether business is expected to improve, and if the company is expected to perform better than wider market. These estimates imply that sales are expected to slow, with a forecast revenue decline of 0.2% a significant reduction from annual growth of 7.0% over the last five years. By contrast, our data suggests that other companies (with analyst coverage) in the same market are forecast to see their revenue grow 5.0% annually for the foreseeable future. So although its revenues are forecast to shrink, this cloud does not come with a silver lining - analysts also expect Ashford Hospitality Trust to grow slower than the wider market.

The Bottom Line

Fortunately, analysts also reconfirmed their revenue estimates, suggesting sales are tracking in line with expectations - although our data does suggest that Ashford Hospitality Trust's revenues are expected to perform worse than the wider market. Analysts also downgraded their price target, suggesting that the latest news has led analysts to become more pessimistic about the intrinsic value of the business.

Still, the long-term prospects of the business are much more relevant than next year's earnings. At Simply Wall St, we have a full range of analyst estimates for Ashford Hospitality Trust going out to 2022, and you can see them free on our platform here..

You can also see whether Ashford Hospitality Trust is carrying too much debt, and whether its balance sheet is healthy, for free on our platform here.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NYSE:AHT

Ashford Hospitality Trust

Together with its subsidiaries (“Ashford Trust”), is a real estate investment trust (“REIT”).

Slight risk and fair value.

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|41.9% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|14.1% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$613.59|1.3% undervalued

AN

Based on Analyst Price Targets