Advertisement

- United States

- /

- Hotel and Resort REITs

- /

- NasdaqGS:SVC

Analysts Have Been Trimming Their Service Properties Trust (NASDAQ:SVC) Price Target After Its Latest Report

One of the biggest stories of last week was how Service Properties Trust (NASDAQ:SVC) shares plunged 24% in the week since its latest first-quarter results, closing yesterday at US$4.75. Revenues were in line with expectations, at US$484m, while statutory losses ballooned to US$0.20 per share. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. We've gathered the most recent statutory forecasts to see whether the analysts have changed their earnings models, following these results.

Check out our latest analysis for Service Properties Trust

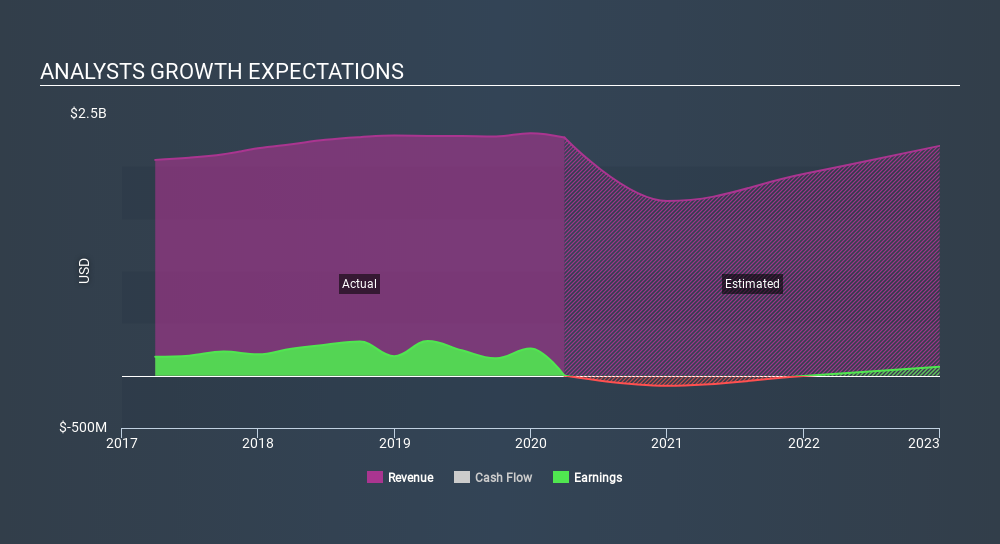

Taking into account the latest results, the current consensus, from the two analysts covering Service Properties Trust, is for revenues of US$1.67b in 2020, which would reflect a concerning 27% reduction in Service Properties Trust's sales over the past 12 months. Earnings are expected to tip over into lossmaking territory, with the analysts forecasting statutory losses of -US$1.52 per share in 2020. Yet prior to the latest earnings, the analysts had been anticipated revenues of US$1.49b and earnings per share (EPS) of US$1.51 in 2020. Despite increasing their revenue numbers, the analysts now anticipate the business will report a loss instead of a profit. It seems the incremental revenue is not without its costs.

It will come as no surprise that expanding losses caused the consensus price target to fall 8.0% to US$8.17 with the analysts implicitly ranking ongoing losses as a greater concern than growing revenues.

Of course, another way to look at these forecasts is to place them into context against the industry itself. These estimates imply that sales are expected to slow, with a forecast revenue decline of 27%, a significant reduction from annual growth of 5.0% over the last five years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 5.1% next year. It's pretty clear that Service Properties Trust's revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The most important thing to take away is that the analysts are expecting Service Properties Trust to become unprofitable next year. They also upgraded their revenue estimates for next year, even though sales are expected to grow slower than the wider industry. The consensus price target fell measurably, with the analysts seemingly not reassured by the latest results, leading to a lower estimate of Service Properties Trust's future valuation.

Following on from that line of thought, we think that the long-term prospects of the business are much more relevant than next year's earnings. At least one analyst has provided forecasts out to 2022, which can be seen for free on our platform here.

That said, it's still necessary to consider the ever-present spectre of investment risk. We've identified 4 warning signs with Service Properties Trust (at least 1 which can't be ignored) , and understanding these should be part of your investment process.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NasdaqGS:SVC

Service Properties Trust

SVC is a real estate investment trust with over $11 billion invested in two asset categories: hotels and service-focused retail net lease properties.

Undervalued with mediocre balance sheet.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|24.9% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.3% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.5% undervalued

DA

Community Contributor